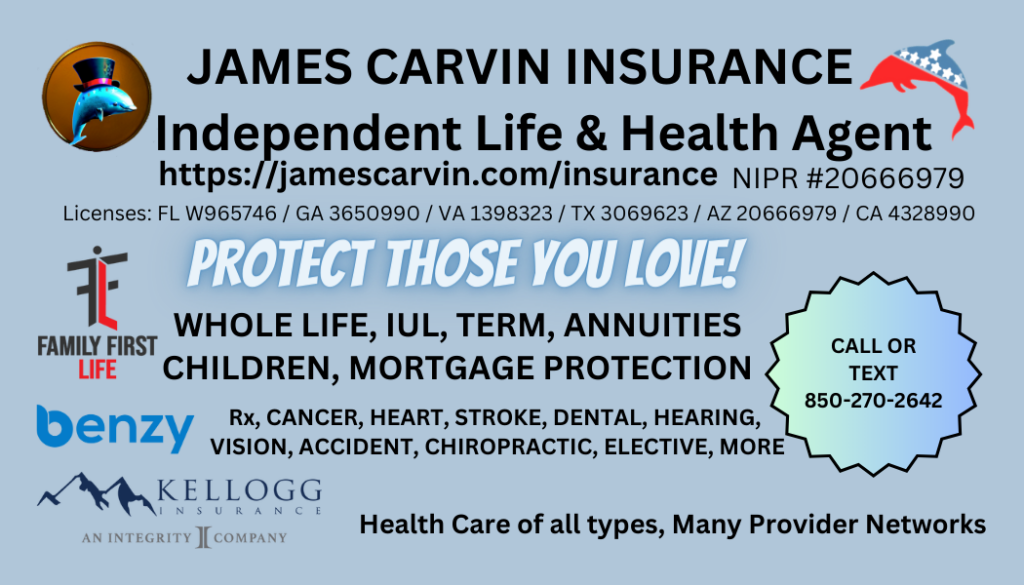

Licensed insurance agent W965746. National Producer #20666979. Presidential candidate 2016. Inventor. Entrepreneur. Philosopher. James has two grown children, cares for the disabled, and blogs in his spare time when he's not on the road helping families optimize their awesomeness.

Annual enrollment period for Medicare is October 15th through December 7th.

Open enrollment season for the Federally Facilitated Marketplace is November 1st through January 15th.

Many group health and private health insurance plans limit enrollment and changes to similar time frames.

Medicare offers an open enrollment period for those who want to make changes to their Medicare Advantage plans from January 1st through March 31st.

Initial enrollment periods for Medicare begin three months prior to the month of your 65th birthday and end the end of the third month after the month of your birthday.

Special enrollment periods take place when events trigger them.

Qualifying for social security may happen at a young age if a person is disabled. Being eligible for social security benefits can make a person eligible for Medicare before the age of 65.

You’ll find me out at local pharmacies here in Tallahassee during enrollment season. More info on that to come. Stand by.

I’ve been working on my branding problem in my spare time. It’s been a daunting project. What’s on your front page? If you were to tell your story, where would you begin? Would you start at the end, the beginning or somewhere in the middle? What theme would you highlight? What would you want the world to know?

Business Card version 12.7

It’s easier for some than others. My latest card involved a simple change of phone number from the previous one. I’ve also changed my email address. But those aren’t branding issues. It’s the images and logos. There is a story behind each one of them. Most people would opt for simplicity. Why did I put a hat on that dolphin? Why two that aren’t the same? What are these other symbols?

Simplicity

The cardinal rule in marketing and advertising is “less is more.” I’m going to advertiser hell for this business card. I know it. But it gets worse. Here’s the back…

The back of Business Card version 12.7

Yeah, that’s right. So unprofessional. Why?

Marketing Organizations vs Products

As an independent insurance broker, I can contract and produce insurance products for all sorts of companies. I’m in charge of choosing what I can recommend and I really like that. I contract with more than most independent brokers because I’m about people more than I’m about commissions. People have a variety of needs and qualifications. But I have a problem. I do want to bring attention to the companies I work with and to the insurance products I offer, but I need a single message – a simple idea. So what single message do I want to bring recognition to? Here’s my challenge …

I’ll start with marketing organizations. A field insurance marketing organization provides a nice plug and play system. The hard work of contracting is made easy.

I started my insurance career with one of the largest life insurance marketing organizations in the country – Family First Life.

FFL works with dozens of life insurance carriers, offering hundreds of life insurance products. Some of the names are already well recognized – names like Mutual of Omaha, Gerber, John Hancock, Aflac and Corebridge. Others are lesser known but quite good.

Then came Benzy. I had wanted to offer health insurance from the start. As an Independent Marketing Organization, Benzy offers two types of products – (1)Health Matching Accounts (HMAs) and (2)private health insurance plans. The insurance plans are with Allstate and Manhattan Life.

Let me offer a quick overview of the types of health insurance products this world has and where Benzy fits in. Health insurance products fall into a number of buckets. There are those that focus on the senior citizens and the Medicare/Medicaid market. And there are those who don’t. With the exception of the HMA, Benzy is for those who don’t. This latter bucket is then itself divided into two general categories – those who need comprehensive insurance to cover preconditions, and those who don’t. Again, with the exception fo the HMA, Benzy’s current line up of products through Allstate and Manhattan Life is for those who don’t. Then finally, there are those who can afford ACA plans (Obamacare) and those who can’t or are unwilling. Benzy products are for those who’d like to pay less money than they would with the Federally Facilitated Marketplace (FFM), which is how the Affordable Care Act (ACA – AKA Obamacare), attempts to make health insurance affordable for everyone. Benzy products don’t offer Obamacare. They offer more affordable alternatives. If government cost sharing and tax credits are needed, I provide that through Kellogg.

My goal was to offer every bucket. What Benzy didn’t do as a marketing organization, Kellog did do. If someone needs Obamacare, I can offer a variety of ACA Federally Facilitated Marketplace products. And if a person has, or needs to get onto Medicare, I have numerous carriers and products for that thanks to Kellogg. There are all sorts of things these organizations do for me in terms of back office support, lead generation, training and marketing so I don’t have to reinvent the wheel.

All that said, I can contract directly with carriers, as well. Tallahassee is one example. It’s my goal to represent all the best plans here in my local market. It’s a changing target that required a lot of training and certification so it’s no easy task, but to provide solutions no matter what the needs of my client are, it’s all part of what I do. I don’t want to be a salesman. I want to be a consultant. My job, is to simplify the complex by knowing how to explore options quickly and distill information into what matters most to my clients.

On this current iteration of my business card, I’ve chosen to add the logos of these three major marketing organizations. Without them, I would never have been able to start my business. Later, I’d like to train and organize an agency of my own. If you are interested in the insurance business, or know someone looking for a great career, I’m happy to mentor new agents. In a later, more simplified version, I’ll remove the IMO logos from my front page and business card. You only want one image. Right? Well … that leaves me with my dolphins. Ultimately, what I’m marketing is James Carvin Insurance. I want you to see my brand, not theirs. But to know my brand is to know my story. Would you like to know about me?

My Story

I’ve got a lot of content on the web. I started telling stories about my family after my father passed in 1995. I was working on my Masters degree and serving as an adjunct professor at a seminary at that time. There were group chats and forums avaialable on Compuserve back then. I was heavily engaged. Then later, I put up a lot of theological content on a group called CARM, as well. I also had a MySpace page and about a dozen others, all before Facebook existed. I owned and put up content on about forty domains to theme out my various interests. On Facebook, I manage dozens of groups and pages.

Despite all that, I never made the connections I wanted. One web site I built had over a hundred million page views in a three-month span but, as with several other businesses I hoped to get up and running, I was never able to raise funds. Ultimately, I had to set the whole enterprise to the side for another day and reinvent myself.

Business Card Version 12.5

Recent Reinvention

I got another degree. This one was in Interdisciplinary Studies at ASU. I busted through it easily in my part time with a 4.0 while I drove for Uber and Lyft. Uber paid for my degree. I thought better credentials might be useful and it only took a few years, so why not? IDS degrees are for those who want double majors. My concentrations were in philosophy and organizational leadership. My goal was to start a philosophical society. I call it the Pamalogy Society. Pamalogy is the philosophy of awesomeness – Awesomeology. It was a great idea, but back to the same old problem – I’m not a fund raiser at heart. I’m an inventor. So I haven’t yet gotten my philosophical society off the ground.

Meantime, I have bills to pay. What I needed was a business I didn’t invent from scratch. The insurance business solved that problem for me. Multi-billion dollar insurance companies needed knowledgeable people to offer their knowledge and expertise. I could do that. Why not just be an awesome insurance consultant? I can make a difference in people’s lives. That matters. And there were very few start up costs. But about that branding …

Can Dolphins Wear Top Hats?

I got baptized with my top hat on.

Really.

A logo that got baptized?

The top hat with sprocket is the Pamalogy Society logo. Top hats symbolize excellence. Sprockets symbolize innovation. Surely we are endowed with great imaginations and can invent new forms of excellence. Isn’t that what awesomeness is? When I put on my top hat, I recognize my call to excellence and innovation. Don’t think in problems. Think in solutions. Let me find you your solution! Are you paying too much for health care? Have you built a financial and digital legacy for your family? Did you fall in love with a charity you wanted to help?

What’s Baptism?

I should be clear about this top hat deal. What’s the top hat about? Innovation? Excellence? Baptism?

Top hats tend to be symbols of success. But a Pamalogy Society top hat is not a declaration of success. It is a declaration of calling. It is a challenge. It is a reminder.

Declaring innovation means declaring change

That’s why I got baptized wearing my top hat. Baptism is not a declaration of success. It is a declaration of a new identity. Baptism goes beyond reinvention and human creativity. It applies hope and faith to something that it envisions and calls upon. Baptism knows what it sees in part but it doesn’t pretend to grasp it entirely just yet. Its calling may be unknowable, in fact, yet faith and hope may be part of a baptism sufficiently to know and trust that whatever is to come is good and that we are entering into it.

That’s how baptism works. Its power and declaration are incomprehensible in this world. Eye has not seen nor has ear heard it.

Why Dolphins?

Did that sound deep? As a philosopher, I ask big questions. One of them is what maximized awesomeness is. A theist will say God is maximized awesomeness. I agree. Maximized Awesomeness is exactly what God is. Perfection. You can’t get any better than that.

But when discussing philosophy, I aim for precision. I can’t be precise if the term “God” doesn’t mean the same thing for every person. It doesn’t.

I decided not to change my LinkedIn profile when I went into the insurance business.

Neither does the phrase, “maximized awesomeness” mean the same thing to everyone. Thank God for that. Now if I talk about mazimized awesomeness, for the sake of precision, I can consider each possible domain. How I can mazimize my awsomeness is one thing. How the world could maximize its awesomeness is another. Then there is what the best truth conceivable is – that is yet another thing. When we think about God, many of us think of that thing.

Maximized Awesomeness in that sense is that than which there could be nothing greater – a very specific description of God. That would be Perfection. But not everyone sees God as perfect. I wind up in discussions about why there is evil in creation. But that’s not what I’m going to talk about here. Here, I’m going to talk about dolphins.

A very smart looking dolphin. Don’t let convention fool you. Sometimes the smile is in the eyes.

Dolphins fall into the “this world” category of awesomeness.

Why do I like dolphins so much? Well … they are usually very friendly with us. They aren’t always friendly though. Some of them injure other animals. In fact, all of them do because they eat fish. Fish are animals. Manatees are much nicer.

Some people say animals don’t go to heaven. I don’t think that is true. I think the fundamental difference between humans and other animals is that we are more capable of intentionally knowing good from evil and seeking to change our behavior in order to seek the good and repent. We reject our own habits deliberately, purely for the sake of good.

I wouldn’t say animals can’t or never do consciously change their moral behavior. I’ve seen animals mourn. I’ve seen them groan with compassion. I’ve heard stories about them rescuing people. I’ve seen shame on dog’s faces. Who trained them to do that? Animals of many species often surprise us with kind and selfless acts. So why dolphins? It’s not their built in smile. That’s delightful but my dog gives me unconditional love too. Even my hamsters and guinea pigs loved me.

The Pamalogist’s top hat is distinguished by sprockets. The seven starred dolphin is another story.

You know what it is? It’s their blow hole. Like a person being baptized, they go under the water and come back up so they can keep on living. Whales and other sea mammals do the same, I know, but dolphins, being roughly the same size as humans, and having a brain size to body mass ratio that is even bigger than humans, symbolize baptism for me. We definitely have to wash that intelligent brain free of stinking thinking and dolphin brains are bigger than human brains. Seals are sea dogs – so cute and pretty smart too. But they don’t have special blow holes declaring to the world their need to breathe and be born again. Seals, otters and penguins, manatees – I know. They’re all cute. They’re all amazing. But dolphins …

Dolphins are my personal brand. I won’t ramble. Do you want to know about the seven stars? Maybe another time. Suffice it to say there is a reason the dolphin with seven stars is the brand I chose. Putting a top hat on it was a very personal thing for me. The seven stars may stay but the hat is not going to be part of my long term insurance company brand. It belongs to my philosophical society brand. If you are interested in my philosophical concepts, let’s talk about them. As for my insurance brand – I will simplify. Give it some time.

I’ve become an insurance agent. If I had my way, things would be very different. There would be no need for insurance – neither health insurance, nor life insurance. There would be some forms of property insurance, but that wouldn’t involve money. It would involve privilege and rights. It’s a long story. But I don’t mind sharing it. Do you have a moment?

Well, if you are interested in insurance as privilege, click here. That’ll take care of that. But to get to what drives me, I’ve got to start at the beginning. The drift of it all begins with the question of what is wrong with everything.

I’m serious. What is wrong with everything?

We don’t know the small, the large, the young or the old. Could pure reason explain it better?

You might think I’m asking a rhetorical question, but I am serious. And on a metaphysical level, I’m being literal – what is wrong with everything? And …

… what is everything to begin with? The particle physicists can’t even tell you what quarks are made of. The cosmologists don’t know how big or old the Universe is. How can we delve into what is wrong with everything if we don’t know what everything is?

We might also ask why everything is. Why?

As a philosopher, I think the answer to this second question provides the key to the first. The purpose of everything is the maximization of awesomeness. This is not just a catchy phrase. It is the actual reason. If you want to follow my reasoning and see how I came up with this answer, subscribe to Season One of my Podcast. I’m 100% serious.

So that takes care of that.

If you follow those links, you’ll see that I’ve covered a lot of ground I won’t have to repeat here. Let’s start with that context. Assume for a minute I’m right. If so, then the why question leads us to other big questions. Is what concerns us on a daily basis fufilling our purpose? If we are here to maximize awesomeness, then how? If your life is just, “blah” and “getting by” then does it concern you at all that you may have been missing out on something wonderful? Why is your answer not the maximization of your awesomeness?!

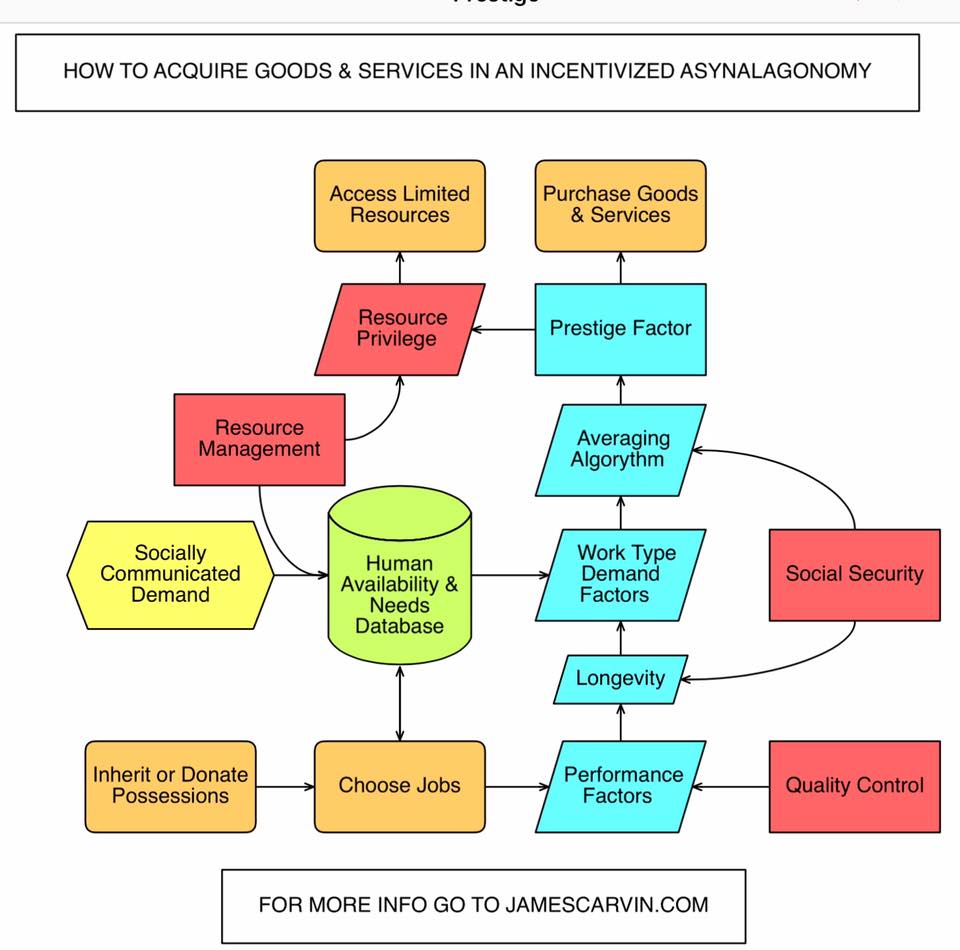

What if everything was very different? Imagine, for instance, if we had always lived in an incentivized asynalogonomy, rather than in the constant tension between capitalist and socialist dystopias. (Click here if you don’t know what that means).

There are better ways to deal with economic problems than plagues and wars. Just sayin’

If only more people knew about the HAND System. (Refer to the above link if you don’t know what the HAND System is). I believe that in the Multiverse, there are many Universes that incorporate the HAND System. I believe there are a vast number of worlds that aren’t nearly this dysfuntional. I’m presently in the insurance business because this world doesn’t know anything about the HAND System. They don’t know that it would fix this world much better than insurance ever could. People don’t know. So I have to settle for the insurance business.

I know that all sounds strange. I’m a little geeky, I know, but I’m not so other-worldly. In fact, I’m perfectly normal and safe to be around – just a little different than what you’re used to. And I can be practical. I may not be of this world, but I live as though I’m really in it. My philosophy holds that this world is at least partially real, even if it seems to be falling apart. Belief in the Multiverse as a product of Maximized Awesomeness does not make a person so other-worldly that they can be no earthly good. I see it as my mission to make this world a little less bad for people, if I can.

Other worldly leadership?

The Ghost Machine was another example of an attempt I made to maximize the good, as I knew how, given what I knew and thought I might be able. As with all of my business ventures, I started with the belief that it wouldn’t necessarily take money to make money. I still haven’t given up on that thought but I’m reminded daily of how pollyannic the concept is. I so much wanted that to be true. I had very little money. If I wanted to be in business for myslef, it would have to be true.

My father hadn’t wanted me to go into business for myself. He knew I wanted to have a positive impact in this world, one that required some entrepreneurial courage, but he wanted me to keep the good government job I had. He said that all the people he knew who’d gone into business for themselves had sacrificed a life without worry. Taking risks could rob a person of their time and of their health. He tried to spare me. He meant well. And I know he was right.

Dad spoke from his personal pain. He had lived in a very different world. It started well enough. He had inherited a fortune from his own father. He started out with a great career in textiles his Dad, my Pop Pop, Charles Carvin, Sr. had taught him. Dad became a marketing man in the textile industry. Even before his Allied Chemical days, he was doing commercials for Chemstrand. If you followed the Netflix series Madmen, you may have caught some of the flavor of my father. He had a trophy wife in Rye. He took the same train from Mamaroneck to Grand Central Station and back every day. “Draper” was even the name of one of his peer VPs at Allied.

One of Dad’s Chemstrand Commercials – images of home

I hope you enjoyed that video. Please watch it. See what I mean by “flavor”? And if you are really astute, you may have found the word, “Cumuloft” familiar too. Well, I should tell you that I was no more than one or two years old when the above commercial was made. Dad’s move to Allied’s Caprolan from Chemstrand was in 1962 and there was no more talk of any Cumuloft after that, if there ever was any in my presence. Assuming it wasn’t just a coincidence, somehow the term “Cumuloft” appears to have managed to stick in my young brain for forty years or so before I incorporated it into the Ghost Machine. The Cumuloft was the Ghost Machine’s “cloud” security storage system. Then one day, I decided to check to see if “Cumuloft” was a word I could trademark. The Internet didn’t show me anything at the turn of the Millennium, as I was developing the Ghost Machine’s blue prints. I only encountered my own father’s commercial, well after that search. I wonder what else is stored in my head without my knowledge. I don’t think we found this video until about 2016. Development of the mobile app started in 2011.

But I digress. Thinking about Dad can make my mind wander. I was talking to you about the insurance business. Specifically, I was thinking about how a person like me, who’s head is happier in the clouds, could possibly take interest in solving the problems inherant in dystopian economic systems. Insurance is a help. I was telling you it was the best I could do. At least it helps some people in this world. I’m sure there are many Universes much like this one where it comes in handy.

And I was telling you about the Ghost Machine. Like the insurance business, it would have put a bandaid on socio-capitalism. The idea was to create a fun way for people to make money. This world can be a very dull and even cruel place. Why isn’t earning a living easy and fun? It’s such a shame I was unable to raise the cash needed to build the Ghost Machine. The world would be a very different place right now if I had succeeded.

The Ghost Machine App Pokemon Go meets Bitcoin with some ghostly edutainment

At least in the insurance business I don’t have to start from scratch. There’s already billions and even trillions of dollars in this business. Getting my personal brokerage started has taken time, more than money. I was able to survive on rideshare earnings while getting my first few sales. It didn’t take hundreds of thousands of dollars.

But you deserve a little more back story.

Dad lost his fortune. My mom, who outlived him by decades, lived a miserly life after he passed. And she was spared the difficult ending to her life that my sister and brother had. She was in great health clear up to the age of ninety. Then she had a heart attack. She never had to pay for assisted living, much less a nursing facility.

Contrast that with my sister, Corinne. She had a stroke ten years before she died. The majority of her remaining years were spent on a feeding tube in a nursing home. Her husband abandoned her. Her four remaining brothers deliberated over her care. One wanted to put her on palitative care and another thought she wouldn’t want that and the right thing to do was to bring her to a new nursing home in Tallahassee. He prevailed. And that is why we moved here – to watch over her before she died.

My wife, six years my younger, also had had a stroke the year before my sister, six years my elder. She was only thirty eight. She’d been in perfect health until it happened in 2004 but she’s been paralyzed in her left side ever since. It shows me that bad things can happen to anyone at any time. Jeanne Calment, who according to the Guiness Book of World Records is the oldest documented woman to ever live, was a smoker. Lisa never smoked, drank or took drugs and she worked out regularly. Bad things happen to good people. It doesn’t matter how rare it is. It happens. And that is why we have insurance.

We still had some good times after Lisa’s stroke even when we had no money. Hardship is bad. But you can work through it.

With that picture, it may make better sense why an inventive philosopher would wind up in the insurance business. It positions me to help people deal with the hard realities that exist when bad health, or death, comes at an unexpected time. We can deal with problems before they happen. I can’t prevent an occult arterio-veinous malformation, like Lisa’s, from bursting. But I can make it easier for families to deal with the financial issues that ensue if and when such a thing happens.

And it wasn’t just Lisa, or my sister Corinne. Do you know what was really eye-opening to me? It was visiting Corinne in that nursing home. Nursing homes are places filled with people suffering. I wish more people knew. Maybe they would visit them. There is so much loneliness there.

And they need care. They shouldn’t go without much needed care. Caregiving takes money.

I don’t mean family caregivers. Lord knows I’ve never been paid for family caregiving and few have. Maybe we all should have been and maybe there are even some insurance plans, ones that I can even write for, that actually cover that to some extent. If anyone would know about those plans, I would. But what I mainly mean is professional nurses, doctors, medications and treatments. It all has to be paid for.

So, I’ve decided that the best way for me to maximize my personal awesomeness, is to learn all I can about health insurance for young and old. And life insurance too. When I was young, I had my days of fun and adventure. I have no shortage of stories to tell. But I continue to ask how I can do the most good for the most people – not just myself – before I die. I continue to focus the answer on the areas I would be most capable of. I still have a few brain cells left. Let me see what I can dig up for you. You have not because you ask not.

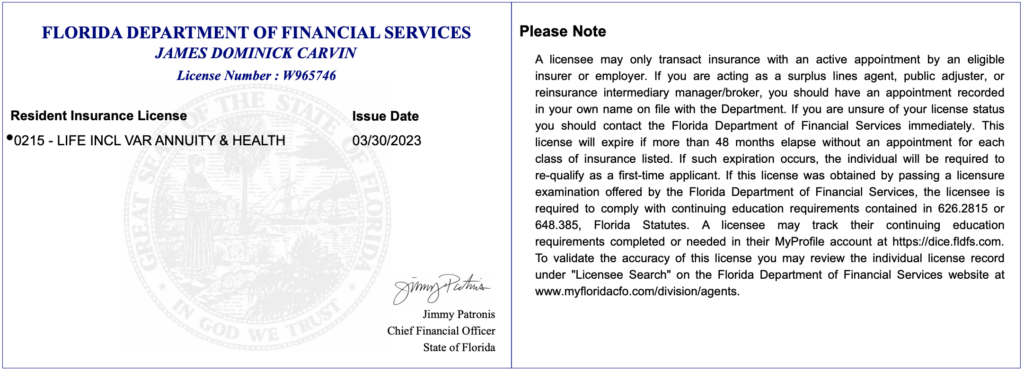

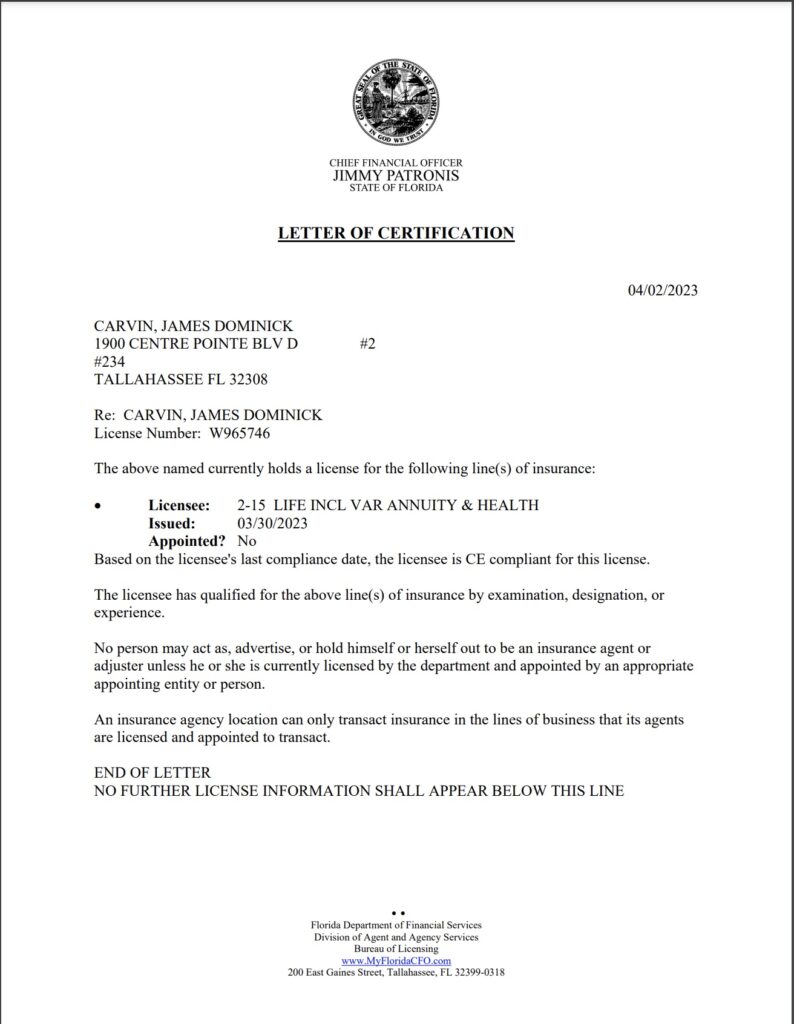

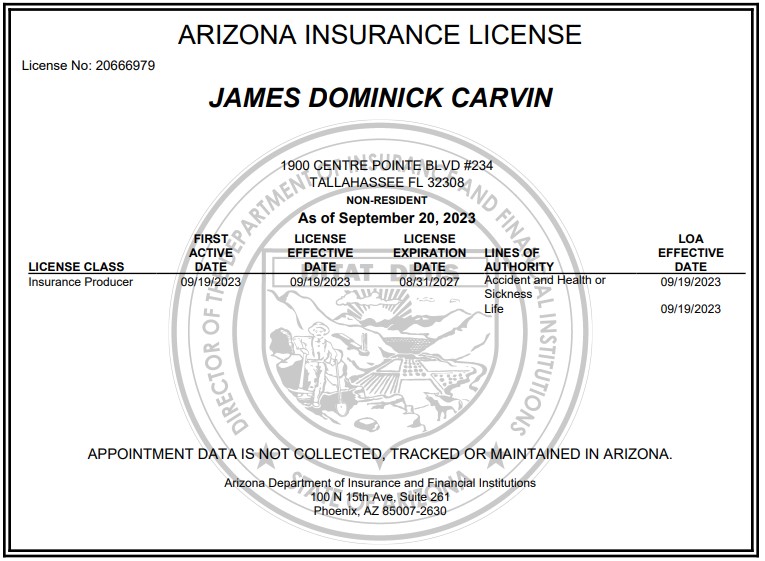

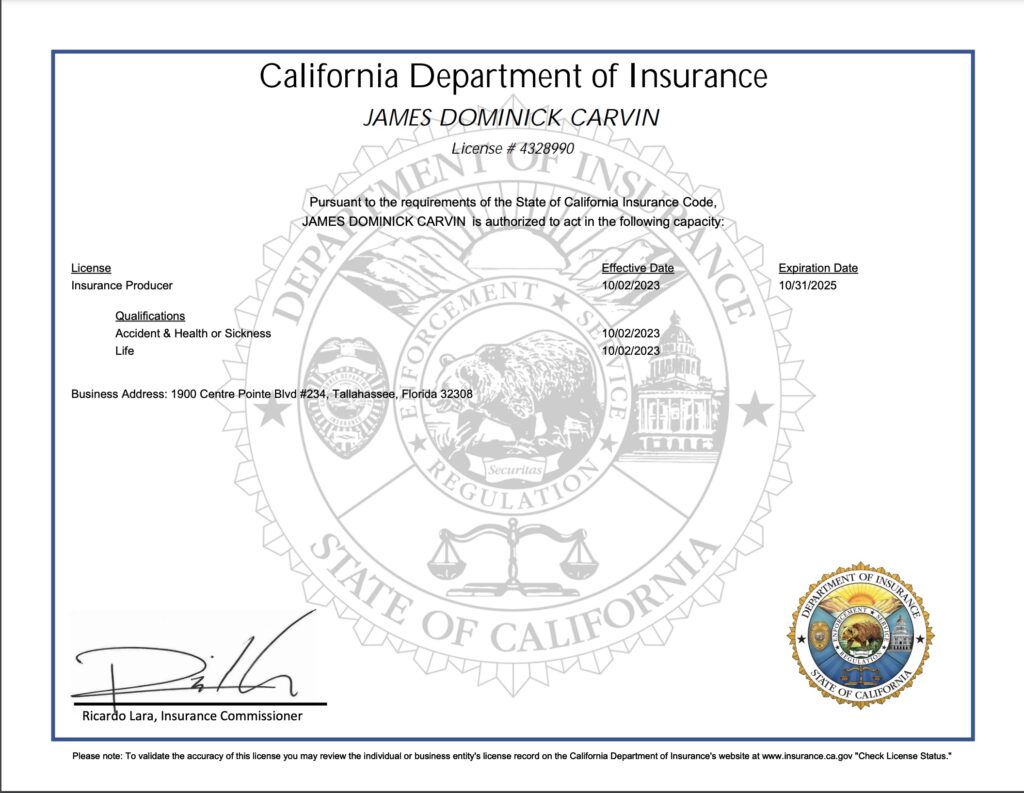

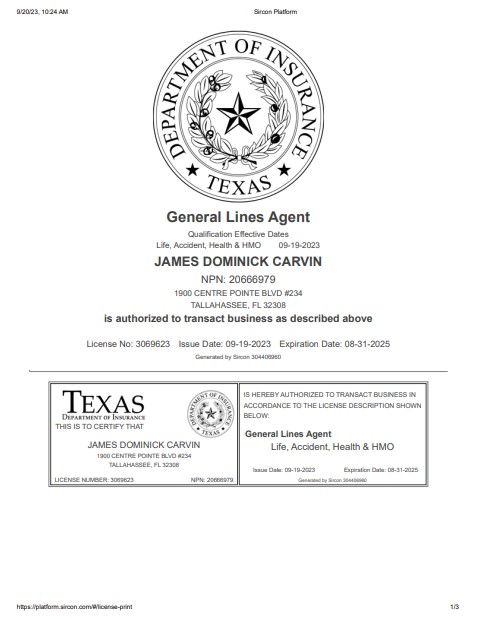

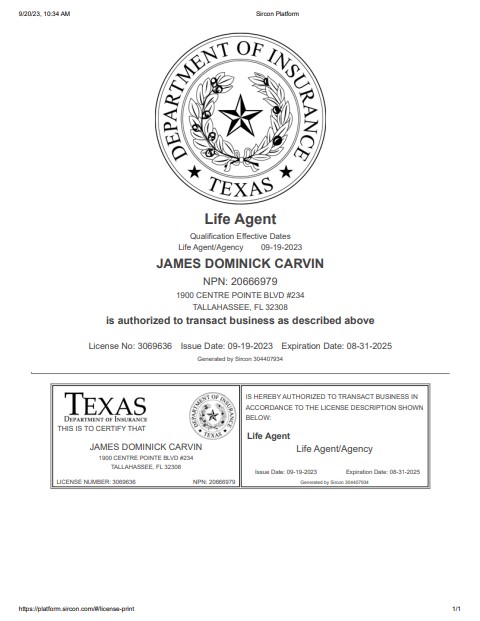

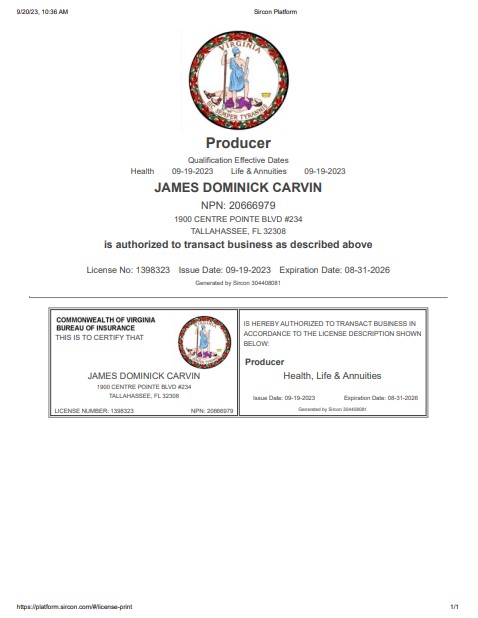

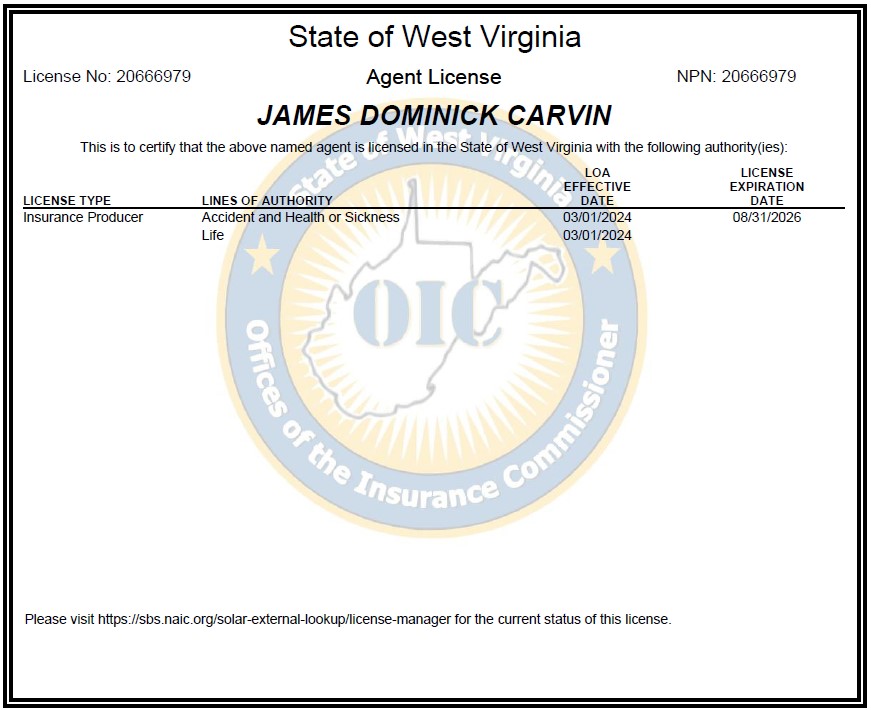

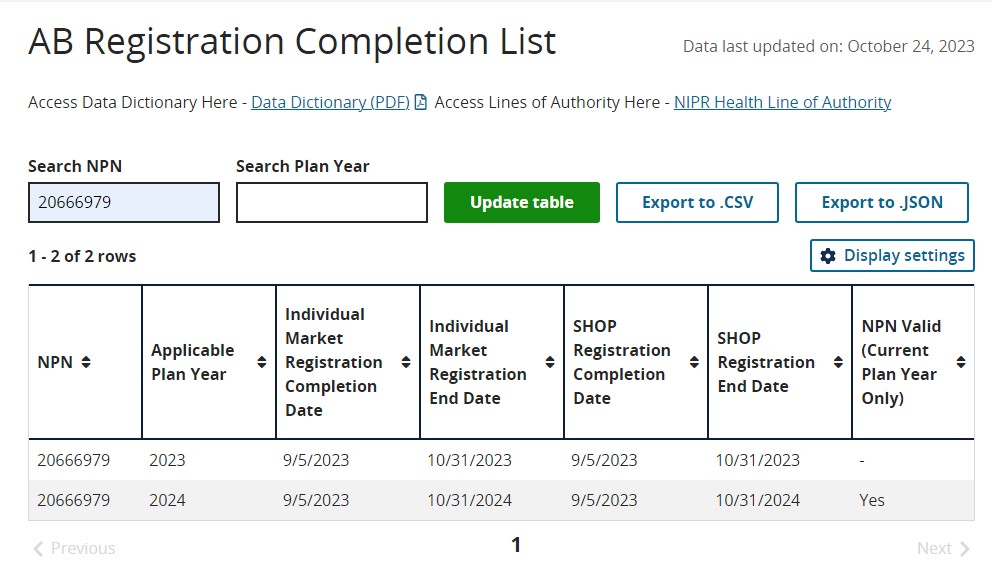

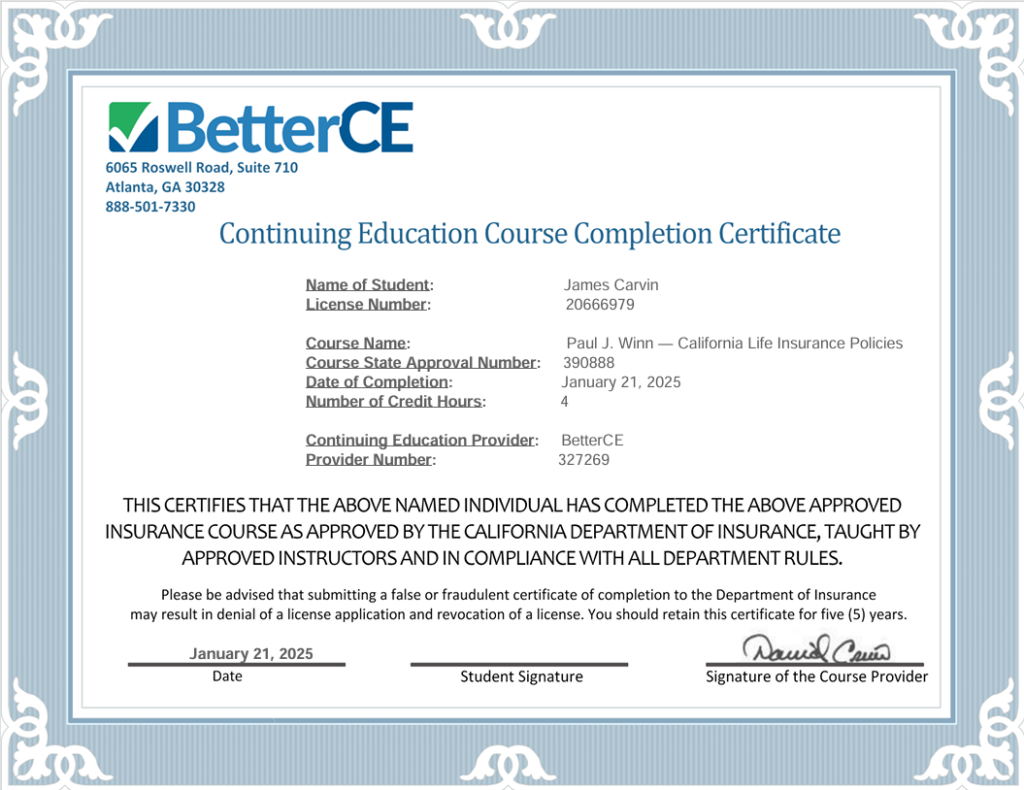

I am an independent life, accident and health insurance producing agent based in Florida, licensed in multiple states:

Arizona (20666979)

California (4328990)

Florida (W965746)

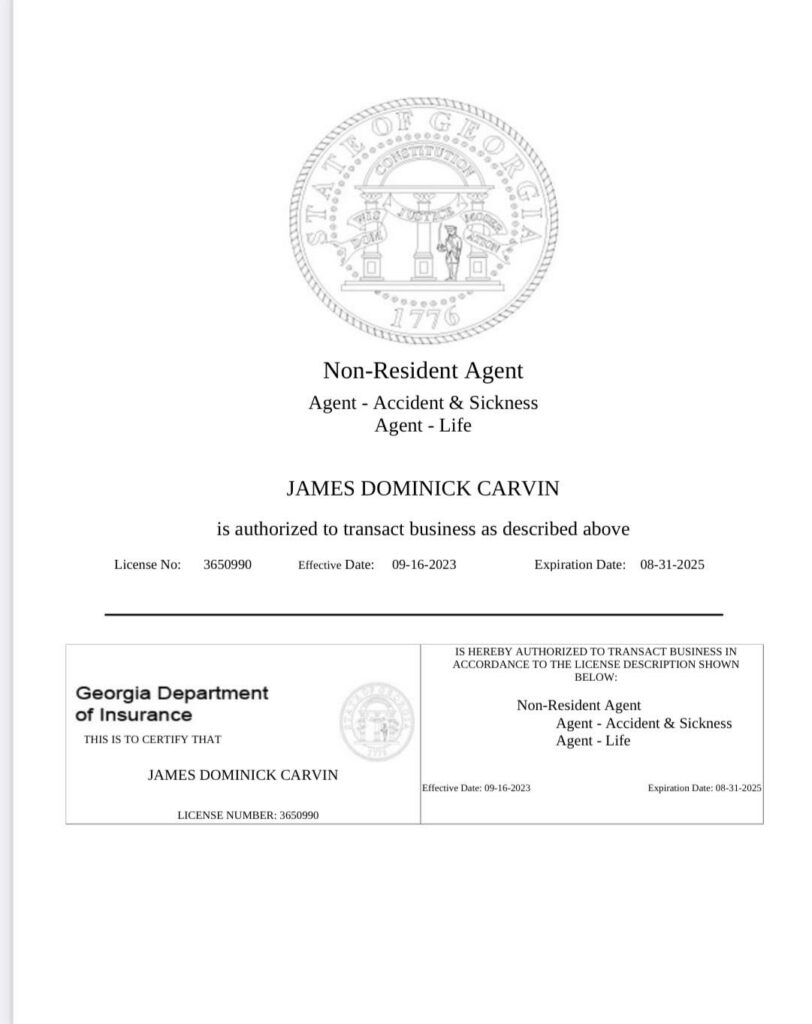

Georgia (3650990)

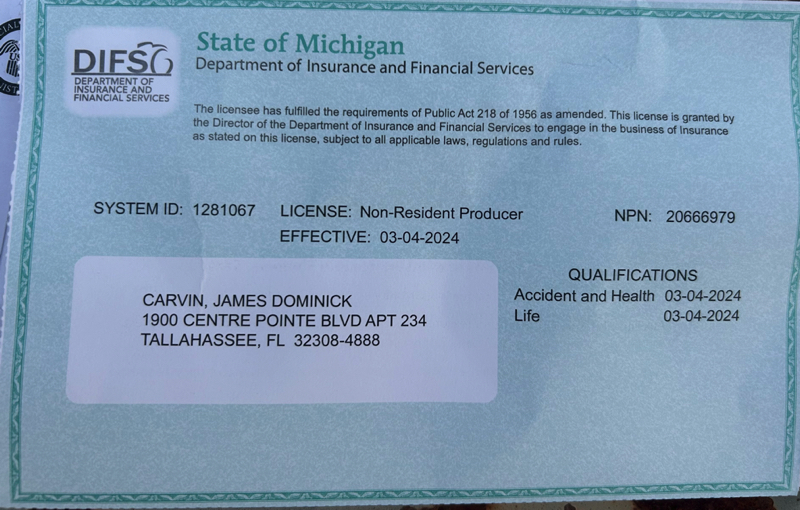

Michigan (20666979)

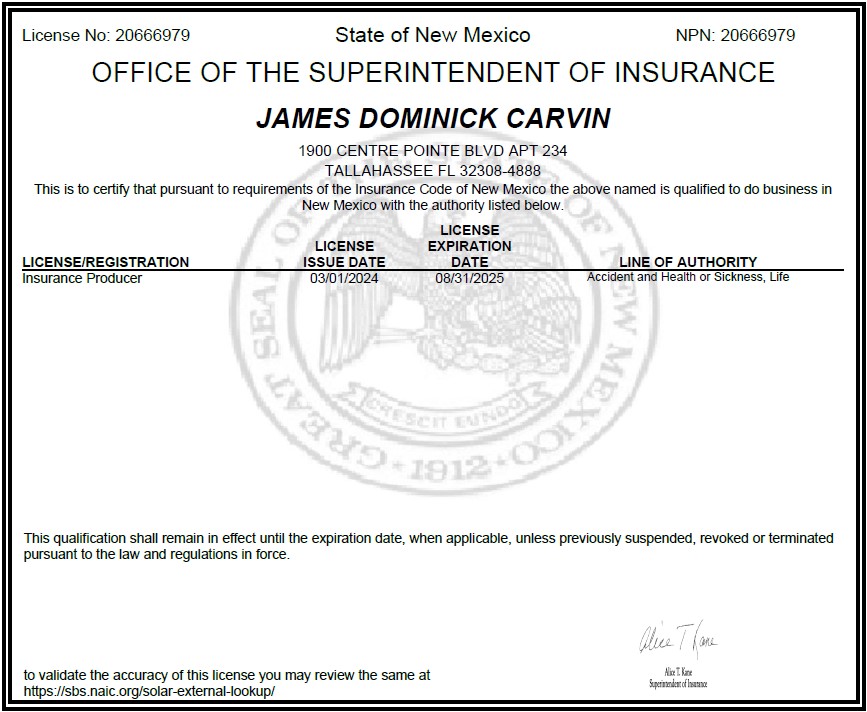

New Mexico (20666979)

South Dakota (40718581)

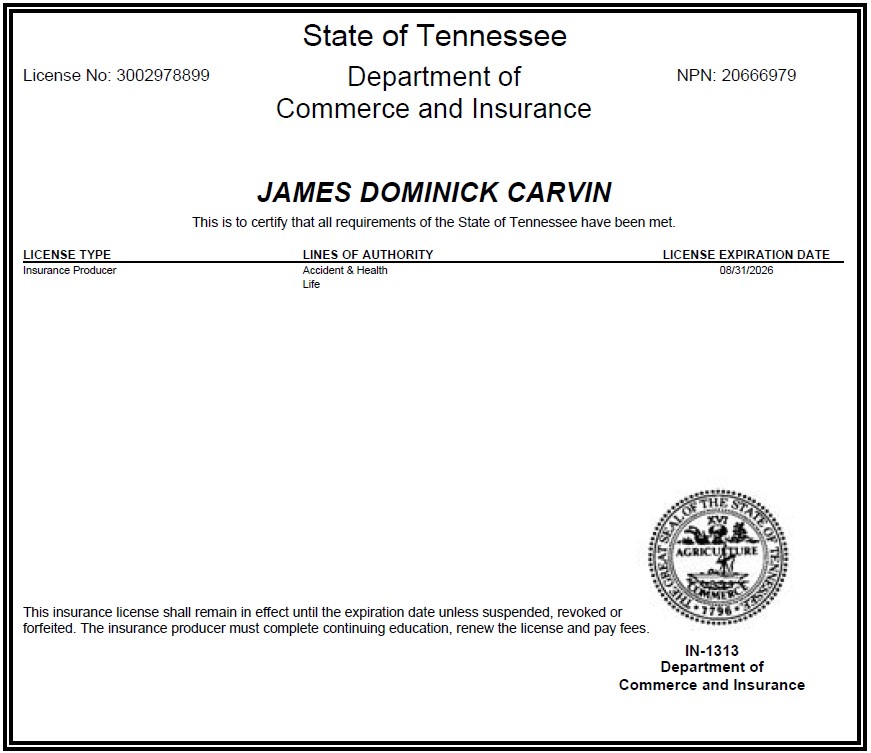

Tennessee (3002978899)

Texas (3069623/3069636)

Virginia (1398323)

West Virginia (20666979).

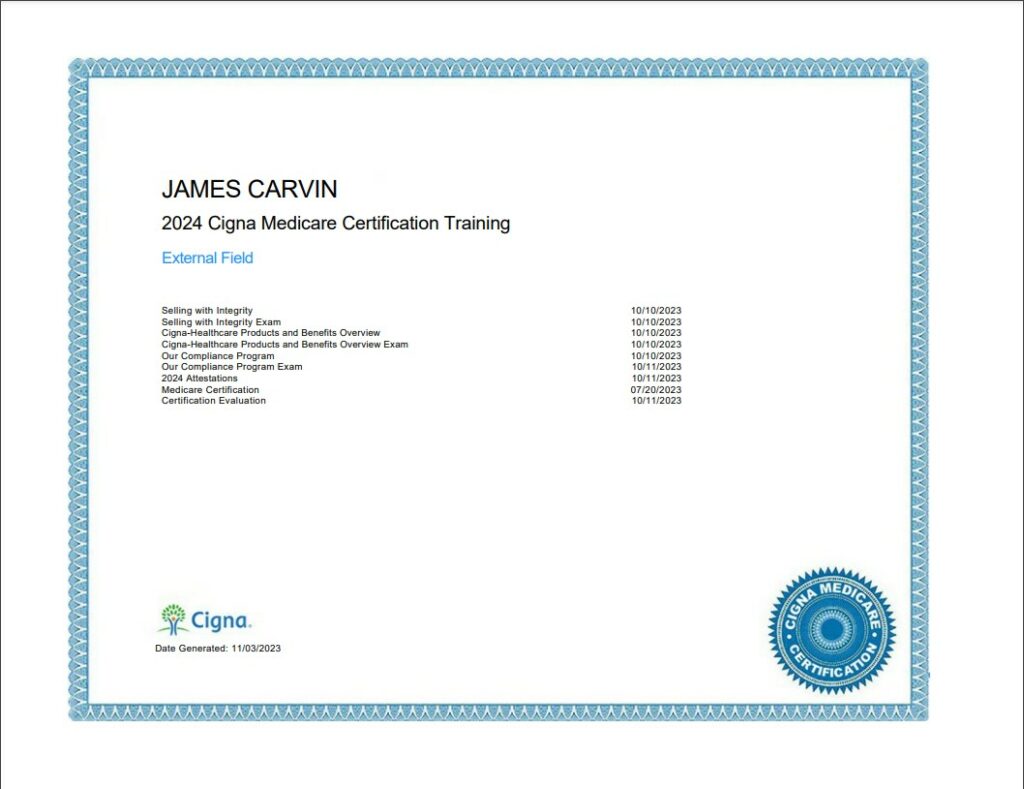

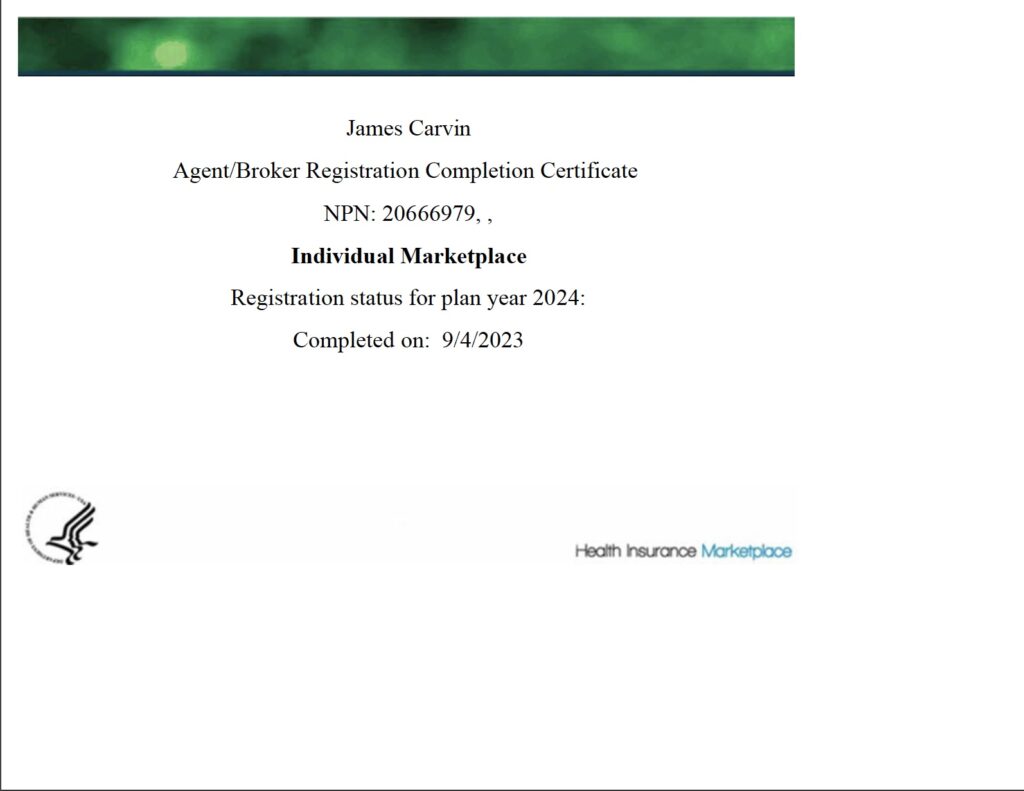

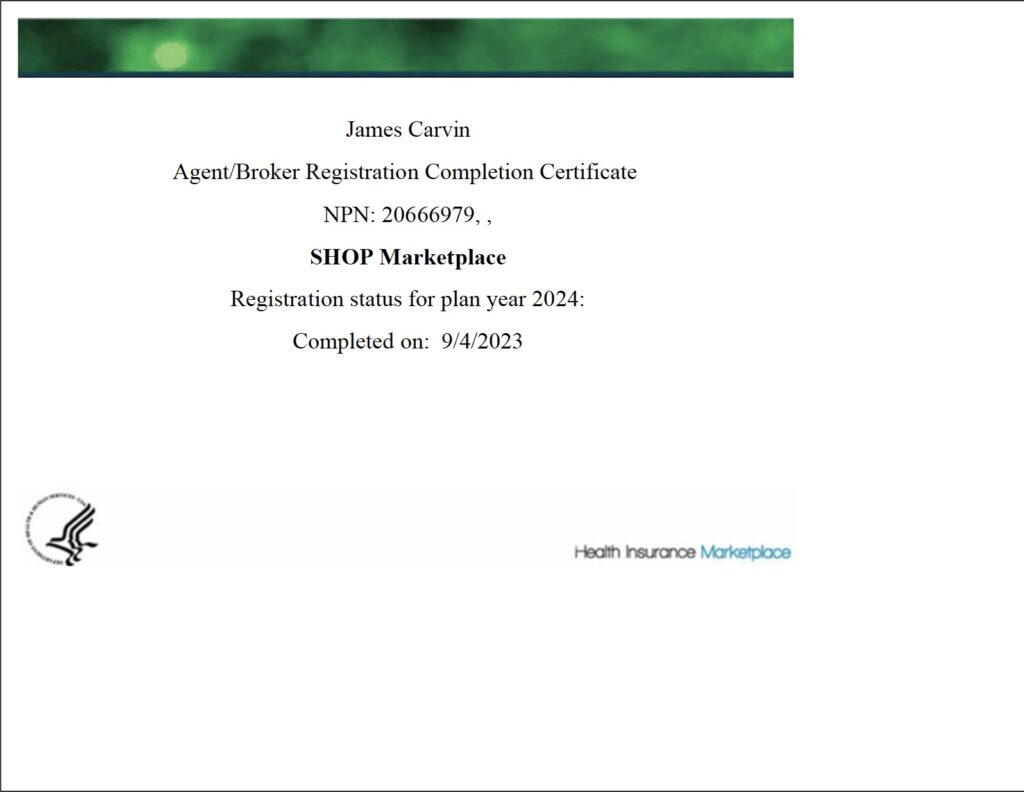

My license information and up-to-date certifications for continuing education requirements are included below for those who may need to check my credentials and eligibility.

NON-RESIDENT LICENCES

As my business expands, I will continue to add state life and health insurance licenses to this page. All licenses and certifications listed here are current.

Michigan 20666979

Medicare Certifications

Marketplace Certifications (ACA/FFM)

About Me

I got into the life insurance business in my sixties after graduating from Arizona State University with a 4.0 average. My degree was in Interdisciplinary Studies with concentrations in Organizational Leadership and Philosophy. I already had a degree in Music Composition from the University of South Carolina that I’d earned in 1980 while on a springboard diving scholarship. And then after that I earned a theology degree, as well, after six years of study in two small colleges in South Florida – St. Vincent de Paul Seminary and St. Michael Academy, where I also served as an adjunct professor. I am a highly dedicated, very detail oriented person, who loves to teach and lead. JamesCarvin.com is a comprehensive web site that tells you not just about my life and health insurance brokerage but about my philosophical and entrepreneurial endeavors. Last year I completed Season One of my Awesomeology solo podcast. I’m currently looking for a co-host for Season Two. My motto is “Maximized Awesomeness.”

James Carvin, 1981

I am an Independent Broker working with Multiple Carriers and Plans.

I am not captive to one company or plan. I work with you as an independent broker to assess your family’s needs and goals. Many people ask for quotes when what they really need is guidance. Being independent enables me to do this.

There are three major marketing organizations I work with. Each contracts with multiple carriers to serve as many needs as possible. I do not have contracts with every carrier that these IMOs serve:

Family First Life – FFL contracts with a majority of A-rated life insurance companies, as assessed by AM Best, Fitch, Moody’s and Standard & Poor’s. I personally scan through ninety five A-rated carriers to find you the cheapest plan within your budget using FFL’s unique tools. FFL specializes in whole life, term, mortgage protection, children’s policies, annuities, IUL’s and accidental insurance.

Benzy – Benzy has contracts with well known carriers to provide health matching accounts and private indemnity plans that cover hospital costs, accidents, illness and out of pocket expenses from dental, health, vision, cancer, heart attack and stroke. Their ideal clients are in generally good health and they don’t benefit much from ACA tax benefits or cost sharing from the health marketplace. If you’ve been paying high premiums, high deductibles, high copays and astronomical cost sharing on top of that, then I can help you eliminate it through an indemnity plan and a health matching account. Benzy specializes in private health plans that don’t pass the high costs of pre-existing conditions and predictable expenses like pregnancy onto other members of the network, as is the case with ACA plans and other comprehensive medical plans.

Kellogg – Kellogg Insurance is my marketing portal for traditional comprehensive health plans and plans for seniors. Whether you qualify for accelerated tax credits and cost sharing due to your lower income, or you have pre-existing conditions or you are in your silver years, Kellogg has provided me the organizational power and training to help me help you.

In any of these areas, it is my goal to help you locate the ideal product for your personal, needs, qualifications and budget. Please note that I have contracts with many but not every carrier and my portfolio of products continues to improve over time as do the number of markets I serve.

Arrange a Consultation

If you are married, it is advisable that your spouse be present and attentive.

Carriers require payment and other sensitive information to set up monthly payments and check medical history for simplified underwriting.

Bloodwork and labs are not required for the majority of policies.

If you live in the Tallahassee vacinity, I am happy to accomodate those who prefer in-home consultations up to about fifty miles in any direction. Most of my work is over the phone or on Zoom. When signing electronically, many carriers will require an active email address and/or text. If you don’t have Zoom, I can share screens using your desktop or laptop’s browser. Typically over the phone there will be a discovery call followed by a plan call. Some carriers may require recording all contact and a 48 hour advance appointment using a scope of appointment form. To arrange a consultation of any type, click here.

Note: (1) In-Home consultations are only available within a fifty mile radius of Tallahassee. (2) Telephone consultations will be recorded and records kept ten years where required by law. (3) On-line consultations utilize Zoom or other video presentation technology and will require that you open a link sent to your email. On-line consultations are also recorded.

How to Proceed:

Step One: Read the instructions on how to prepare for our consultation. Step Two: Read and agree to the disclaimer. Step Three: Click on the link below that corresponds to the consultation method that you prefer – In-Home, By-Phone or On-Line.

Understand who I am and what I can do that others can’t. First, as an independent broker, I am not captive to one company or plan. I offer many. I will help you compare your options and meet your goals. Second, I don’t just offer health plans. I also offer life insurance and annuities, mortgage protection and long term care with the best rated carriers. I offer group health and life plans as well as wellness and workers comp. I offer individual and family health plans. I help those in financial need and those with pre-existing conditions. I help business owners and high income earners as well as those with special needs who may qualify for subsidies. I offer both ACA and private plans. Whether or not you have pre-existing conditions or you are a low income earner, I can help. I also offer both traditional Medicare and Medicare Advantage Plans. I offer Medicare Supplemental plans and Prescription Drug Plans. We will discuss your needs and I will help find the solution. That’s who I am and what I do. That’s why it is called consulting rather than sales. Prepare mentally for a very helpful consultation. I am going to help you and direct you to the best plan for your expressed needs. Make time for me.

Different types of meetings require different types of preparation. If we are discussing health plans, I won’t need all your prescription information, but if we are discussing life insurance, I will, so I can compare pricing and value and see which programs you qualify for. For health, since there are laws against discrimination, I can’t ask those questions. However, you will be interested in pricing and I am permitted to answer any questions you have about the cost of certain drugs or the availability of specialists and primary care physicians in a plan’s network. Prepare a list of questions. If you are on Medicare, have your Medicare card ready. If you are enrolling in Medicare for the first time, prepare by applying online at least two weeks before our meeting at SSA.gov so you can have your card before we meet. You must be enrolled in both Part A and Part B to qualify for a Medicare Advantage program. Check your card to make sure you are in both. If not, head to SSA.gov to get enrolled into Plan B.

Whether our consultation is about life or health insurance, have any existing policies you have available for review and comparison and have your banking info ready so I can enroll you into a plan, if needed. Normally payments are made monthly and you can select a date for your payments. You may also choose a different mode of payment, such as quarterly, semi-annually or annually, and select a start date for your plan. Some carriers may require your drivers license. Most require your social security number. For life insurance policies, have available the addresses and dates of birth of any beneficiaries. Most carriers won’t require the social security numbers or emails of your beneficiaries but those are helpful to provide just in case. The social security number prevents confusion about people with the same name. The email address and phone number of the beneficiary helps with notification in the event of your death. Having all this available before our meeting will speed things up tremendously.

If the meeting is about Medicare plans, (as opposed to a general discussion of Medicare not involving plan specifics), then you will have to submit a Scope of Appointment form (SOA) at least 48 hours prior to our meeting. Be aware that at any meeting discussing Medicare plans, I will not be permitted to discuss life insurance or ACA plans by law. Our conversation will have to be limited to what you check off on the Scope of Appointment form and the meeting will be recorded. The only meetings that won’t be recorded are face-to-face meetings. On-line consultations will be recorded on Zoom or other media as required by law. Virtual appointments do not legally qualify as face-to-face meetings according to the Center for Medicare and Medicaid Services. If you do not wish to be recorded, it is only required for Medicare. Let me know in advance of the call if you do not wish to be recorded and so long as it is not out of compliance, I will arrange to talk on an unrecorded line.

Timing matters. Prepare for enrollment periods by knowing when they are and whether they apply. Life insurance is best bought while young and healthy because its cheaper and has more value that way but it doesn’t have any enrollment period restrictions so much as plans that you’ll only qualify for at certain ages. Health Insurance involves enrollment periods you do need to be aware of and Medicare enrollment periods are different than Non-Medicare enrollments. The three main dates on Medicare to know are (1) the Annual Enrollment (AEP) Oct. 15th – Dec. 7th, which allows you to start new plans or change plans and make as many changes as you want (2) the Open Enrollment Period (OEP) Jan. 1st – Mar. 31st, when you can make one change to a Medicare Advantage plan and (3) Special Enrollment Periods (SEPs) throughout the year that can be triggered by events such as coming in and out of an institution or coming on or off Medicaid, discontinued plans or change of address that makes you lose your network. For ACA health plans, open enrollment is from Nov. 1st – Jan 15th and similarly there are Special Enrollment Periods throughout the year. Some indemnity plans and ancillary services aren’t subject to enrollment period restrictions. Be sure to ask me about indemnity plans as they are often the key to eliminating your out of pocket costs. Understand that it is my goal to reduce or eliminate your medical expenses entirely, if possible. And sometimes it is. You just need to know what to look for. Book me.

By completing this consultation scheduler tool, you agree that you have read and understood the following disclaimer:

DISCLAIMER:

1 ~ If you are NOT seeking Medicare or Medicare options such as supplementary insurance or Medicare Advantage or a Medicare Prescription Drug Plan or equivalent, DO NOT check the Medicare Disclaimer on the Scheduling tool.

2 ~ If you ARE seeking Medicare or Medicare options such as supplementary insurance or Medicare Advantage or a Medicare Prescription Drug Plan or equivalent, then YOU MUST check the Medicare Disclaimer on the Scheduling tool and the following disclaimers below shall apply:

2.1 ~ NOT AFFILIATED WITH OR ENDORSED BY THE GOVERNMENT OR FEDERAL MEDICARE PROGRAM.

2.2 ~ Participating sales agencies represent Medicare Advantage [HMO, PPO, PFFS, and PDP] organizations that are contracted with Medicare. Enrollment depends on the plan’s contract renewal.

2.3 ~ I do not offer every plan available in your area. Currently I represent 4 organizations in Tallahassee which offer 18 plans.Please contact Medicare.gov, 1‑800‑MEDICARE, or your local

State Health Insurance Program to get information on all of your options.

I should add some thoughts that help summarize my thinking. One of my goals in offering better health plans is to help families build legacies. If you have read my blog you know how important legacies are to me. A legacy is what you leave to the world after you die. Typically your family is most affected by your presence or absence. Some manage to build foundations and have more long term benefit to the world that survives them. Unfortunately, many legacies are destroyed by a simple failure to check their policies. Often the people that I meet are too embarassed to admit that they may never have checked their policy at work, or the fine print on a policy they picked up at the funeral home or got in the mail. We trust our employers and we are too busy to sort through anything with a lot of fine print on it. This is probably a bigger problem with life insurance policies than health insurance but it applies to both. The simple fact of the matter is that many policies don’t deliver what peo0ple think they do. Let’s check.

If you have access to your existing policies, please have these ready to review when I arrive so we can determine whether you should keep, cancel or modify them. If you do not know which carrier your policies are with or what your current premiums are, check your bank statements. If you are not making payments monthly, you probably don’t have a policy. If you don’t have a copy of your policy, show me the phone number on the bank statement where you are making your payment when I arrive. For life insurance policies, I will make sure that both you and your beneficiaries have a copy of all of your policies before I leave. For health insurance, you ought to have a card. If not, then what will you do if you get sick or have an accident? If a life insurance policy is with an employer, you probably do not have a policy since you don’t own it. Instead, you may have a certificate. Employer life insurance policies often offer far less than what employees assume they do. Did you read my story about Bob and Sally? The same is also the case with PreNeeds policies, renewable term policies, graded and guaranteed issue policies. I will discuss this with you when I arrive. Let me see them.

Location Matters

Once again, all in-home consultations must be in the greater Tallahassee, Florida region, where I live, or possibly Southern Georgia, where I’m also licensed. If you live outside of the Big Bend region or far from town, I prefer to help you by Zoom rather than by phone, so I can see you and you can show me your policies, if you have any. I also prefer to see the faces of the people I help. Visit my Licenses & Certifications page to see which states I am authorized to serve families in.

Be aware that I am not licensed in every state and not every carrier offers the same products in every state. Health insurance is also limited to networks. However, if you are not a Florida resident, in most cases, depending on the type of product, I can still help you. Be sure to let me know what state you are an official resident of before booking your session with me, so I can prepare for our meeting in advance. Otherwise, I will assume that the address you list is the address of your official residence. Florida residency requires that you generally live at your address for 180 days out of the year or more. A Florida drivers license is normally sufficient to establish that you are a resident. If I am not licensed in your state, please let me know where you are. I am always interested in expanding and need to monitor demand.

Every Monday and Thursday I spend all day booking appointments to help families with their life and final expenses. I like to meet families face-to-face when I can. It helps me know who I’m helping. I literally love helping people. It gives me a sense of purpose. And I love the way people think about the people they love. It renews my faith in humanity. But a lot of people won’t let me help them because they are confused. This is a very serious problem. So, today I’m going to clear up this confusion by addressing the twelve most common erroneous assumptions people make about me when I call to book an appointment, almost always hurting those they care about in the process.

Tap on the insurance myth that describes what you were thinking when you hung up …

Look at the list below. Click on the myth that describes your last conversation with a life insurance broker like me. It will show you what we were thinking when you told us you didn’t want our business and hung up …

Watch the video below that fits. And then if you want to become a quick expert on life and final expense insurance, watch the rest. When you’re ready to do business, fill out the form at the bottom of this page to book an appointment. Then after I’ve helped you, join in the fun and satisfaction I get out of all this by sharing this page with your friends. 🙂

Myth #1 – I am a telemarketer.

If I am calling you, there is only one reason I’m doing it. You requested information. I don’t make cold calls. Now to be sure, depending on how the request came in, there may be more than one agent who follows up on it, but more often than not, people looking to protect their loved ones will make the mistake of submitting multiple inquiries while it is on their mind. That can trigger a flurry of never-ending phone calls. Even if you just filled out one online form to the wrong place, many agents will call, rather than one. And the problem just begins there. Something that makes me even angrier is that social media, Google, and other generic sources, will often sell “leads.” In fact, big data, as it is called, is even known to resell the same leads to multiple buyers.

I respond when you’ve contacted me for help. Do you know how frustrating this is?

So here is my reality. I don’t ever know when any of that has happened when I call. If you’ve received too many calls, then you’ll hang up on me, thinking I’m a telemarketer. At that point, I can pretty much guess the reason, but by then it’s too late. Of course, I can totally relate. I hate to get sales calls too. It drives me bananas. I don’t blame you for hanging up, or even cussing me out in the process. What does bother me most though, is that I’m not helping someone. I happen to know that more often than not, people actually do need my help. They just don’t know it. And when they hang up on me, I’m not given the chance to help them.

While some people are natural-born salesman, I am not. I stutter when I speak. And the older I get, the more pauses there are as I search for words. Plus, I have ADHD and easily move off topic. I’m the opposite of a smooth talker and I’m no extrovert. If I make a video, I’ll have to edit it a lot just to speed it up to a normal pace and remove the ands and ums. I can also write. At least I can do that. I know this about myself. That’s why when I graduated from ASU and started to get offers from Insurance companies, I didn’t apply. I knew they needed smooth talkers to push their one-size-fits-all products onto people that those products might not be best suited for.

It seemed both better suited to my own personality and to my sense of ethics, to be in the business of helping people find what they needed, rather than to convince them they needed what I happened to sell.

Salesmen and consultants are two very different things. I’m not a captive agent!

You should know how this works. I am in business for myself. I’m an independent agent who works with dozens of companies that each has many products. Most agents work for insurance companies as employees. Those agents are very limited in what they can offer you and they have to sell one-size-fits all policies. Very typically, those policies will not be in your family’s best interest. Me, I make a great teacher. I prefer to help someone shop and make the best decision. My role is that of a consultant. I save you time because I can connect you to the products that will help you the most within your budget. If you ultimately are able to find an insurance product that gives you more coverage, or the same coverage for a lower price than I can find you, I will thank you for finding that for me and seek out that company so I can contract with them to provide that product to any future clients I have that fit your profile. But that rarely happens because I’m plugged into a very sophisticated system that has already done most of that work for you. I already have contracts with all the best A-rated carriers.

Look. Let’s be realistic. I’m here to help people – not waste my time or yours. If a letter doesn’t have a first class stamp in my house, it’s going into my trash. How about you? And if it’s going to my email, I’m probably going to delete it. How much of your junk email do you read?

What good would a quote for a policy you didn’t qualify for do you?

But even if that wasn’t the case … even if you did read it, what would I send you? I need to know what you need first. And I need to know what you qualify for. Otherwise, you’ll be shopping for something you can never have. Do you want a multi-million dollar mansion? So do I, but if I don’t qualify for it, I won’t waste my time, or my realtor’s, trying to buy it. That realtor is going to prequalify me. Until I’m prequalified, they won’t even talk to me. So, ask yourself this question: how much time and effort does getting prequalified to buy a home take you? You have to supply bank statements. Don’t you? You have to have a credit look up. Right? That means you have to give them your social security number and your bank account info. Doesn’t it? Yes, it does. And you’ll need to verify your identity with something, probably a driver’s license. I’m going to need certain information too.

It won’t be quite as detailed as buying a home, but I can’t give you a quote without knowing what you qualify for. You should be aware that that’s going to happen no matter where you go for insurance. If you do get a quote without that information, there will be a catch. I’ve warned you. Beware. I do want to give you a quote, but I’m going to have to prequalify you first. That should take about ten or fifteen minutes. Most of the information you need, like what prescriptions you take, will be at your home. That’s one of the reasons I prefer in-home appointments. Sound fair?

By the time I reach you, it’s always possible that you’ve already bought insurance, but when I’m calling back about the information you’ve requested and you tell me you’re not interested, I’m going to think that either you tried to get insurance somewhere but weren’t qualified, or that you did qualify but it was too expensive, maybe somebody already came over to help you, or maybe you bought something you found in the mail. I’m not going to think you weren’t interested. That would mean you didn’t care about your family and at some point you were asking about benefits for them. I’m assuming you just don’t want to talk about it.

There are people you love. Don’t tell me you weren’t even curious.

So, put yourself in my shoes for a moment. When you tell me you are not interested, expect me to ask you why you changed your mind. And if you do give me time to ask you that before hanging up, please try to understand why I’m asking. I’m asking because I care. And I care because I know that in every one of the most likely explanations I just mentioned, it’s most probable that you could have made a better decision. What’s more, if you would just give me the time, I would be able to show you how to correct it. And that could make a huge difference both for you and for those you love. The most common underlying reason is that you already took care of it and just don’t want to talk.

Caring for those you love is something you maintain and double-check. It’s not something you don’t periodically review, and I want you to really think about this. If you had a child who was sick, you would take them to the doctor. And if the doctor gave you a certain drug you had never heard of before, would you trust them? Or would you trust your friend who used home remedies? Even if you had a doctor, if your child was about to die and needed surgery or some difficult treatment, wouldn’t you seek a second opinion? Of course you would. You haven’t taken care of your child if you haven’t consulted a licensed professional. And even if you have, you haven’t taken care of them without a second opinion. You allow your doctor to revise your prescriptions. Allow a licensed independent agent to review your policies. You are not truly taking care of your family if you don’t. So, you haven’t really taken care of it.

Here’s what an insurance broker is thinking when you say you already took care of it

Now these days, a lot of people go to Google to learn a lot of things and people self-prescribe the right thing more often than they used to. And that’s a good thing often enough, especially for those who avoid doctors because of medical bills. But second opinions from independent life insurance agents cost you nothing. An agent like me will check your policies without charge because more often than not we will be able to make a significant improvement over your current policy – either qualifying you, when you couldn’t qualify before, or getting you more coverage for the same price, or perhaps the same coverage at a significantly lower price.

And it involves much more than mere price. It also involves misunderstanding. Check through the other myths I’ve singled out here. For those who’ve already purchased insurance policies, it is very common for people to think they have more coverage than they actually do, or to think that a policy is much cheaper than it actually is. Be sure to watch all of the myth busting videos on this page and see for yourself what I mean. Even if you have already taken care of it, then share this page with a friend who probably hasn’t. Even if you’ve truly taken care of your family, have you cared for your friends? Share this with them.

Employers contribute to health care plans and sometimes offer life insurance policies as a benefit, in addition to retirement plans. However, there are several things you should be aware of before relying on an employer’s insurance plan for either your health or to protect your loved ones when you pass away or if you become disabled.

First, be sure your company’s life insurance is not “key employee” insurance. Key employee insurance is not a policy for you or your family as a beneficiary. It is a policy taken out on you with the employer as the beneficiary. It keeps a business running when a key employee dies. It does nothing to help the employee’s family at all in the event of their death.

Let a licensed professional review the life insurance policy your employer is providing.

Second, only a handful of employers anywhere offer individual policies for their employees. Most often, if they offer life insurance at all, they will offer group term policies that will lapse when an employee is no longer able to work, which is unfortunately typical if an employee suffers from a long term illness. It is very tragic, but when an employee gets a fatal disease and is unable to return to work for a given period of time, usually just thirty days, they may be able to extend their health benefits if they personally contribute to a COBRA policy, but the life policy will not be offered without a health examination. Of course, no one with a terminal illness will qualify for a life insurance policy. Unless your employer is offering a whole life policy that is portable, your employer’s life insurance policy will be of no value to your family.

Third, you should own your own policy. Even if your employer was providing you with fully portable whole life policies, they could still decide to cancel every policy every employee had at any time, all in one group fell-swoop. If its going through an aggressive hiring phase, an employer might over-buy benefits to attract new employees. But if it is going through a lay-off phase, it will typically choose to trim benefits rather than lay off employees. Your family matters too much for that sort of risk.

The bottom line is that you should own your own policy – not rely on an employer’s policy. Statistically, only 2% of employer policies pay out as employees expect them to. So, when I hear someone on the phone tell me their employer offers a policy, I cringe. How can I explain all this before they hang up? It’s hard to know where to begin. That’s one of the reasons I prefer to discuss this at someone’s home rather than over the phone. At your house, I can look through your employer’s policy with you. I can check every policy you have with you. Think of me as a doctor giving you a check up. You are not the professional. I am the professional. Google is great, but it doesn’t have a license. I am the one who studies this round the clock so I can protect you.

Typically, a person will choose to prepay a funeral home or crematory when they’ve discovered the hard way that final expenses can be a huge burden on a family mourning a loss. This motive is a really good one. You don’t want the same thing to happen to those who survive you as what happened to your family when someone you love passed away. But to be frank, it’s not as good of a solution as final expense insurance. And its not hard to understand why. So think about how all this works.

When you prepay for your funeral, your plot, your casket, the burial service, maybe a ceremony with a pastor followed by a luncheon, your cost will be something a little greater than the cost of a luxury car, even if you try to trim expenses through cremation, assuming cremation is allowed according to your faith tradition. And like the cost of cars, the cost of funerary services and items for sale keeps increasing year after year, often out-pacing inflation. So, when you pay for all of this ahead of time, you are thinking you are skirting inflation and solving the problem by removing a huge burden from your family. You are sending them one last message that says you thought about them. You told them you loved them one last time. It is such a beautiful gift. And it gives you peace knowing you’ve taken care of it.

Great. In a lump sum? Or are you still making payments?

The problem is that unless you pay for the whole thing in advance with cash, you will be making payments to the funeral home, and until you have paid them in full, the remainder of the cost will be imposed on those who survive you. Funeral plots have deeds and like any real estate, deeds are subjecty to liens. And the truth is, most funeral homes won’t do anything for your family at all, unless the bill is paid in full. There will be a lien on that property untill all bills are paid. So, you may just have created a problem rather than solved one.

Contrast this with final expense insurance. With final expense insurance, you get the full amount of a policy from day one. It doesn’t have to be paid in full. If you have an accident and die tomorrow, all of your final expenses will be covered. Whereas, when you prepay a funeral home, unless there is a clause in your contract stating otherwise, any credit you have paid in advance to the funeral home, they get to keep. Just like a bank, they can foreclose on your property when you don’t pay. So, if your family can’t pay the balance, that’s their problem. This is so tragic. I hate to have to explain this but this is what it looks like. Whereas you thought you picked out your final resting place, your body, or cremains, can easily wind up spread out over a lake or under a tree somewhere. Who knows, but it won’t be where you thought. And more importantly, the ones you love will be anything but relieved with that arrangement. I hate to be frank about these things but it is important. You do not want them to be upset with you after you are dead for mishandling what you’ve left them with.

Now all this begs a question: what if you’ve been paying a funeral home in advance, hoping to care for your family, but now you realize this whole arrangement may have been a huge mistake? I know I’ve painted a very bleak picture here, but there’s good news. Don’t worry about it. All you have to do to fix this is take out a final expense policy. Keep paying the funeral home. You’re on the right track. The policy will pay the remaining expenses owed to the funeral home in the event of your death, plus whatever more you decide to bless your family with. Problem solved. You’re going to need me for that, of course. So please don’t hang up on me or close your door telling me you’ve taken care of your final expenses, when all you’ve done is start prepaying a mortuary. Good for you. Now let’s really protect your family.

Seeing the basic problem I just addressed in Myth #7, the Funerary business came up with a sort of insurance policy that would pay out the full amount of the cost of Funeral expenses known as “PreNeed.” PreNeed policies are a step in the right direction, but they are far from ideal. Yes, they do pay out the full face amount of a policy so long as you pay your premiums. But that’s where the benefit ends. And they’re not what you might expect.

For one thing, suppose you have a PreNeed policy for $10,000 that you take out when you are sixty five years old and you pay a $100/month. That’s $1,200/year. So by the time your seventy three, you’ll have paid in the full amount of the policy. So, what will happen if you live to eighty? Well, you’ll have to keep paying $100/month to keep your policy or you will have nothing at all, even though you’ve paid in $10,000. By the time you’re eighty, you will have paid in about $19,000 for your $10,000 policy. Do you see what a bad net outcome that is? And that’s just one problem…

Is it irrevocable? Let’s look at the fine print and the laws in your state.

A possibly even greater problem is that PreNeeds policies from funeral homes don’t assign the family as the beneficiary – at all. The funeral home is the beneficiary. Think about that. So, what that means is that the funeral home is going to upcharge all it can, while it scrimps on as many of its costs as possible, so that it gets 100% of the face amount of the policy with a minimal expenditure and maximum net profit – even if that happens when you’ve paid more than the policy’s face amount, like I just showed you.

So, let’s be realistic here. Businesses are in businesses for profit – even businesses that serve families in their time of grief. By paying a business a set amount, the business is most likely to trim its costs and upsell more and more services as necessary, to retain all it can of the face value that the insurance offers. You’ve seen health care companies jack up prices to do this. The funerary business is no different. Once you contract with the company and have an insurance policy that will pay a set amount, free market competition is no longer a factor. A competitive market place is what serves the public, driving down prices. And once the funeral home is chosen as the beneficiary, the family can’t exactly take their business elsewhere.

Now to be sure, there are some laws regulating funerary contracts. Some are irrevocable and fall under planning laws, depending on your state, and those laws may require expense planning to avoid the exploitation of consumers this way. Revocable contracts, on the other hand, may allow you up to a 90% refund at any time during the contract. The upshot of all this is that it may be worthwhile to switch from a PreNeeds contract to a whole life policy for a number of reasons. Certainly, you should weigh it out. For one thing, whole life policies normally assign the family as the beneficiary, not the funeral home and give the family the liberty to spend proceeds as they see fit. This may involve the cost of airfare and other expenses such as time off work, that are often overlooked, and definitely not covered in PreNeeds contracts. Always keep in mind that any monies left over after final expenses are paid, are not subject to probate or taxation. They are gifts to those you love. That’s why life insurance policies are the ideal way to bequeeth savings.

As true as it may be that the older you are the more expensive final expense benefits become, I should let you know that there is at least one A-rated carrier that covers those up to age 89. You might also want to consider that when you are that old, you are likely to not pay premiums for as many years as someone who is much younger, so your total cost may not be that much higher than your younger peers would pay after all.

I also know which carriers offer the best coverage for those with serious health problems, including cancer, heart attacks, strokes, diabetes, kidney problems and so on – you name it. Typically, these will be graded policies, which means you won’t get the full face amount of the policy until the third year, but as graded and modified policies go, I know how to find you the best value. The first thing I should say about this is to look closely at the terms. Most graded policies offer something called a 10% return of premium. This means you are offered a benefit of 10% of the total premium you pay during the first two or three years on a policy. Compare that to a savings account. Where can you get 10% guaranteed interest on a savings account? Nowhere. And show me a savings account that suddenly pops up in value in the third year to tens of thousands of dollars. It’s a no brainer investment. I’m a specialist in finding you these.

Never say never! You can be on your death bed and I’ll find you a policy.

That’s good news, but it gets even better. Modified policies, with the right companies, pay even more even faster. As long as you pay your premiums, the value of your policy will jump up from year to year. So for instance, if you’ve got a $30,000 policy that pays 30% of the value after the first year, 70% after the second year and 100% of the value after the third year, your family would receive much more than their return of premium plus 10% back, as they might get with a graded policy. For example, if you passed away in month 15 and the policy paid out 30%, that would be $9,000 to your family. If your premium had been $100, you would have only paid in $1,500 at that point. That’s much more than 10%. It’s 600%.

I’m not going to say that I can qualify every single person for all the insurance they want. But I am going to say that in over 99% of cases, it is going to be a myth to say you don’t qualify at all, and I can get more people qualified than most other agents can due to the large number of carriers I can call on. Therefore, you probably will qualify – maybe not for a million dollar policy, but for enough to help your family out when you pass, having done what you could. If your family wants more than the best you can do, then please give the money to me instead. They are ungrateful and I wouldn’t be. I can think of all sorts of charities I would rather give that money to.

Okay. I’m kidding. Give the money to your family. But do be realistic. I’m here to help you. I don’t want to waste my time. And I don’t want to waste your time. I’m happy to help you do what I can.

This is probably my favorite complaint. When people say they don’t have the money for life insurance, it tells me they are responsible people who have priorities. They may value a policy, but they are figthing the good fight of daily life, quite possibly living from paycheck to paycheck, as they start to see inflation get the better of them and defeat them in the rat race. As they seek to trim expenses wherever they can, to stay within their monthly budget, especially husbands and wives, they see a final expense policy as something they might be able to put off until some later date when they can finally get a break in life … some good news, maybe a new job, maybe some windfall like winning the lottery or being the beneficiary in some lawsuit.

I do deeply appreciate that thought because I’ve experienced that thinking myself. But it overlooks the fact that the cost of insurance is never lower than what it is today. Year by year two things happen. #1 – Our age increases, bringing us closer to our last day on Earth. And #2 – we start losing our great health. Both of these factors chip in to increase the cost of life insurance at a later age. And for couples, the chances of bad news are doubled. Typically an income will disappear. Who will pay the bills when they are gone? How long will it take to make an adjustment to living arrangements? Will a bank foreclose on your house so the surviving spouse loses their hard earned equity?

This is worth an extra paragraph or two to really think about.

Think ahead and keep in mind that younger people qualify for better policies that older people can’t get – and they’re cheaper. Many of these policies offer cash back options too. Whole life insurance, in particular, is easy to borrow on. Its cash value can be used to collateralize loans, maybe buy a house so you don’t have to pay rent any more. Other policies serve to force savings you wouldn’t have the discipline to lay aside otherwise. And if a person is older, there are many policies that offer living benefits. This means that if the policy amount is needed early for things like chronic or fatal illnesses or assisted living, the policy will cover those expenses. It saves your family from paying for your medical expenses when you get old. And that’s as much of a final “I love you” as paying for a funeral expense. It may be something you all want.

We all do what we can. But if you really want to have value, where you don’t have to compromise in the end, start early. When you are young, you may think that you can’t afford it. Just be aware that I can show you policies that allow you to build up incredible cash value. Ask me about IULs. Not only do they build up cash value, but they are indexed to stock values in such a way that if indexes like Standard and Poors go up, they go up with it, but if the S&P goes down, they hold at 0%. Amazing, and you can borrow from them at very low interest rates. You might just discover that the whole policy has a net zero cost.

Finally, you should consider accidental death benefits. The number one cause of death among young people is accidents. The younger you are the truer this is. Among teens – accidents account for almost half of all deaths. The nice thing about accident insurance is that only dare devils and people who die committing federal crimes don’t qualify for it, and it’s the cheapest insurance there is. Even if a younger person just puts in a few dollars a month into a policy, they can make a huge difference to their families when they die. Minors are typically covered with a few extra dollars added to an adult’s policy too. Always ask about children and grandchildren riders on your policy. Some of those riders offer options to continue insurance as separate policies when the child gets older. And that gives them even more value.

A lot of people think they have insurance they don’t really have. It’s very common and here are the main reasons why. To start with, ten thousand Americans turn sixty-five years old every day, which means suddenly they can officially collect social security. They are on a fixed income for the first time in their life. The banks know it. Direct mailers know it. And they know that everyone needs to make a plan for their final days so these people are top targets. What senior citizen hasn’t filled out a few forms in response to this? Mailer after mailer will offer policies for pennies. A lot of citizens get tired of thinking it’s too good to be true. Even your local bank, in whom you trust, has offered you some free starter insurance, hoping you’ll buy more. How can you resist?

Really? What kind? How much? Who with? What are you paying? What’s the catch?

Insurance consultants, like me, know something about all this. We’d be willing to bet that that convenient form that got filled out leads to one of three things – a graded policy, a renewable term policy, or to an accidental death policy. The first type doesn’t pay the full benefit the first few years. The second keeps increasing the price and ends at a certain age. And the third is really accident insurance. It won’t cover any death by natural causes. Even if a well known and trusted bank name is under it, senior citizens need to understand what they’re paying for.

And I have a question. Are banks really in the insurance business now? Rest assured, your bank is not in the insurance business and neither is your credit union.

But maybe I’m wrong. It could be a valuable policy – or at least seem that way. Beware because there’s a very good chance it has an introductory price that is scheduled to increase after five years. It’s actually renewable term insurance rather than whole life. At an older age, this matters a lot. A five year term at age 65 is pretty cheap. Most people live past seventy. From 70-75, a lot more people die. So what happens to the premium cost? It goes up. And then what about the five years after that? You may have a renewable term policy that says it’s good to the age of a hundred. Don’t let the high age on that contract fool you. That insurance company is hoping you won’t notice the fact tht the premiums are not level. They are going to increase. Have they made it clear to you how much the premiums would be once your reached the age of 80? How about 85?

Do you see what I’m up against? You might just have several of these types of policies before you meet me. And you’ll likely ask yourself, what do you need me for? You’re thinking to yourself, you can just keep adding more and more policies you’re getting in the mail. They’re cheap. You’re insured to the age of a hundred, for some huge amount, and you’re pretty sure that you can afford it. But really you can’t. And you won’t know that because you won’t let me in your door.

So, what I have to do, if you let me in, is get you to call all of your insurance providers and get them to tell you directly what’s going to happen when your term renews, when it will renew, how often, and what the price will be when that happens. I’ll also want to know what sort of graded policy you were issued, because you may just have no insurance at all. This may require you to look for your policy, but I will help you. If you’ve lost your policy, you can get a new one. And if you can’t remember who your insurance providers are… (Good grief, I can’t remember why I was looking for my keys in the refrigerator a minute ago)…. If you can’t remember who your insurance providers are, then all you have to do is check your bank statements.

Thank God for bank statements. Every month, you pay your insurance bill and every month, your bank statement will show you both how much you paid and who you paid it to. If you want me to help you go through that I can. I’ll put us on speaker phone talking to your insurance carrier myself, both of us together. I’ll make sure they send copies of your policy both to you and to your beneficiary, so they’ll know that you have it. You do realize that your loved ones and the charities you want to bless when you die won’t receive a penny unless they know you have a policy. Right? So I’ll make sure you have all the copies of your policy you need.

But do you know what I won’t do? I won’t ask you to cancel any of your policies unless they are completely worthless. We’ll figure that out together. And then I’ll see what kind of an actual whole life policy you would qualify for – one that won’t have increasing premium costs; one that will last until the day you die; one you can afford when it’s most likely to be essential that you can.

Friend, in your final years, you are on a fixed income. You can’t risk making bad decisions. It’s my job to protect you. It may take some work to give you a good insurance check up. Be ready for that when I come to your home, both you and your spouse if you’re married. It’s some work, but that’s what I do. And it’s worth it. I’m a licensed professional. I don’t work for any insurance carrier. My business model is built around helping you avoid the misakes that thousands of others do so that you can get the best coverage and protect those you love for a price you can afford. That’s my job. I rarely give a thought to what I get paid for it. All I care about is you. I just need you to let me help you. A consultant and a salesman may both be paid commissions but they are two very different things.

If you don’t like whole life, I can consult with you on term life instead. As I said in a previous video, the carriers I work with have dozens of products each. Many of them are the best term products in the industry. Everybody shops price, price price, but my job is to educate, educate educate.

Of course, I know you can get a much larger policy for a far lower premium! Particularly when you are younger, term policies make really good sense. All I ask is that you think about what you’re betting on. You see that a term policy would certainly help those yoou love if you did happen to die within the term. But if you outlive your term by even one day, and you don’t pay extra for a cash back or return of premium option, then you’ll lose every penny you paid in. So what seems like more policy per dollar can easily become valueless the day the term expires. See how that works? It’s a tradeoff. It’s a gamble.

“Coverage” means covering every possibility.

But did you know that you can have it both ways? If you want the high value of a term policy with a low premium that converts to a whole life policy at the end of the term – irrespective of your health at the end of the term, I know of a carrier that will convert your policy. You can also stack policies – one can be whole life while another is term and you can pick and choose products from multiple carriers to optimize your protection. If you can afford it, I recommend you start stacking insurance policies of different types early because your health and age are going to keep driving up the cost of any whole life policy you eventually buy. Conversely, if you don’t buy young, you risk being forced to apply for a policy when your health is declining. That will drive the price up much higher than it is right now.

In the long run, I’d generally recommend having a good whole life policy as a base. That should be your core long term policy. Let it build up value as you age. Consider it a savings plan you can borrow from for the rest of your loife. You can’t borrow on a term policy. Unless you have a rider for return of premium or a cash back option, a term policy has no cash value. Add a term policy to your whole life policy.

Following my advice is particularly important for young couples. Not too many people live forever, and bad things happen to good people way too frequently. When you and your spouse take out policies for one another, if the worst imaginable news comes to your home, at least you won’t have to feel the full brunt of the financial impact of losing part of a two person income while you’re grieving. You may be able to prevent a foreclosure on your house. You may save its equity from going to a lender with a lien. You may buy yourself enough time with your benefits to make new living arrangements.

Whole life may cost more than term, but if it acts as a savings account and also protects you against life’s worst nightmares, it isn’t all about face and premium amounts. It’s about dealing with life itself. If it pays for itself, as many do, then your net cost is zero. Which is more expensive then? Let me help you with both term and whole life policies. I’m here to help you think it through. I would never steer you wrong.

Now it’s time for our appointment. Tap on a date below …

Here’s what’s next…

Now that you know I’m here to help, it’s time I came over. Click on a date below, choose a time, answer the questions on the form and submit. That’s it. I look forward to meeting you!

With 2024 around the corner, Elmer Truesdell Merrill’s work, Essays in Early Christian History is becoming Public Domain in the coming year. Unfortunately, it is long out of print in the USA. If you want the whole book, (and why shouldn’t you?), you will have to order it from London. I highly recommend it. Here is chapter 11 – “St. Peter and the Church in Rome”. I think it is fair use to share it so that my supporters have a chance to offer me some personal guidance as I prepare my own work …