A Health Matching Account (HMA) is not to be confused with a Health Savings Account (HSA). An HSA will have value only while insured if a person qualifies and utilizes its benefits during that time. An HMA retains its value after you quit a job and when you change insurance plans. Its value lasts. Even going on Medicare doesn’t disqualify eligibility.

Neither does poor health. It is a genuine savings plan.

I’m happy to share my personal experience with my HMA account. It’s very user friendly.

It’s my mission to save clients money while optimizing the perfect combination of insurance programs they qualify for – so they can keep it. There is nothing that can crack a nest egg faster than unplanned for health issues and accidents. Cancer, heart attack, stroke, highway accidents and fatalities – these things rock families to the core. And what about if we live long but don’t prosper? Long term care plans may be required. But do they even exist? What is your plan?

Life is a gamble. Insurance turns it into a sure bet. But is it adequate?

The problem is that the house always wins. The odds are always slightly stacked in favor of the Insurance Company rather than the consumer. That is their business model. That is how they stay in profit. They collect more in premiums than they pay out.

Young James Carvin and friends – for the young, gambling is a game. With age, not so much.

Insurance companies are in the business of gambling according to the odds. The odds are you won’t need your insurance right away. So what is its value to you, the consumer?

What insurance pays for is peace of mind, knowing that if we get unlucky, we’re still covered. As an independent insurance agent, that is what I sell – peace of mind. Thanks to insurance, the bad case and worst case scenarios in life become less bad and less worse. There’s peace in that. And the peace I sell costs less and buys more because I do the shopping for my clients so they can also know they aren’t paying more for less.

I sell both life insurance and every form of health insurance. But on the health insurance side, there is a problem. The cost of health care keeps going up and so do the premiums. People can’t afford adequate policies any more.

I hate that only the wealthy can afford peace. My sister suffered such a long and painful death – on a feeding tube, in dementia, not understanding why she was paralyzed, why Jesus wasn’t answering her prayers, unable to communicate that she might want a DNR.

It was horrible.

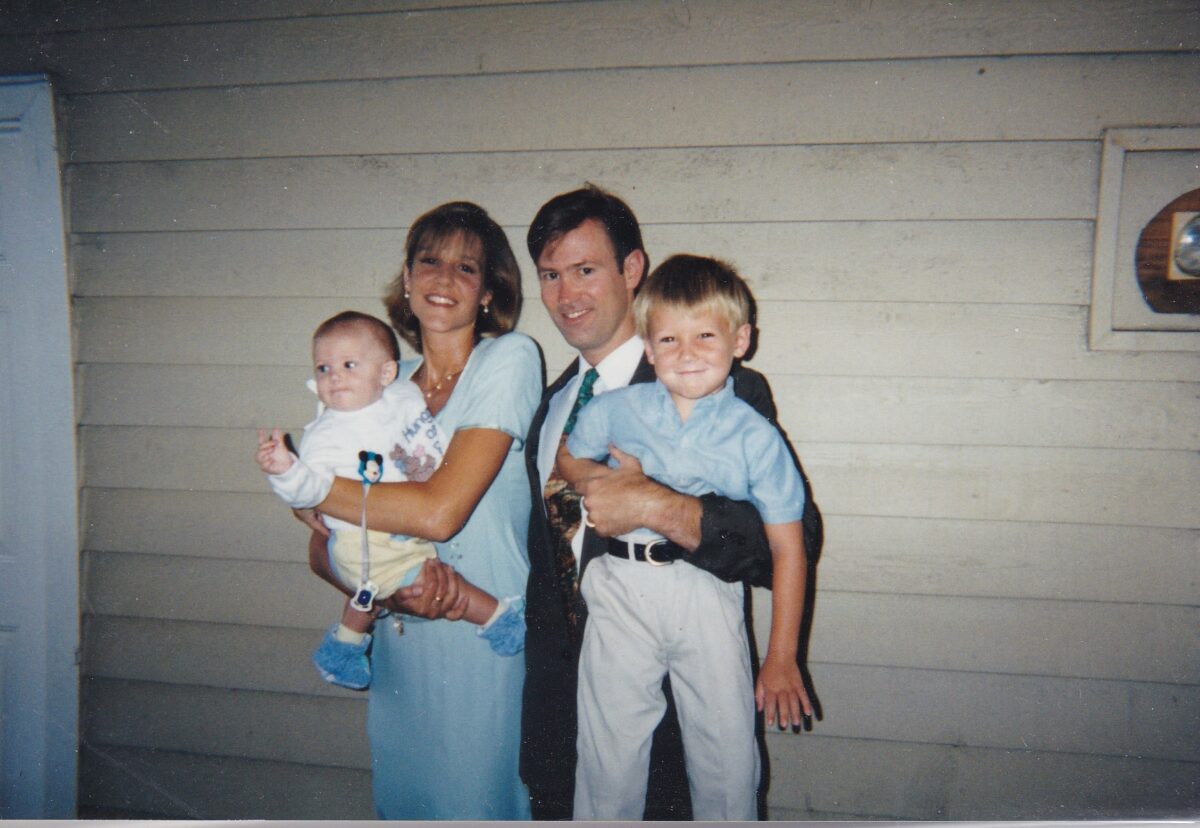

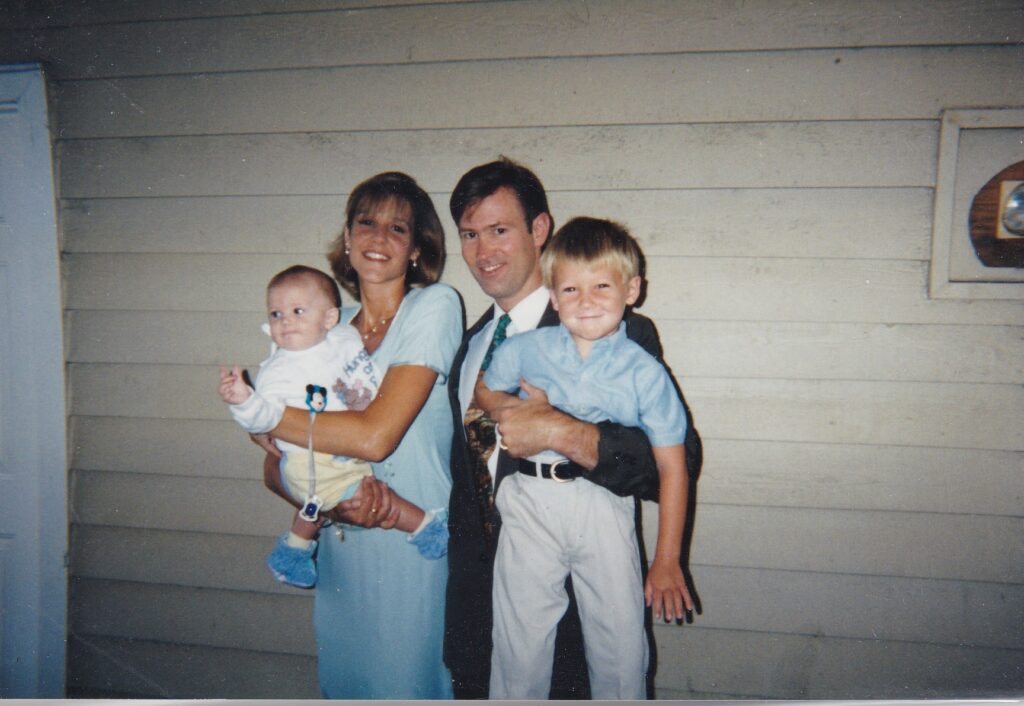

Her husband had abandoned her and only her four surviving brothers, who all lived in different cities, were left to make sure she was cared for. I moved with my wife to Tallahassee to stay close to her and make sure she wasn’t being left alone in her nursing home without proper attention. I never announced when I was visiting. And it was never enough.

My family and sister getting fresh air. We made the best of things and did the best we could.

Sometimes she would be asleep. I would visit the other residents. There were rarely any other visitors. I didn’t go into the rooms except my sister’s, though I would sure liked to have kept the staff accountable. Those in the common areas – the patio, the tv room, the dining halls -these managed to sit in wheel chairs. Some could turn the wheels by themselves. Others had to be pushed. They all had stories to tell. I fell in love a hundred times.

Do you have family that would visit you if you were forced to live in a nursing home and were in very deep need? How often would they come? How many hours would they stay? If you had the very best nursing home care, how much of an improvement would that be over the worst nursing home care where you live? Have you visited your local nursing homes to consider what the answers to this question might be? Consider this a mandatory assignment. Consider it a personal responsibility. And most importantly …

Do you realize that more people will wind up dying after long stays in nursing homes than not?

Some die by accident. My mother was very lucky. She didn’t pay for assisted living. She lived by herself for sixteen years after my father died. Then one day, unexpectedly, when she was ninety years old, she died of a heart attack. She was very lucky. We all were. We couldn’t afford a nursing home. And she was on Medicare. She didn’t have adequate nursing home coverage. She didn’t have any sort of a long term care plan at all. We all gambled with her health. And we got lucky that she won that gamble. The Lord took her very suddenly.

My sister was not so lucky. I watched her suffer daily. I prayed with her. Corinne only received as much care as Medicaid would pay for. The rest would have to come from the charity of her family. The words “adequate care” stretched the word “adequate” to new lows. I saw her daily, seemingly endless torment, and I wondered whether my own life would end with a story like hers. Maybe I would get lucky and die more suddenly, like my Mom.

The residents at the nursing home didn’t mind when I dressed up on Independence Day.

Given this deep reality in my life, I’m surprised more people don’t ask me about long term care. A friend I have, who was about to turn sixty, and who has a history of health problems, did ask me about long term care plans. He was already on disability and eligible for Medicare, perplexed that long term care was inadequately covered by the government.

Well they do. The plan is Medicaid. First the patient and their family burn through whatever savings they’ve struggled to amass all their lives. Then after that, they qualify for Medicaid. Then when they die, unless they have a life insurance policy, the family gets no inheritance and has to pay for their funeral expenses. I’ve seen this more times than I can count.

It’s tragic. My poor friend had worked so hard all his life to put his children through school and to pay for his divorce. His children had moved away. Now here he was all alone, realizing that his life was likely to be like that of my sister. He was trying to form a plan. And someone told him that at the age of sixty long term care (LTC) plans get significantly more expensive and offer fewer benefits.

The reality of a person’s retirement picture hits hard at the age of sixty. But the time to start working on it begins decades before that.

He was right about the sudden leap in premium costs at age sixty though. So he turned to me – the miracle worker. If anybody can solve an insurance problem, it’s me. Unfortunately, I had to let him know that no sound insurance company would qualify him. He was stuck with no long term care plan. I told him that when open enrollment season came up for Medicare that I would review plans with him and let him know what the best option was. We’d have to set an appointment 48 hours in advance for that.

But I gave him one other piece of advice – one that it wasn’t too late for him to do. Enroll in an HMA.

Everyone should have an HMA. To put it simply, an HMA aims at cutting out-of-pocket expenses in half. It’s important to note that it is not an insurance plan at all. It’s a savings plan. That’s why they don’t use the word “premiums.” You pay maintenance fees and make contributions to your savings plan. Your contributions are then matched by the plan, which builds up the benefits value you have available. It’s better than insurance really. With insurance you start over every year. With an HMA you accumulate value that carries over year to year.

These videos explain how HMA plans work

Did you watch some videos?

So let’s say my friend goes into a nursing home long term when he turns seventy and has sixty thousand dollars accumulated in his HMA plan by then. At that point, let’s say he has a choice between two nursing homes – Abundant Staff Pamper Place or Minimal Medicaid Manor.

He may just be able to afford Abundant Staff Pamper Place if he has that HMA. He may not be able to do that if he depends on his own savings or on Medicare. An HMA may not solve all of his problems, but it might just cut them in half.

Perhaps mosty importantly, he may not ever need long term care at all. How does he know he’s going to spend years of his life in a nursiong home? He doesn’t know that. He may need to use his benefits somewhere else. What if he just needs to cover his pain medication as his arthritis gets worse until one day God is merciful to him and he dies of a heart attack? If that is the case, his main concern will be paying for his medication. If it isn’t covered under his Medicare plan, he can pay for the rest using his HMA.

The difference between an HMA and insurance is like the difference between cash and barter. An HMA is simply more efficient and useful – like cash.

The Pamalogist

Think about it. Unless my friend exceeds his HMA plan limit, his only out-of-pocket cost is his monthly HMA plan contribution. His HMA may just cover all of his annual deductibles and copays, plus the cost of any uncovered meds. That’s equivalent to 100% coverage. We don’t know what will happen in life. But an HMA covers more possibilities because it isn’t limited to a specific type of medical need.

An HMA is the only kind of plan I can think of where the consumer wins every time. Every other kind of plan is gambling against the house while the odds are stacked in the favor of the casino.

HMAs are for individuals, for families and for employers looking for better benefits for their employees. You won’t be disqualified for pre-existing conditions. There is no health check.

Watch the video I’ve posted here for more details on how HMAs work. Decide on your budget. Let your contribution to your HMA plan become part of your monthly budget. Even though it is not technically an insurance plan, you do need to pay monthly. If you don’t make your monthly contributions on time, you will lose your benefits. Nothing else can cause you to lose your benefits but it is imperative that you not commit to more than you can comfortably afford.

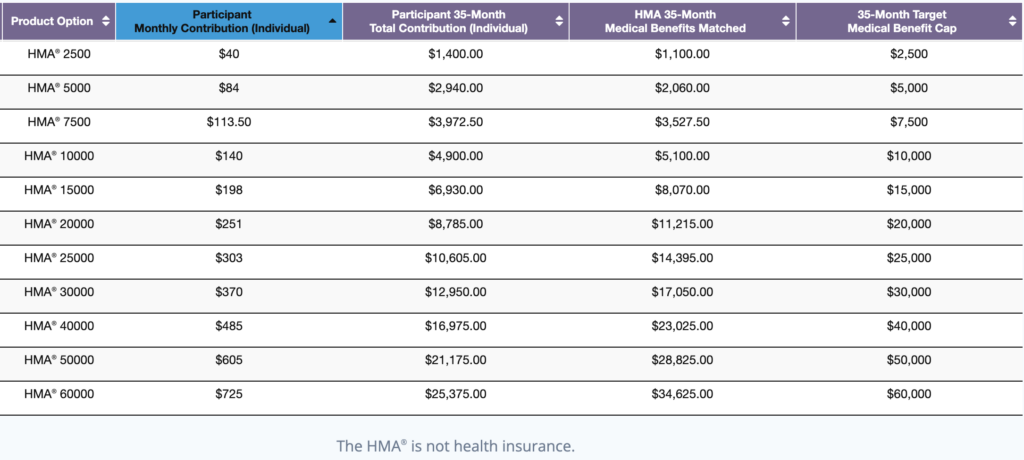

There are eleven plans – something for every budget. They start as low as $40/month to $725/month for individuals. Spouses and children can also be covered. Never spend more than you can afford. Here is the breakdown …

It’s been a while since I blogged. I recently entered a season of change. Turning 65 gave me much to think about. What was I going to do with the rest of my life? I got heavily involved in projects I’d been wanting to do since my twenties.

OK. I didn’t just write some music. I invented an entirely new musical system.

You’re supposed to be able to do stuff like that at my age. And tomorrow, I have yet another birthday. What is happening with the time? Didn’t I just have one of those?

You can probably tell from my last post that I was getting frustrated too. The last life insurance policy I was working on with a family, the husband and I had talked for months about what his best path would be. I designed the best conceivable plan and he told me he was ready to buy a policy. But he lives in California and I live in Florida. And he and his wife didn’t realize that. They wanted to be able to step into my office. His wife absolutely refused to give her personal banking info to me over the phone.

I’m setting 72 Psalms to Ragadana Modes

Bottom line, I put about twenty hours of research and prep time into writing a policy that, in the end, fell flat when the wife put an end to it. Unfortunately, she had been ripped off from someone on the Internet in the past.

Upsets like that are a normal part of this business. I was paying $50-70 per contact so that they would call me. I refused to do what so many other life insurance sales people do. They buy two and three year old leads for 50 cents a piece.

They call each lead 9x per day using an autodialer, or hire someone to call for $10/hour. They don’t feel like spammers because they receive live dials. Their hourly worker will transfer the call when that 100th call answers and is ready to talk. They don’t care how many people tell them please stop calling. They get paid by the hour. They set return call appointments.

That’s how 99% of agents do it. And the ones who just keep forging ahead, are the ones earning six figure incomes.

Doing business that way reminds me of eating hamburgers and chicken. You don’t see the slaughter. You just see the sandwich.

They get really good at closing too. They don’t really care if a product is in their prospect’s best interest. Their only ethic is their personal gain. Where’s the beef?

Mode 42 has six half steps, a Minor 3rd and a Major 3rd!

The beef is their commission check. You should be aware of how commissions work in this business. The client doesn’t pay the agent. The insurance company does. Life insurance generally pays a percentage from 80-140% of the first year’s premiums to the agent. Large policies can have a sweet pay off. Health Insurance tends to pay a fixed initial amount and then pays monthly or annual residuals to the agent for the life of the policy. I like health insurance. Everyone knows they have to have it. Life insurance – you’ve got to see the value.

That’s how this business works. When I don’t work I don’t get paid. My residuals start to drop. So taking some time off is costly. Then again, a good week isn’t necessarily measured in income. A better week might be finally doing something you’ve wanted to do your whole life.

Weeks like that are better weeks indeed.

I can’t tell you how nice it feels to finally have that one project complete. I’ve been walking around with a degree in music composition for the past forty five years and not using it. That’s changed now. As my wife will attest, the hard part is getting me to stop. And there is still quite a bit more to do …

Show Me the Money

Poor woman. She wants to make sure I’m paying the bills. Yes, dear.

She does have a beautiful heart. But I’ve spent all of my healthiest years paying the bills. And no, I don’t see how writing music will make me any money. She’s got me on that one, .

Balance.

I get it. But I know I’ve got health insurance season coming up in October. Are you ready? We’ve got a pretty good client base right now, and quite a bit of work left to do following up on all those who’ve called asking about life insurance this past year.

I realize I’m more of a “you-call-me” kind of guy. Way too passive for my wife’s taste. I may well be doing my contacts a huge favor by urging them to immediately take action. I sometimes have to get over the fact that I believe people don’t want to be pushed into life’s decisions. There’s a place for common courtesy. But I give good insurance advice for a living. And when you don’t buy, that can cost you thousands of dollars and be tremendously hard on your family.

If only I hadn’t ever experienced the pain and reality of it. I’ve had more than one client pass within a year of writing a policy. One passed literally two days after I wrote a policy.

Did you know that I have to pay back my advanced commissions when that happens? I do. In fact, I still pay one company monthly because of a huge advanced commission they paid out. If the man had only held on six more months. I’d have been in the clear. His family would have enjoyed being with him as he aged. But my business is one that protects people against bad news. And ironically, when it does all it is supposed to do in that worst case scenario, which is my strongest selling point, I have to pay back the commissions I’ve received.

It’s a consolation at a hard time for the family but it’s a double ouch for me.

It makes me consider pitches like, “what will happen if you walk out the door and get hit by a car tomorrow? How would your family adjust financially?” This is a very common sales pitch in the insurance industry. I don’t avoid it. It’s a harsh reality that bad unexpected things can happen. And then there’s every insurance salesman’s pet peeve – the time to ask me for a life insurance policy isn’t after you find out you have cancer. It’s before you get that sort of bad news. Is there a tactful way to say this?

I’m starting a crowd source capaign among musicians to complete the project

Imagine saying that for a living. I’ve learned to get comfortable with it but for the most part, I still rely on people to think that through themselves. I figure that’s why they are calling me. I don’t like to insult people’s intelligence by stating the obvious. Instead, I’ll ask open ended questions like, “why do you want to buy insurance?

Ultimately, most of the companies offer similar levels of service so it all comes down to price. How fast does your cash value build up? And what is the cost of your premiums? I research what the best product is based on a person’s health, age, gender, location and budget. People can’t do that by randomly searching on the Internet. I look through a database of about 64 companies and hundreds of types of policies. Then I write up policies based on that research. That’s what I do.

I’m not that guy who sells ice pops to Eskimos. But take it from someone who put off working on his materpiece for forty years … there’s a time and a season for everything. I needed a few months away from the daily grind of the insurance business. But Honey, our insurance business is about to hit some all time highs. Hang in there. Thanks for letting me have a little play time. I feel refreshed.

I had a bad week. For me a bad week is measured in two ways. (1)How many families did I help? (2) Was I able to help my own family?

Now if you are savvy, you may have guessed that there is a strong correlation between how many families I can help and how much I’m helping my own family but you may be unaware of the underworkings of how I get paid and how much or how little getting paid may have to do with helping my family. To answer this latter question, I’ll need to focus a bit on what I value. Not all insurance agents have the same values. Some lack a good life-work balance. Some lack lasting marriages. And not all cherish or evaluate honesty and integrity the same way.

James Carvin is perplexed

Here’s my story. I have a sort of Kantian belief that if everyone lied, the world would fall apart, whereas if everyone treated everyone else with kindness and honesty, not always serving themselves, that the world would be a much nicer place for everyone. Call me naive. Call me a dreamer. I don’t think about commissions much. I contract with as many carriers as I need to to provide the best value for as many families as possible. And I assume the money will follow. Eventually. Never lose faith in that.

But Is Aiming Wide and Long-Term a Shot in the Foot?

If you understand the insurance industry, you may understand how this sort of Kantian philosophy can be self-detrimental. Although it may be empowering, there are several ways in which contracting with too many carriers can be harmful to an agent. Firstly, every hour spent training is an hour taken away from selling. Contracting with many carriers and many types of products in many states is a long-term strategy. And it has a moving target, since carriers change their competitive edge with some frequency.

It’s also detrimental to a more efficient sales process. If efficiency was my top priority, I would stick with one area of expertise. I would either sell medicare or ACA, or hospital indemnity, or dental plans, or cancer, or accidental, or final expense, or IULs, or annuities, or health matching accounts, or group insurance – not all. (I do have multiple sources for all of those things in multiple states and much more).

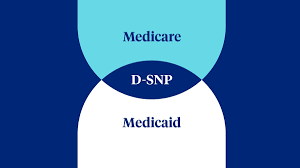

If I was like most, I would have a store, not a mall, or a section of a store with just one demographic to target. I’d probably focus on life insurance, since that’s where the big up-front commissions are. And I sure wouldn’t become an expert in DSNPs.

I’ve spent days trying to help people get onto Medicaid, knowing they qualify, or on Medicare since they are on Medicaid but didn’t know Medicare came withb the disabity SSDI they were receiving. I’ve spent a lot of time teaching people how to access their social security accounts to access their Medicare numbers – only to find that they aren’t able to or won’t take the initiative to help themselves. A DSNP is a Dual Special Needs Plan. Use my abreviation chart if you see any acronyms you’re unfamiliar with. My plan is to be the ultimate source for training in all things insurance. Knowledge is power, but in the short term, it may not be practical to spend time gaining it.

Still, knowledge helps me to know how to fix things. I have a deep inner need to fix problems and the harder they are to fix the more determined I get to solve them. My friends, this sort of need is not compatible with efficiency and high volume sales. If I tell you that I’ve had a bad week, it probably means that I put in a great deal of effort to help people in desperate need of my help, but not only failed to meet that goal, but also took time away from my own family, not to mention the bills that I accrued both in my business and at home.

Have you ever wondered what it is like to be an insurance agent? Despite the presently very gloomy week I’ve been telling you about, it is actually a very lucrative career on average, especially if you do it the way the most successful agents do. And you don’t even need a college degree to get started. I could train you myself and show you the steps I took to get my own licenses. I’ve been turning myself into a human insurance encyclopedia. I could even offer practical advice about who to work with based on your personality type. I would be the first to tell you why my own personality type isn’t the best fit for certain types of insurance sales – at least not in the short term. I’ll explain.

A Tale of Two Personality Types

I love missions. I hate sales. Are you my type? I believe that if you do the right thing, the money will follow. I believe that if I do extra research for my clients so that I know with certainty they couldn’t possibly get more insurance for their dollar, that I’ll get as many referrals as I can handle, and that one day my referral business will be sufficient to end my need to ever pay for leads again. Does that resonate with you? Well, then you have what I call agent personality type one.

Then there is personality type two:

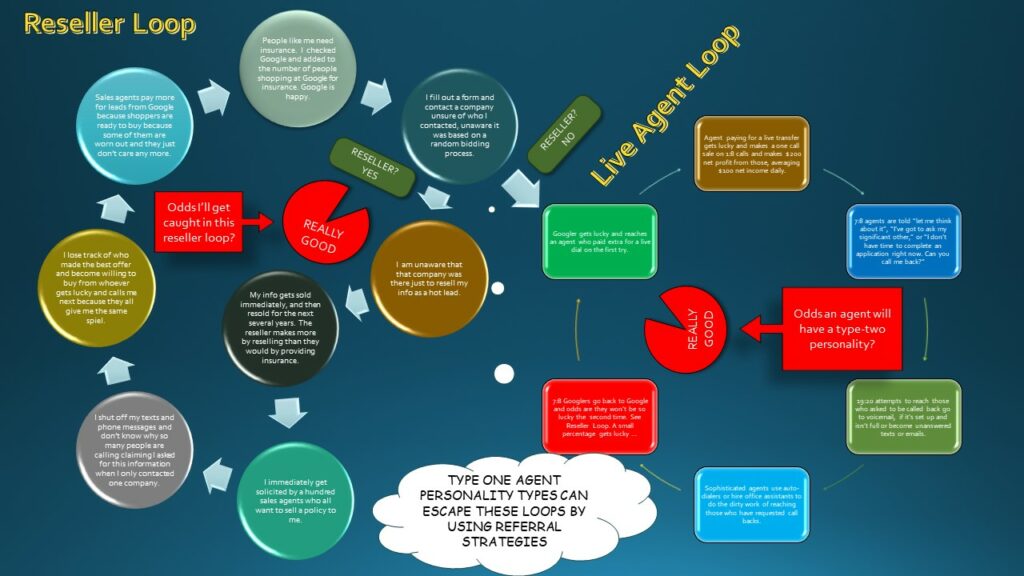

When you start in business, any business, not just the insurance business, if you’re not lucky enough to be a social media influencer, or if you don’t come loaded with startup cash to pay for a staff and an advertising agency, or pay for AI to do most of your work for you, or to organize a customer relations management system like SalesForce, then you are likely to do it the way I was told I should do it by the people who introduced me to this business. They are looking for people with personality type two. Only people with personality type two make a quick fortune in this business. The rest choose to leave the rat race. As a result, the majority of insurance agents do it their way. They are the only ones that last.

What is their way? I hate their way and it’s not how I want to spend my life. They pay a leads agency for leads. The cheapest leads go for about 50 cents. They are three years old or older. These leads have been sold and resold by Facebook, by Google, and by specialty agencies who bid for key words and take the same information and sell it over and over and over again.

There is nothing exclusive about these leads. They were generated by people like you and me who occasionally fill out a form we find online, usually on a trusted source, innocently enough – some ad we saw as we were scrolling through our favorite social media site, or from some active search we did. We probably cringed as we discovered we were being asked for our contact data in exchange for a quote or some hyped up piece of information that was probably too good to be true.

It really hurts, from my perspective, to find out that a $50 lead was actually from someone responding to an ad about free government money. Do I have to pay more than $50 to pay for someone who actually wants insurance?

Such people would have been smart to recognize it was too good to be true, and since the call went through, I can’t get a refund for the lead. And now it is too late. Too late for them and too late for me.

We’ve all done it. Our inbox, our text messenger, our phone, will receive dozens of messages daily for the forseeable future. We’ve learned to block it all, but it’s still a major nuisance in our life. Meanwhile, my business, on the receiving end, is ruined by it.

Sometimes, we actually want what someone is selling. Type two personalities count on that happening often enough. Some people are impulse shoppers. They count on that too.

Others of us are more methodical and like to compare and get the best value.

But all of us get worn out sooner or later. We don’t have the unlimited time or energy we need to do a thorough search. And once we see how the system works, we become fearful that the more places we check the more people we’ll have calling us. We hate callers, so we cut the shopping journey short even if we know we’re probably paying too much. This is what the type two agent personality depends on. They are comfortable calling people all day long if they can wear out enough people. They don’t feel bad about taking away a little from their quality of life by being the hundredth caller.

And from that weary prospect’s perspective, maybe just buying something and getting it all over with, will stop the endless stream of solicitations. But will actually buying the thing dozens of agents have been calling to sell us get the phone to stop ringing and the texts to stop pouring in? Not at all. So the type two agent’s call will be like a drop in the bucket. No harm, no foul.

Pullerama

I have a deep seated disdain for the fact that the reselling of leads is an American reality.

On the high end of the leads pricing scale is something called an exclusive lead, and at the tippy top, is the exclusive live-transfer lead. I pay $61 a piece for those. I get very specific information to show they were qualified and it is all ported over to me at the time of the call. To me, those are the only ethical leads to buy. The person has contacted me specifically as they’ve searched, even if they reached me indirectly through the leads agency. As a result, I don’t have to lie when I tell them that they asked for the information I am trying bring them. I pay that much just to be ethical. I could have bought 124 unethical leads for the same price and used the script my trainers gave me. To do that, I would have to push sell, rather than pull sell, not just lie. Sure they asked for that info at some point, some of them have anyway. But either way they didn’t ask me for it. They didn’t even ask a company I work for for it.

I used to own the domain name “pullerama.com” because I hated spam and pushy ads that intruded on my life and workspace. I started building a search engine in 1998 but I was unable to compete with the speed, efficiency and capacity of Google and didn’t get that business funded. It was designed to solve the problem Google has created by reselling personal data.

The type two salesman doesn’t care about any of that. Many of them will lie to make a sale. Others will find ways to rewrite their pitch so that what they say is all true. But they have this in common. They see success in numbers. And success is all they care about. They are told to call each lead nine times daily. Yes, that’s right. Nine times. Three times in the morning, three in the afternoon and three in the evening. There is rarely an answer on the first call, but by calling three times, the solicitation survivor may just figure it’s urgent and not be another salesman.

Never leave a voicemail until the third call, I was told. That’s how all the successful agents do it. Push! And never give up on that process, we are told. Do it for thirty work days in a row. Buy new leads every Sunday and Wednesday night. Work them from 8am to 9pm daily. Get licensed on the opposite coast from what you live on so you can have more calling hours. Date your leads. Slow down calls on the “older” leads to once every week after they’re a month old. And then after three months, you dial them once per month. That’s what I was advised to do.

Successful insurance agents on their teams follow this process religiously. Then one day they figure out how to use auto dialers and hire cheap labor from foreign countries to transfer their calls to them. A few of them hire marketing agencies to build them landing pages and ad campaigns to skirt this cycle, but most do it low tech. They just keep buying those old cheap leads. And when they hire somebody to make their calls for them, they leverage their time. Ahhh. Peace at last. No more people cussing at them and dodging them all day long.

It’s a better use of their personal time, but a type one personality will still see this as woefully unethical. It reminds me of the meat industry. Consumers don’t sense the killing because that part all takes place at the butcher shop. They pay for it and the problem remains. They just don’t have to personally experience it.

It takes most of the push away from their lives too. It even becomes enjoyable. Once they have you on the phone, they reel you in like a fish on the line. Pulling you in feels like pull. You improve your sales skills. Closing the deal feels like something they asked you for because it isn’t the hundredth dial you’ve made that day and all you need to do is get better at anticipating your objections. First they hook you on the line with a good listening strategy that involves repeating what you just got them to say, or verify from the data you purchased.

A good type two personality will master this and be convinced – “Whatever you just admitted to me you needed, you just asked for and you agreed I could solve your problem. You sold me. I didn’t sell you.”

An ideal type two personality may even be honest about all this and admit, “this may not be the best solution, but you didn’t call me because I had the best solution. You called me because you said you needed this.”

And they are closers. You just told me you needed this, right? You showed me you could afford it. Right? So what is stopping you from doing this right now? Why do you need to talk to your brother about it? What if you die today? Didn’t you just say you needed it? Why are you thinking about it? What are you not telling me? What are you afraid of? Let’s get this done right away. What is your social security number and bank-routing number?”

That last part was a joke. Insurance agents do need to access this personal information. We have to earn trust somewhere in this conversation. Trust is one disadvantage a person making hundreds of outbound calls daily has. But a true type two agent will recognize that this is just part of the numbers game they play. Some will balk at giving out personal info to someone who has just called them. They learn to ask these questions last as they complete their telephone applications. If something about that call seems like a scam, they’ll lose the sale. None of this matters. The sales agent who has the successful personality type – type two- will know what the SMSMSW acronym stands for. “Some will some won’t. So what?”

A good type two agent needs to have some narcisistic personality traits. They need to be empathetic enough to sense what a person is thinking, but not have so much empathy they can’t use and hurt them for their own advantage. They’ll learn to skirt the fact that insurance payments have to be made monthly for the better part of a prospective client’s entire life – that this is one of the more important decisions they will ever make. And if they know for a fact that they aren’t offering them the ideal product for their needs, no matter how well they convince themselves they really care about them, they’ll choose their personal comission over what is in the clients best interest. Have you won their trust? Are they feeling somehow uneasy? Call them on it. “Why specifically are you feeling hesitant? You won’t know if you qualify if you don’t apply. You can get a refund over the next thirty days if you change your mind and find something better.” Leave the responsibility of further research with the client. If they pay more for less or have buyer’s remorse after the thirty day refundability period expires, that’s their problem.

And that, my friends, is why five year-old leads are still being bought and sold. If I was a lawmaker, I would be doing something about that. Medicare is highly regulated to prevent this very type of thing. Non-government funded insurance products, not so much.

Bad Weeks Revisited and the IUL

Now step into my shoes. Imagine for a minute that I pay a thousand dollars a week for fifty live transfer leads at a rate of four leads a day, supposing that I can sell an average of 1:4, or one sold policy per day. An average life insurance policy commission advances me ten months of premiums typically yielding somewhere in the range of $500 to $1,500 in advanced commissions once the first premium gets paid. So I start out my week thinking I should be able to net $4,000/week in net income that I’ll receive into my bank account in another week or two. Now I can also expect that some clients will die in their first year. If that happens, I’ll have to pay back my commission advance. I’ll also lose it if they cancel any time the first year. These are called, “charge backs.” If the system worked the way it should, at that rate I would be earning over $200,000/year and probably paying back 20% in charge backs, so I should net $160,000/year. That was my business plan.

But there is a problem. Now imagine that the very same people that have called me have agreed with me, that me shopping for them so that they don’t continue to be barraged with phone calls is a good idea. But then picture them not responding to my texts or phone calls after I actually do conduct an hour or two of research for them to determine what the optimal solution is, given what they’ve told me.

Being a type-one agent, I might suppose the decision should center around whether what the carriers will offer fits into their budget. I may have done a quick scan while I was on the phone with them, but thinking that I am helping them solve the problem of shopping for insurance, I may need to compare things that an immediate scan won’t show, so that there is no possibility that my answer isn’t the ideal answer given their situation.

This happens when they are in poor health and I find out that the top carriers would offer them immediate coverage of the full face amount on a policy so I have to check outside that database and it also happens with people who are in very good health and qualify for an IUL.

Let’s talk about IULs. One of the most desirable insurance products is something called an Indexed Universal Life policy (IUL). I have contracts with quite a number of IUL providers, and these are considered the gold standard in insurance. But there are a lot of moving parts in IULs and not every carrier is offering the same product, making comparison shopping not all that simple. The better ones are like whole life policies in that they offer a face value benefit that is immediately payable in the event of death or certain conditions like terminal or chronic illnesses, but they also offer a cash value for life that is likely to grow more rapidly over time than a traditional whole life policy.

My point here is that researching the best policies is not something that can be accomplished during a single inbound phone call unless someone’s health falls somewhere in the middle. To do the right thing, I’ll have to do some research and call them back when I’ve come up with an optimal solution.

And therein lies the cog in the wheel of my business plan. As soon as I position myself to have to call them back, my very real, probably very best possible solution among all competitors, never reaches them. They have blocked my texts and calls and voice messages. They have failed to put my name in their contacts as they said they would, and I’ve wasted somewhere between two to three hours of my time and anywhere between $48 to $61. In truth, even though my lead was exclusive, they have already looked at Google to see what else they could find, and their contact info has been sold a hundred times. In the two or three hours it takes to gather up the information and take another inbound call or two, they’ve already received five more phone calls and they’ve forgotten who I was. As a result, I’m shooting myself in the foot by promising them I’ll check to make sure this is the very best product, or to go see if there is another carrier that might offer them immediate insurance, when an initial scan only indicated they could qualify for a guaranteed issue policy that won’t pay out full benefits until the third or fourth year.

I’ve had more than a few bad weeks because of this and it adds up. I can’t compete with AI and highly funded, organization-slick champion type two agents, who keep stealing my ethical old fashioned business. It’s even become unsustainable. Life before health made sense when all I was doing was in-home appointments here in Tallahassee locally. But I outgrew my local market. Tallahassee is a small city.

Pivoting

My wife hates the word “pivot.” She’s heard it way too many times and it always means that some business concept of mine is failing and needs to be adjusted. “Pivoting” sounds sort of like a radical change of direction, in fact, not just a minor tweak. And to be honest, one thing I know I can’t do, is pivot to an unethical proven success model. I can’t pivot my personality type.

What I can do, is I can ask for referrals. What I can do, is I can go out into pharmacies with a table and let people come to me out there. I can focus my energy on my ACA, Medicare, DSNP and private plan business. What I can do, is ask that if my friends see anyone who is on Medicaid, or needs to be, or qualifies for disability but got refused, that they be the ones to help them connect with Health and Human Services to get them the Medicaid they need, or with a social security disability attorney who will take them through another round of applications, and to help them log into SSA.gov and make sure they’ve applied for Medicare. They need to write down their Medicare Part A and Part B numbers once they’ve applied and if they have a Medicare card, I’m going to need to see it so I know what plan they’re currently on.

I’m thinking of people who have had life-altering accidents and strokes or who have otherwise become impaired and unable to help themselves or help me help them. Not everyone has family members who know how to help. If you will do that, then I can add efficiency to my business model by spending my time researching their best health plan options. I am really good at both life and health. But life has been beating me up. I’ve had one too many bad weeks. I’ll still do it, but I can’t both be ethical and win the rat race without your help. Help me help others. Quality referrals are my only hope. Can you help me with this?

Insurance is ridiculously complicated. And what saddens me is that the people who need it the most, are the ones least capable of obtaining it. Even if they can afford it, it’s just really hard to know who to turn to for answers. Heck, it’s not even easy to figure out what the questions are supposed to be.

Help Me!

Lately, I’ve been expanding my contracting in the states I’m licensed in. And that means I’ve been doing all sorts of additional training. My goal is to offer best of class healthcare coverage in every county. Life insurance is easy by comparison. It’s by state. If I’m licensed in your state, counties don’t matter. You’ll be covered. Health Insurance – that’s a different beast. First, there is the type you need. Then there is where you need it. What county do you live in? And then there is the type of network you want. Will you lose your doctor, or a much needed specialist if you change plans? Will your drugs all be covered? And what about if you have a chronic illness? What if you’re terminal? What if you’re in a nursing home? What if you are very poor and can’t afford standard healthcare?

With all these questions, you would be right if you guessed that it’s a little more complicated to provide a health plan than a life insurance policy. And to be honest, it doesn’t pay me as much. Many of my peers in the insurance business avoid it because it is a lot of work.

But I can’t do that. My inescapable reality is that I have a bleeding heart and it’s the people that need my help the most, that cry out for attention. I want to help them. The rich have more than enough helpers. The seriously infirm, the marginally qualified, those with special needs, those who might qualify for Medicaid and Special Needs Programs, those who need translators – these all need better support than they now have. And most don’t know how to ask for it. On a daily basis, I find that I’m like a sponge soaking up all I can to prepare myself to help. And be ready next time someone calls for it.

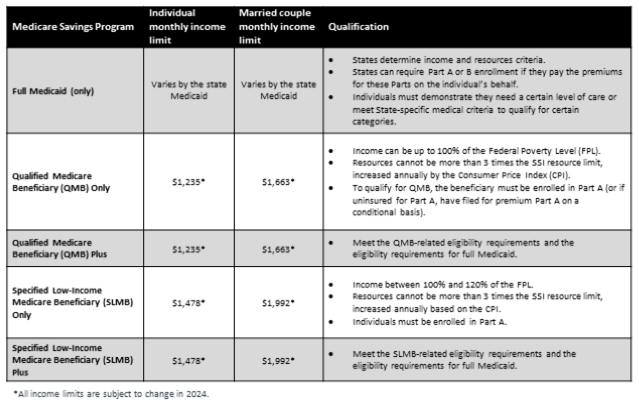

It can be distressing. Look at the lingo. According to the Centers for Medicare and Medicaid Services (CMS), those who qualify for dual special needs programs, (where they could get Medicaid and the state to pay for all or part of their Medicare expenses), are classified into the following five possible types. When I help them apply, I’ve got to classify them correctly. Tell me if this all sounds clear as mud to you.

FBDE – Full Benefit Dual Eligible only

Full Medicaid coverage refers to the package of services, beyond coverage for Medicare premiums and cost-sharing, that certain individuals are entitle to when they qualify under eligibility categories covered under a state’s Medicaid program. Some of these coverage groups are ones that states must cover (for example, Supplemental Security Income [SSI] beneficiares), and some are groups that states have the option to cover (for example, the “special income level” institutionalized group for individuals or home-and community-based waiver participants and “medically needy” individuals).

These indivudals get Medicaid only, are enrolled in Medicare Part A and/or B, and qualify for full Medicaid benefits, but not for Medicare Savings Program c ategories. However, the state may pay for their Part B premiums.

Beneficiaries pay no more than the amount allowed under the state’s Medicaid program for services furnished by Medicare providers.

QMB – Qualified Medicare Beneficiary Only without Other Medicaid

Medicaid pays Part A (if any) and Part B premiums.

Medicaid pays Medicare deductibles, coinsurance, and copayments for services furnished by Medicare providers for Medicare-covered items and services (even if the Medicaid State Plan payment does not fully pay these charges, the QMB is not liable for them).

QMB+ – Qualified Medicare Beneficiary Plus

Medicaid pays Part A (if any) and Part B premiums.

Medicaid pays Medicare deductibles, coinsurance and copayments for services furnished by Medicare providers for Medicare-covered items and services (even if the Medicaid State Plan payment does not fully pay these charges, the QMB is not liable for them).

Get “full Medicaid” coverage in addition to coverage for Medicare premiums and cost-sharing.

SLMB – Specified Low Income Medicare Beneficiary Only

Medicaid pays Part B premiums.

SLMB+ – Specified Low-Income Medicare Beneficiary Plus program

Medicaid pays Part B premiums.

Get full Medicaid coverage in addition to coverage for Medicare Part B premiums.

What this means and what to do about it are two different questions. What it means is some people qualify for extra help as spelled out above. Any US citizen falling on or below the poverty line is likely to qualify for state Medicaid. Even if they are as much 20% above the Federal Poverty Level (FPL), they can at least qualify to get their Medicare Part B premium covered. When people are on a low fixed income, every dollar counts.

What you can do about it is help me help people. Get them onto Medicaid, if you can. If not, see what they qualify for by helping them pay their bills. See if you can help them prove their income at their local Medicaid office.

If you’ll do that, I’ll do this

It takes a village. Having a bleeding heart is sweet, but I’m about maximizing the good I do. I know that if I spend my time tirelessly helping people get onto Medicaid and helping them with their bills, that I won’t be able to help those who have already taken those steps and now just need to get plugged into the best dual special needs plan for their needs so they can get to their doctor. Let me focus on the insurance side of the problem. Let their church friends and family help them with their Medicaid applications. Then let me know immediately what they’ve qualified for once they are approved. What is their individual or family income? Have they been approved for FBDE, QMB, QMB+, SLMB, or SLMB+? If you’re not sure which is which, call me. I can decipher bureaucracy-speak.

NOT AFFILIATED WITH OR ENDORSED BY THE GOVERNMENT OR FEDERAL MEDICARE PROGRAM.

Participating sales agencies represent Medicare Advantage [HMO, PPO, PFFS, and PDP] organizations that are contracted with Medicare. Enrollment depends on the plan’s contract renewal.

I do not offer every plan available in your area. Currently I represent 6 organizations in Tallahassee which offer 42 plans and other organizations with numerous but not all plans in six total states, including Florida, Georgia, Texas, Arizona, California and Virginia.

Most of my friends know that I’m a veritable insurance mall. I handle Medicare, dual Medicaid/Medicare plans (D-SNPs), and both traditional, supplemental and Medicare Advantage plans. I also offer Marketplace (Obamacare/ACA), as well as private and specialty health plans. And if that wasn’t enough, my core business – when we’re not in a Medicare or Marketplace open season – is life insurance. I represent numerous life insurance carriers and plans so that I can match individual needs with the plan that fits best.

Use this code to schedule me

It’s January 10th. As I post this, there are only six days left of open season for the Marketplace. If you are under 65 and have significant preconditions and don’t have a very high annual income, the Marketplace may be the best match for you. You can probably avoid premiums. Just be aware that having no monthly premiums to pay does not mean you get free healthcare. And think about it. If you have preconditions, that will likely matter a lot. Always check to see what your annual deductibles will be. And count up your most likely copays and costshare. Most “free” healthcare plans only pay 70-80% and that’s only after a huge annual deductible is out of the way. Don’t get me wrong. A lot of thes out-of-pocket expenses may be subsidized, as well. But then maybe not. I’m here to help my clients figure that sort of thing out and direct them to the plans that will save them the most money.

As you might imagine, my goal is to help as many people as possible. To do that, I’ve got to manage my time super well. I’m happy to educate people, but I also like to make sure they’ve followed my advice. If I don’t have the best plans for your needs, I’ll let you know. I don’t mind that at all. What gets me down is when people end a conversation saying they want to shop around some more, and then I find out they’ve chosen a plan that will cost them more.

Who becomes family when family is gone?

One thing that is particularly difficult for me emotionally is helping the seriously sick and poor with their health insurance. They are often incapable of providing the paperwork needed to prove they qualify for Medicaid or Low Income Subsidies (LIS). I will literally go the extra mile to help people who don’t know how to help themselves, sometimes driving far out of town. If a person needs Medicaid, their friends should know it. We need to be one human family and look out for one another. Managing bills when you’ve had a stroke and live alone can be near impossible. Imagine if you were alone and growing old. Who would help you? Be that friend. Step up. Let each person do what they do best. Make sure your friend has help. Bring them to your local Health and Human Services office and help them get them enrolled in Medicaid. Help them with their bills. They need you. Then once they are enrolled, they need people like me, to set them up with D-SNPs.

Qualifying for Medicaid triggers a special enrollment period for a D-SNP. That means I can help your friend outside of the normal enrollment periods most any time of year. I can work over the phone or face to face. Usually, the only limitation is that you will need to schedule at least 48 hours ahead of time using a Scope of Appointment form to schedule me once you’ve helped them enroll in Medicaid.

I’m sure you know your friend will also need legal representation if they can’t answer questions for themselves. Sometimes a non-family member can obtain a temporary power of attorney to help make insurance decisions on their behalf. Medical Power of Attorney, Living Wills and Advance Directives are related and sometimes critical to obtain to help people when they need it most. That said, I’m not an attorney and this is not legal advice. Downloadable forms can be obtained for free online for these purposes and you can personalize them. Then you would need to get your friend to sign them in front of a notary, but I would strongly suggest you consult with a local attorney before doing anything.

The seasons of our lives change. In the fall, I go into full Medicare mode. In the winter, I do both health and life. In spring and summer I focus on life insurance. And throughout the year I think about how I can help as many people as possible, especially those most incapable of helping themselves. Please help me help your friends. Understand that I can’t speak with you about their medical conditions or about any possible health plans without a scope of appointment that is properly authorized. And that means you may have to obtain a Power of Attorney so you can act on their behalf. If you are helping them gather the information they will need to apply for Medicaid, you will likely need a POA for that too.

NOT AFFILIATED WITH OR ENDORSED BY THE GOVERNMENT OR FEDERAL MEDICARE PROGRAM.

Participating sales agencies represent Medicare Advantage [HMO, PPO, PFFS, and PDP] organizations that are contracted with Medicare. Enrollment depends on the plan’s contract renewal.

I do not offer every plan available in your area. Currently I represent 6 organizations in Tallahassee which offer 42 plans and other organizations with numerous but not all plans in six total states, including Florida, Georgia, Texas, Arizona, California and Virginia.

You are problably aware by now that as an independent insurance consultant, I am like a virtual insurance mall. While I don’t have contracts with every carrier, I am licensed in multiple states to produce not just Medicare of every type, but also Obamacare for those under 65 and private insurance, as well. And I have more options for life insurance than most other agents too – more carriers, more products, more variety, sorting from among 95 top rated carriers based on your personal qualifications.

But do Insurance Malls offer shopping assistants?

The problem with the insurance mall concept is that it suggests casual browsing. If you treat shopping for insurance casually, then you are taking the wrong approach. You should be diligent and make a good decision. Good decisions can save you thousands of dollars. Bad decisions can cost you tens of thousands of dollars. All this affects those you love.

Also, in a mall, there is no consultant to guide you through a mass of complex options so that you can make the right decision about something you could need immediately and just don’t know it yet. What you need is an experienced coach. As I see it, my job is to encourage you to take the world of insurance seriously. There is nothing that affects your pocket book more dramatically than lack of adequate health or life insurance when you or your family needs it.

Being Over-Insured

You could have an accident tomorrow. You, or a loved one could have a stroke. Bad things happen to seemingly healthy people all the time and you never know when. I don’t have to tell you this or you wouldn’t be here reading about it. But don’t let such facts frighten you into buying more insurance than you need. You are buying too much insurance if you are unlikely to be able to make the premium payments. That part is obvious. But you are also buying too much insurance if the odds of you ever needing it are exceedingly poor, or if the same insurance would be included in another type of policy. You don’t want overlap. Third, you may be paying too much and probably are, plain and simple. Why pay more money for less insurance? Usually, the problem is being under-insured, of course, and then finding this out too late. Many, for instance, rely on their employer’s insurance, or their VA benefits, only to discover that their coverage has limitations. I strongly advise that you take the time to have me review your policies.

What To Expect From Me?

Are you in an enrollment season? Scan or click here to Get Medicare

I take a holistic and realistic approach as I help you shop for insurance. I leave my teaching to my blog. I assume you don’t have unlimited time to research this. So I will simply explain why one product is better suited for you than another and give you a recommendation based on your personal needs and qualifications. My goal is to get you set-up with an insurance plan effortlessly and without delay once we’ve identified the right products you need and searched for the best price. As always, insurance is highly regulated.

Scan here to Get Obamacare in Season

On the health side, there are only certain times of the year you can make changes. I’ll let you know when those are. For Medicare, you will need to complete a Scope of Appointment form to even talk to me about specific plans and there will be a 48 hour minimum delay before the appointment. That’s the law. For Marketplace products (Obamacare, AKA ACA), you’ll need to grant me permission to contact you.

Of course, I won’t contact anyone who hasn’t asked for help anyway. Same for life. If I call you, it is because you asked me to. I only ask that you keep your appointments and have the documents you will need on hand.

What Documents Do You Need?

In almost every case, you can expect simplified underwriting and instant approvals. The carriers I choose generally don’t require medical appointments. Instead they utilize information from the Medical Information Bureau (MIB) under HIPAA.

LIFE INSURANCE DOCS YOU’LL NEED TO HAVE ON HAND

Drivers License or proof of identity

List of Medications insured takes, dosages, how long taken

Names, Addresses, Phone Numbers of all proposed insured and their beneficiaries.

A good email address of the policy owner.

Policy owner’s social security number.

Bank Routing Number and Account Number to draw premiums from

HEALTH INSURANCE DOCS YOU’LL NEED TO HAVE ON HAND

Same as for Life (see above) except list of meds and beneficiary info aren’t needed

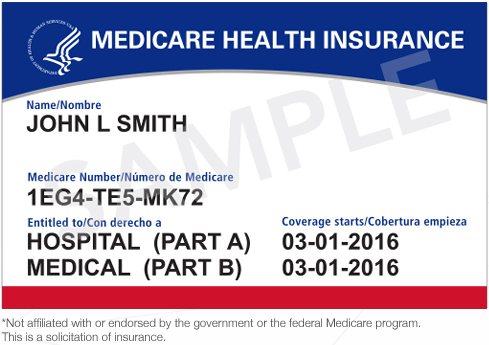

Medicare card if applicable

Name and address of Primary Care Physician if you have a preference

Name and address of any specialists you want to keep

Current Policy Info. (Carrier names, plan details)

List of drugs you want to see the prices of. (You don’t have to volunteer any medical information when applying for Obamacare or Medicare but it is often helpful when comparing plans)

What is Private Health Insurance?

In general, you will save money with private insurance and get the same or greater benefits if you qualify. On the downside, with private insurance you won’t get tax credits and cost sharing help from the ACA state or federally facilitated marketplace and you may not qualify if you have pre-existing conditions. On the positive side, you don’t have to pay for other people’s pre-existing conditions or subsidize their healthcare costs and this saves all of the members money. Generally, it is best suited for those who earn too much to qualify for significant tax credits in the marketplace and who don’t have significant pre-existing health conditions. Not everyone qualifies.

Most ancillary plans are also private. Ancillary plans cover serious conditions like cancer, heart attack and stroke on the one hand, and dental, hearing and vision, on the other. Many plans also offer network discounts and other benefits for things such as lab work, imaging and genetic analysis. Most private plans include medical appointments and counseling online or over the phone with little or no extra cost. Some private plans also specialize in short term medical and in-home care, which is not covered by traditional plans.

What is a Holistic Approach?

A holistic approach to life and health insurance looks at goals and budgets. It analyzes gaps in coverage and counts the cost of filling them and the risk of not filling them. Many people are surprised when they find they have been paying huge premiums only to encounter budget busting deductibles that prevent plans from paying the first benefit when a health crisis comes along. A holistic approach is educational. It is not enough to be insured. A person should know what is not insured and what risks they are taking and what the consequences of being under-insured can be. An independent insurance agent is your friend and guide. It is their job to keep you informed and adequately and appropriately insured. Many plans also offer incentives and benefits for going to the gym or for planning a healthy diet and for going in for regular check ups. An ounce of prevention is worth a pound of cure. Some plans also offer over the counter drug benefits, allowing you to purchase vitamins and other non-prescription drugs. As your guide, it is my job to help you weigh out these options. Sometimes a traditional plan saves you more money than a plan with lots of perks. If I can get you to fully understand what the trade offs are without overwhelming you with too much information, I’ve done my job well.

A holistic approach also considers your whole family. It helps you plan long term and considers your final expenses and legacy. On account of marketing regulations in the health insurance business, I generally start a discussion about life insurance first. I am not permitted by law to cross-sell life insurance to my Medicare clients. But my aim in producing life insurance is to help families keep homes, protect inheritances and build savings. Instruments like Indexed Universal Life insurance policies build wealth that can be transferred to loved ones at death without inheritance tax and free from creditors. Annuities and IULs can both be indexed to S&P etc. for more earnings than banks, yet guarantee against loss. Some offer living benefits. This means that if a chronic or terminal illness occurs, a life insurance policy can cover what a health insurance policy doesn’t. Life and health insurance are related through living and accelerated benefits. So, typically a conversation about life insurance will lead to a conversation about health insurance and savings plans.

Ultimately then, I’m simply your insurance guy. I don’t offer everything. Who does? No property and casualty insurance here, for instance. But I can offer group health and life, or individual and family health and life, as well. I’m very versatile. And if you’ve got a 401K, I can even show you how to convert it into an annuity that won’t be subject to market losses. Very cool. Like I said, I’m a virtual insurance mall. Just don’t be so casual. And don’t be too proud to ask for a guide. Everyone needs help. And very few people understand what being under-insured actually means.

Caviat:

NOT AFFILIATED WITH OR ENDORSED BY THE GOVERNMENT OR FEDERAL MEDICARE PROGRAM.

Participating sales agencies represent Medicare Advantage [HMO, PPO, PFFS, and PDP] organizations that are contracted with Medicare. Enrollment depends on the plan’s contract renewal.

I do not offer every plan available in your area. Currently I represent 6 organizations in Tallahassee which offer 42 Medicare plans and other organizations with numerous but not all plans in six total states, including Florida, Georgia, Texas, Arizona, California and Virginia.

Does insurance and medical terminology confuse you? I have a dirty little secret. It even confuses licensed professionals. The word ambulatory sounds like the word “ambulance.” So what is ambulatory surgery and what is an ambulatory surgery center (ASC)?

As it turns out, it has nothing to do with ambulances.

In short, ASCs save money because if you need surgery, you can simply get a provider or specialist to schedule you. ASCs skirt expensive hospital check-ins.

Typically, you go home after an ambulatory surgery. You save money by not spending the night. Does that remind you of something called “outpatient surgery?” It should. So, what’s the difference between “ambulatory surgery” and “outpatient surgery”?

Very simple. Ambulatory surgery is a type of outpatient surgery that doesn’t involve a hospital. It only involves an Ambulatory Surgical Center. And that will likely save you money.

Ambulatory Surgical Centers may say “Outpatient Surgery”

That said, be careful. On the downside, there could be complications a hospital could be better suited to deal with. For instance, an ASC may not know about all of your medications and allergies. It also may not be prepared to tackle any complications that its streamlined business model, designed to save money, is designed for.

Think speed and efficiency, but don’t let that confuse you. Despite the name, you may or may not need to take an actual ambulance to make your appointment to an ASC – more likely not.

Emergency transportation in an “ambulance” is another matter. What does your plan say about that? Let’s look up all of these possible costs together, measure risks and find a plan or combination of plans that works best for you. That’s what I do.

James Carvin is a Florida based insurance consultant licensed in multiple states.

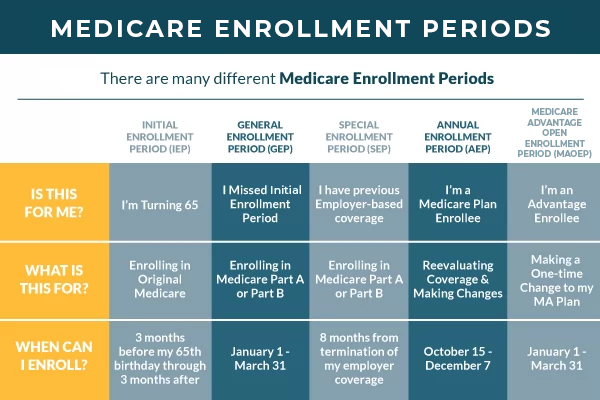

It may seem like a silly time to ask that question. The annual enrollment period just ended December 7th. But getting insured doesn’t always require waiting for an annual enrollment period. In today’s blog, I’ll summarize the exceptions…

#1 – If you are under 65 and healthy, Medicare is probably not what you want. What you want is Obamacare. Obamacare goes by a few other names – ACA, Marketplace, FFM. Don’t be confused. I’m here to make it all easier to understand. There is an open enrollment period for the Federally Facilitated Marketplace (FFM), (or your state marketplace, if you are in a state with a state FFM equivalent). For most people, it’s understood as Obamacare. But what’s in a name? Bottom line: your enrollment period ends January 15th. Call me. I’ll show you your options.

#2 – Some insurance products don’t have enrollment periods. For instance, odds are you can sign up for an indemnity plan any time of the year. You can also add on or remove dental, health and vision, or cancer, heart attack and stroke policies to your existing insurance. Obamacare and Medicare plans don’t normally cover these. You can also initiate a Health Matching Account at any time up to age 64 without respect to enrollment periods.

#3 – You may qualify for Medicaid. And if you qualify for both Medicaid and Medicare, you may be eligible for a Dual Special Needs Plan (D-SNP) with a Dual Special Enrollment Period (D-SEP). I have a heart for people in need. And the good news is that those who qualify, can enroll or change plans once every three months – except in the fall. But that’s when the Annual Enrollment Period (AEP) happens (Oct. 15th-Dec 7th), so even in the fourth quarter you can get enrolled or change plans if you are a Medicaid recipient who qualifies for Medicare.

#4 – Whether it’s Obamacare, or Medicare, if you move in or out of a service area, you’ll probably qualify for a special enrollment period (SEP). In fact, if you don’t change plans, carriers will boot you off your plan after you’ve been out of the area for six months. Don’t let this catch you off guard. Go ahead and change plans before or after your move. Ideally, you’ll remember to set an effective date for a health plan change a few months in advance as you are packing. I love getting calls from people moving to Tallahassee. I’m happy to be their tour guide.

#5 – You also qualify for a Special Enrollment Period if your plan gets terminated. Moving can do that. So can non-payment. Don’t let your policy lapse! Other reasons might involve fraud or duplicate coverage. Maybe your plan’s carrier went out of business. Or on a more positive note – if you were on a special needs plan for a chronic condition that you no longer qualify for, or because your icnome improved and you no longer qualify for a Dual Special Needs Plan. Whatever the reason, the good news is you may not have to wait until next year to get insurance.

#6 – Thinking even more positively, there’s also the possibility that a plan earned five stars. A plan earns five stars when it doesn’t get bad reports from enrollees. Companies that get compliments instead of complaints through the Center for Medicare and Medicaid toll free number get rated accordingly. When a company earns five stars, everyone in the network area has the option to immediately switch to that plan, or do so any time before the next annual enrollment period. Cool? Believe it or not, there is actually some incentive for these networks to meet or exceed your expectations. I should also disclose that part of that formula is agents like me. If I tell you about a plan, I want to make sure you get out of it what you are hoping for. Good communication is critical. Complaints stem from poor communication. Never rush when enrolling in health care. Learning about it can be a tedious process. There are too many choices. I’ve learned that good communication and consumer education is an art. It may be faster to just say, “trust me.” I can get people in and out of the door quickly if I have to. But medical costs and processes have harsh realities. I’ve done my job well if I’ve prepared you to know what to expect. Take time for quality decision making. Five stars.

#7 – Dramatic changes in your health or income may also qualify you to change plans outside of the annual enrollment period. This can be an improvment from a chronic or qualifying condition that triggers the loss of a plan as noted above (#5), or it can be a loss of health that qualifies you for a chronic special needs plan (C-SNP). There is also going into or coming out of institutions such as nursing facilities. This will trigger a thirty day period to change a plan under an I-SNP (SEPI). Don’t worry about the jargon and the acronyms. Just call me and I’ll give you more specifics.

#8 – Federally Declared Emergencies and Disaster Areas can trigger special enrollment periods. In Florida, we had Hurricane Idalia. This SEP declaration is effective: 08/27/2023 – 01/31/2024. All counties in the state qualify.

#9 – When we are talking about Medicare, there is always a bit of confusion about the difference between an Intital Eligibility Period (IEP) and an Intial Coverage Enrollment Period (ICEP). This relates to when a person actually enrolls in or qualifies for and takes advantage of Medicare for the first time as opposed to when they become eligible. A person becomes eligible three months before their 65th birthday to sign up for Medicare. This is the Initial Eligibility Period (IEP). It lasts until the end of the third month after their birthday and it comes in two possible parts – Part A and Part B. Part A is automatic and free when you request it from Social Security at https://ssa.gov.

Part B is optional and some people delay paying it because the premium is pretty significant. You may be penalized if you don’t pay it. You may have an equivalent from your employer’s group health plan. If you do, you won’t be penalized. The catch is that you still have to pay for Part B if you want a Medicare Advantage plan. And there are certain advantages to Advantage plans, but today we’re just talking about special enrollment periods, and the ICEP isn’t exactly a Special Enrollment Period (SEP). It’s standard. But both the IEP and the ICEP periods give certain qualifying individuals time outside of Annual Enrollment Period Oct. 15th – Dec. 7th, to enroll in or change Medicare plans. And that’s my summary of special enrollment periods.

#10 – When you do things matters. You can call me any time and ask for help. You can get all this same information at Medicare.gov and/or at CMS.gov. HealthCare.gov focuses mainly on Obamacare and the Marketplace or FFM. I am here to guide you through it all. Two other periods deserve special mention. For Medicare, there is an Open Enrollment Period (OEP) from Jan. 1st – March 31st. The Medicare Advantage Open Enrollment Period is for those on Medicare Advantage Plans. Whereas during Annual Enrollment period those qualified can make as many changes as they want until the period ends, Medicare recipients can make only one change during the Medicare Advantage OEP period. They can go back to traditional Medicare if they want. Or they can switch Medicare Advantage plans. If they go back to traditional Medicare, they can add a stand alone drug plan. The purpose of this period is to help people make adjustments when they’ve chosen plans they realize don’t really meet their needs.

The second special period is for Obamacare. This is the regular Open Enrollment Period for the Marketplace that begins November 1st and lasts until January 15th. We are now in that period. In my last blog, I described the various health care buckets. It is not always in a person’s best interset to be on a Marketplace plan. Private plans that don’t qualify for the Marketplace may be both less expensive and even cover more, depending on the plan. I already covered this a few blogs ago so I won’t repeat that here. Today, I just wanted to be clear about when to take action. In December and early January, I’ll be focusing my attention on the young and the relatively healthy since its open season. I do have contracts with a number of Maretplace carriers and plans, not all. But I also know most people want to save money. Call me and I’ll show you your options.

James Carvin insurance. Virtual or in home appointments in multiple states

As the 2023 Medicare Annual Enrollment Period (AEP) comes to a close (December 7th), I’ll be shifting my focus from Medicare to Marketplace and Group Health Plans from now through January 15th. Tis the season. If you happen to find out you don’t like a Medicare Advantage plan that you just got on, an adjustment to your Medicare Advantage plan, either from one to another, or back to traditional Medicare may be made January 1st through March 31st.

If health insurance confuses you, here is a quick summary. There are three basic types:

Medicare: Generally those 65 years old or more who qualify for social security or social security disability. Also those with ALS and End Stage Renal disease. To set up an appointment to get onto or switch Medicare plans near Tallahassee, call 850-270-2642. Elsewhere, dial 833-485-0194.

Marketplace: Generally the Marketplace is for adults 21 and up who don’t qualify for Medicare and don’t have Group Health Insurance. The Health Insurance Marketplace is also referred to as Obamacare and ACA, which stands for the Affordable Care Act. The ACA Marketplace is designed for those with low income and/or pre-existing conditions. Others not on Medicare should probably try Private Insurance to save money. Under 65 and don’t qualify for Medicare? Compare Marketplace plans here.

Private Insurance: Private Insurance is generally the best option for those who don’t qualify for Medicare and who don’t have Group Health, who have to pay too much for Obamacare because they earn too much and also don’t have pre-existing conditions. Paying too much for Obamacare? To schedule a consultation, dial 850-270-2642.

Outside the Buckets

In addition to the main categories above, there are certain special situations.

SNPs: If you’re on Medicare and also close to or below the federal poverty line, you may qualify for extra help, either through a Low Income Subsidy program (LIS), or state Medicaid. If you are both on Medaid and Medicare, then you qualify for a Dual Special Needs Program (DSNP). If you need free healthcare, DSNPs are one way to get it. There are also other types of SNPs, such as Institutional and Chronic Illness SNPs. If you qualify for an SNP of any type, there will typically be a Special Enrollment Period corresponding to it, which you should ask me about. If you know of someone going into or coming out of an institution such as a nursing or rehab facility, direct them to a licensed agent like me to see whether an adjustment to their plan makes sense.

Specialty Plans: There are some types of plans you can enroll in all year long. They don’t have enrollment periods. As an example, insurance for cancer, heart attack and stroke, for short term home health care, for long term care, for dental, vision and hearing, for health matching accounts and life insurance policies mostly don’t have enrollment periods. You can ask me about this type of insurance any time of year. I’ll help you compare plans and options you qualify for. Call 850-270-2642.

James Carvin insurance. Virtual or in home appointments in multiple states

Specializing in Hard Cases

I have noticed that the people who need insurance the most are commonly the people who are least able to afford it and unable to help themselves. This saddens me because I like to fix things for people. Very poor people, the elderly and the infirm can be hard to help. Many don’t have the same level of digital access. I have to meet with people several times and not everyone is capable of understanding everything that is at stake. It isn’t profitable to serve hard cases. It takes more time. Policies that require premiums often get canceled for non-payment and insufficient funds. People often make poor decisions.

My goal in the coming years will be to create an agency that specializes in handling hard cases and simplifying the complex for those in need. No one should be left behind. I hope to build an army of highly educated specialists for this purpose. If you would like to take part, I will be happy to train you. You have my number.

Many people suffer during the holidays. It is an exceedingly busy time of the year and many of our years are filled in preparation. We measure our goals annually. We compare this year with the last and see what hope we have for what remains. We reflect on our lives. No wonder Halloween seems to kick it all off. It can be a nightmare. Maybe that’s why my whole body broke down last week and today on Thanksgiving I’m still recovering. The stress of it all can be overwhelming. But I’m thankful for that sickness. While it spelled out complete failure in achieving my goals, since I was laid up in bed, it also gave me time to reflect and find a quiet place in the midst of the struggle. I needed to adjust the timing of my vision.

It’s Thanksgiving! Let’s think happy thoughts and express our gratitude! Oh, what’s that on my tooth?

Timing is seldom as we would have it. I have learned that the hard way many times. Then when the age of sixty five approached, it pushed itself onto my vision again, only to humble me, once more. So as if to ad to my nausium (sic), as the holidays approach, rather than being the Santa Claus that can help everyone I would like to help this year, I find myself fortunate to have a roof over my head, and food for my growing family, just barely making it. Here on Thanksgiving Day, with fifteen minutes I’ve set aside to express my thoughts – stretched by typos and editing much longer, I’m reminded by the occasion that I am indeed grateful for the Living God, who speaks to me despite my poor listening ability, even if it requires removing my health for the sake of slowing me down and finding that quiet place.

For many of us, myself included, the happy memory of youthful Thanksgivings gathered around large families, breaking out the leaves on the dinner table, enjoying parlor games, and if like me being able to swim and go to the beach without being cold because we’re from Florida’s paradise, and as children, having few cares in the world, we think to ourselves, “how can any Thanksgiving ever be like that again?” Most of the people we loved are gone, and certainly that carefree life is gone. We are the providers now, and we are not doing the best job of it. Family fortunes are lost. It’s up to us now to bring about good endings to our lives. Entering the senior years we consider what we can do with our remaining days to make the best of them. Some of us have more work to do than others. Some have achieved their dreams and have provided their children with the great experiences we had when we were young. If that’s you, I’m super glad for you. It’s exactly what I would hope for myself and for anyone.

My sincere wish for you and your family this year

Others grew up under-privileged. For these, I have a dream they will know one day what Thanksgivings like that can be like. Some have. Not enough. Never enough. I wish we all had that. Don’t you? We all have that opium of the people called religion to offer what the world fails to. That’s what I’d think if I’d lost my faith anyway. I’m among that 1% of philosphy post-graduates who is still a theist. Academia is misguided. I am here to show them their error – the details of which belong in some other blog. Today, I share my Thanksgiving Day thoughts. I am at a particular place in a particular way. I caught a very bad flu bug a few weeks ago that I still haven’t shaken. My head still sounds stuffy. I’m still in bed quarantining myself as best as I can from my wife and children.