I am an independent life, accident and health insurance producing agent based in Florida, licensed in multiple states:

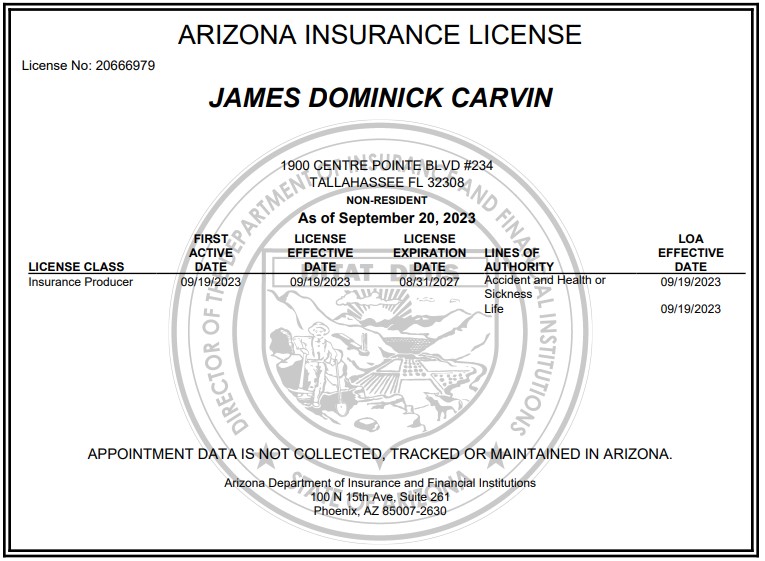

Arizona (20666979)

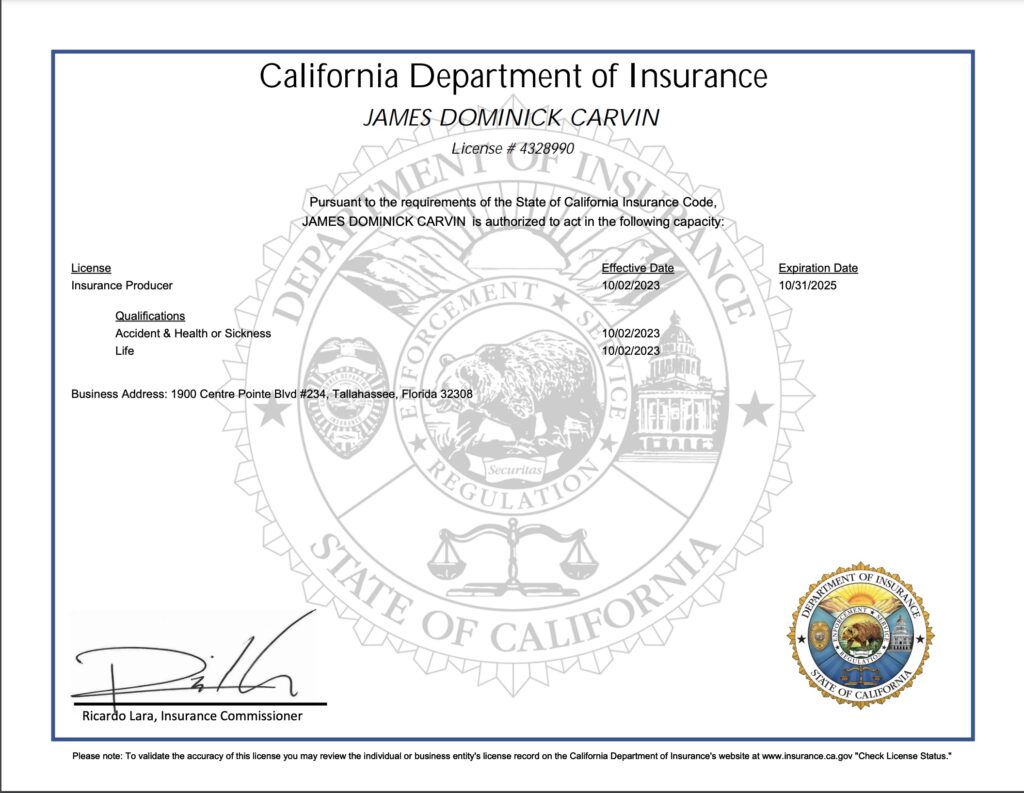

California (4328990)

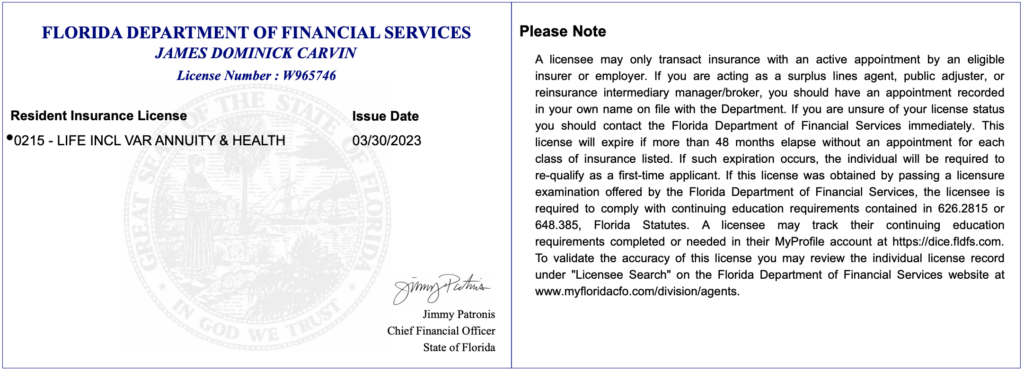

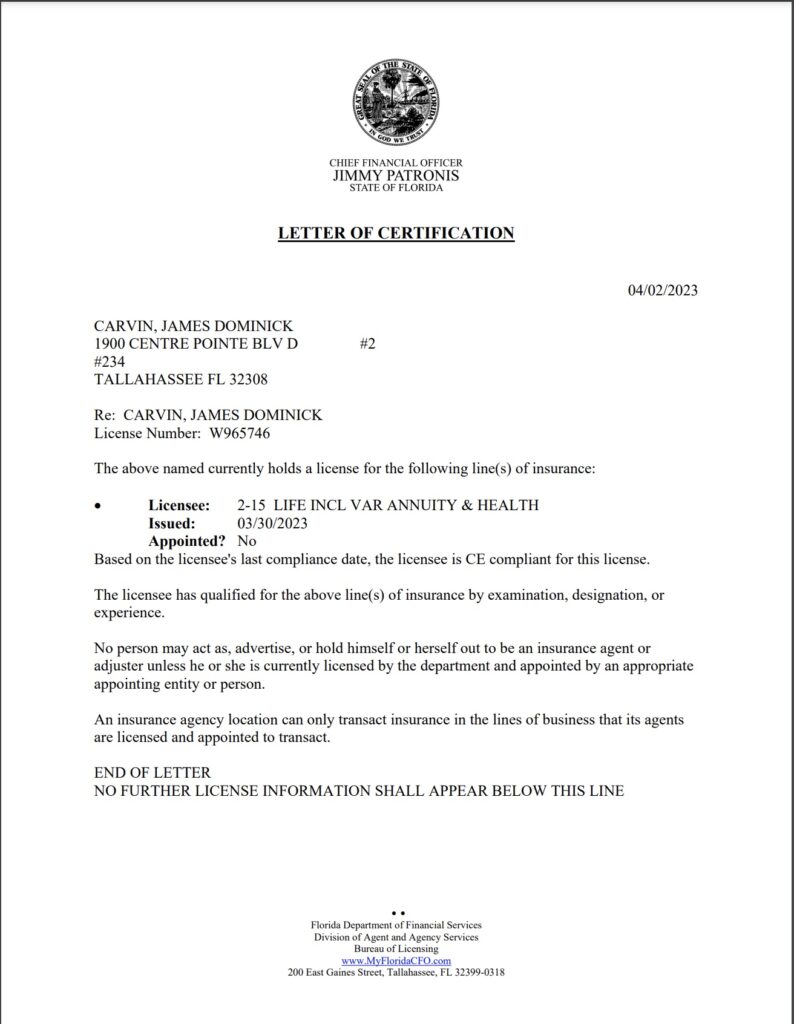

Florida (W965746)

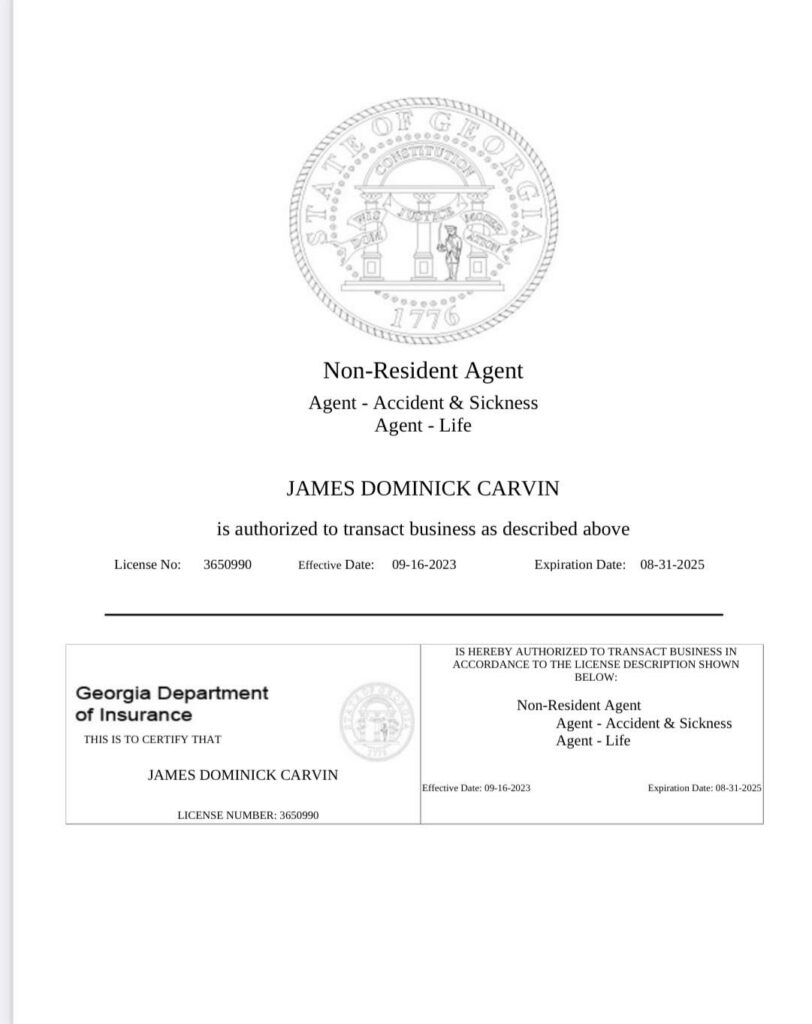

Georgia (3650990)

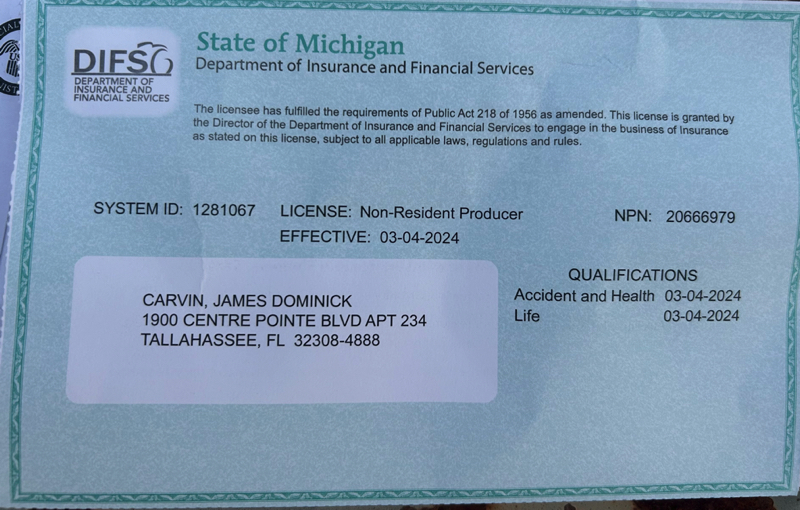

Michigan (20666979)

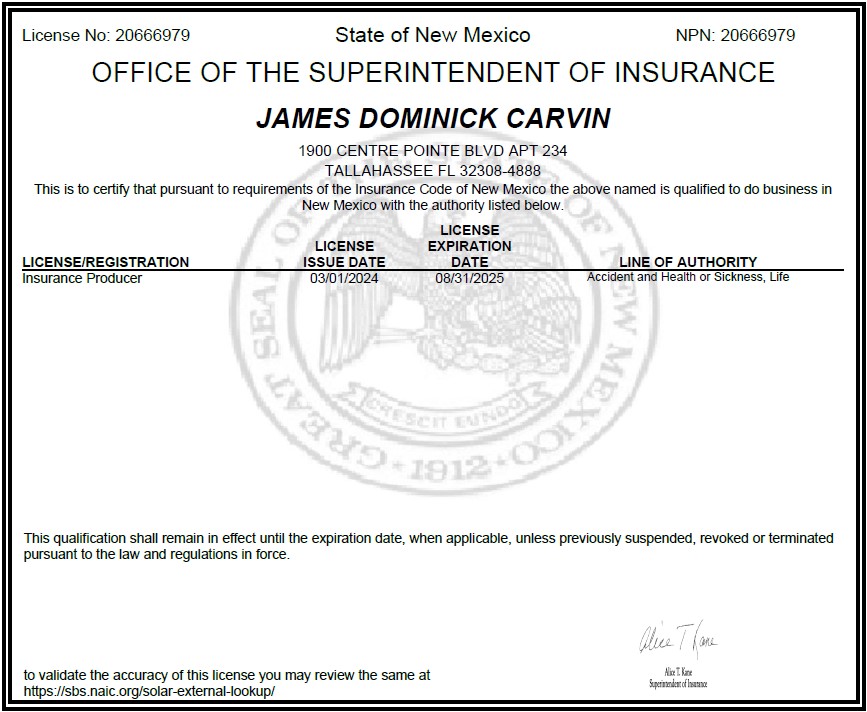

New Mexico (20666979)

South Dakota (40718581)

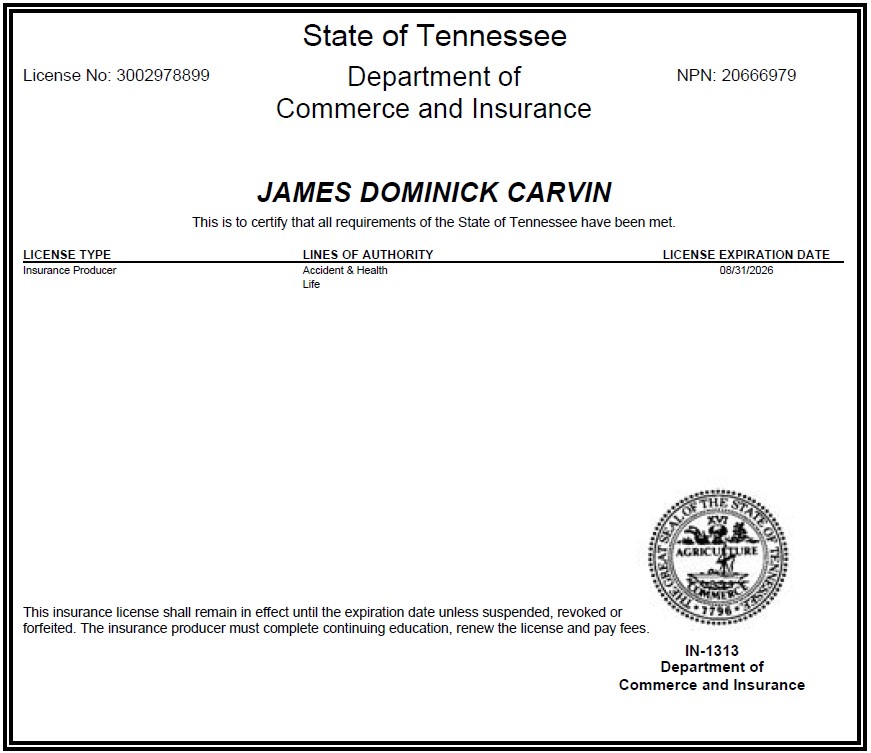

Tennessee (3002978899)

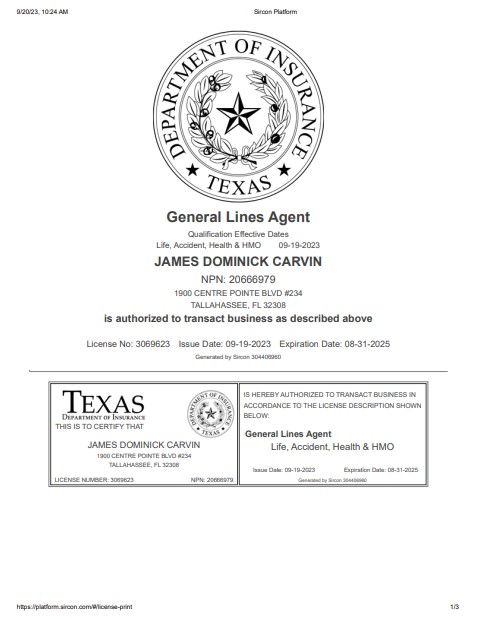

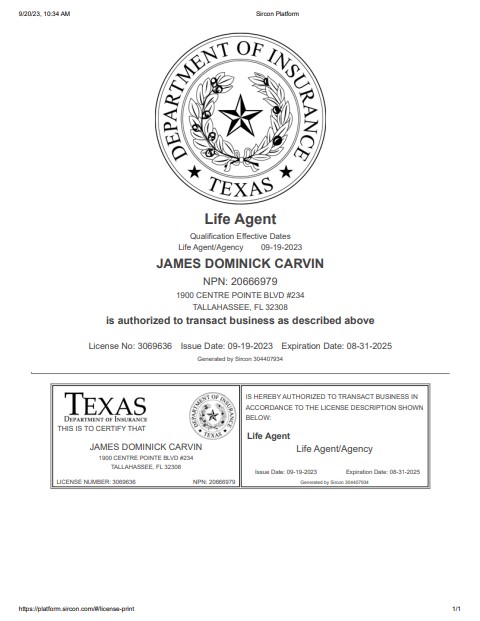

Texas (3069623/3069636)

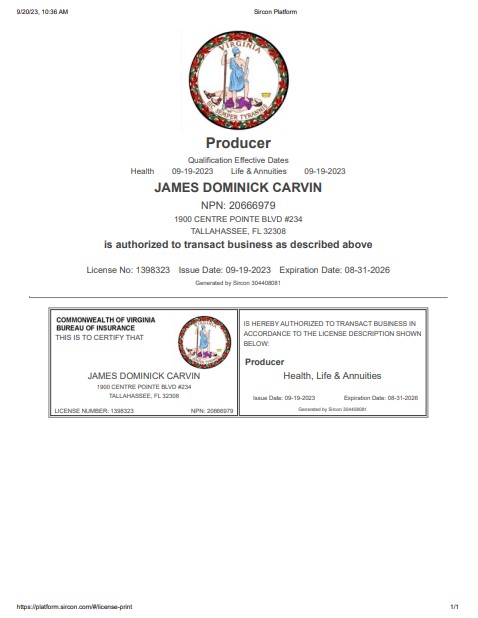

Virginia (1398323)

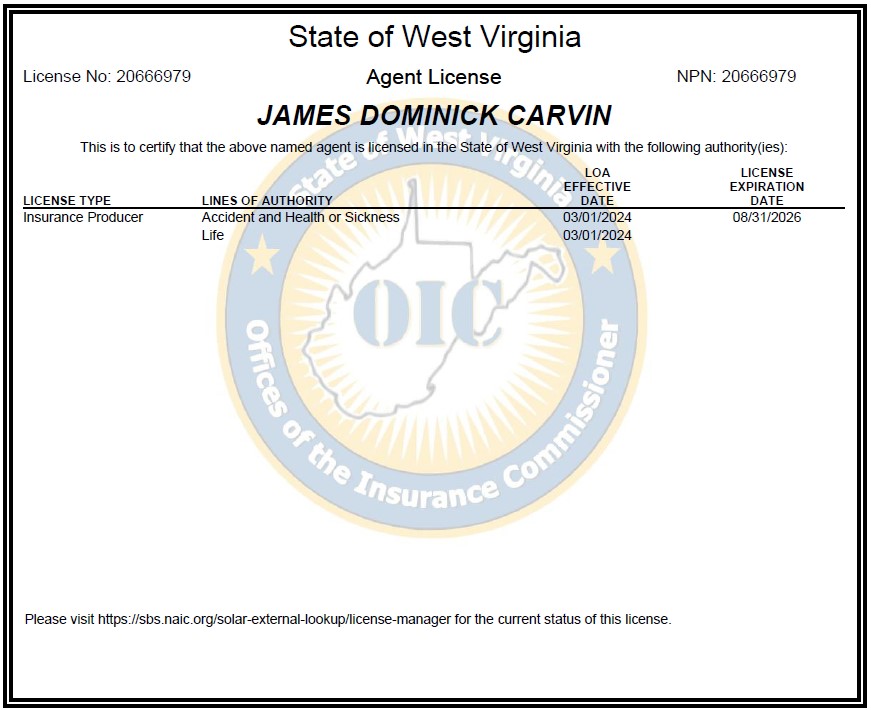

West Virginia (20666979).

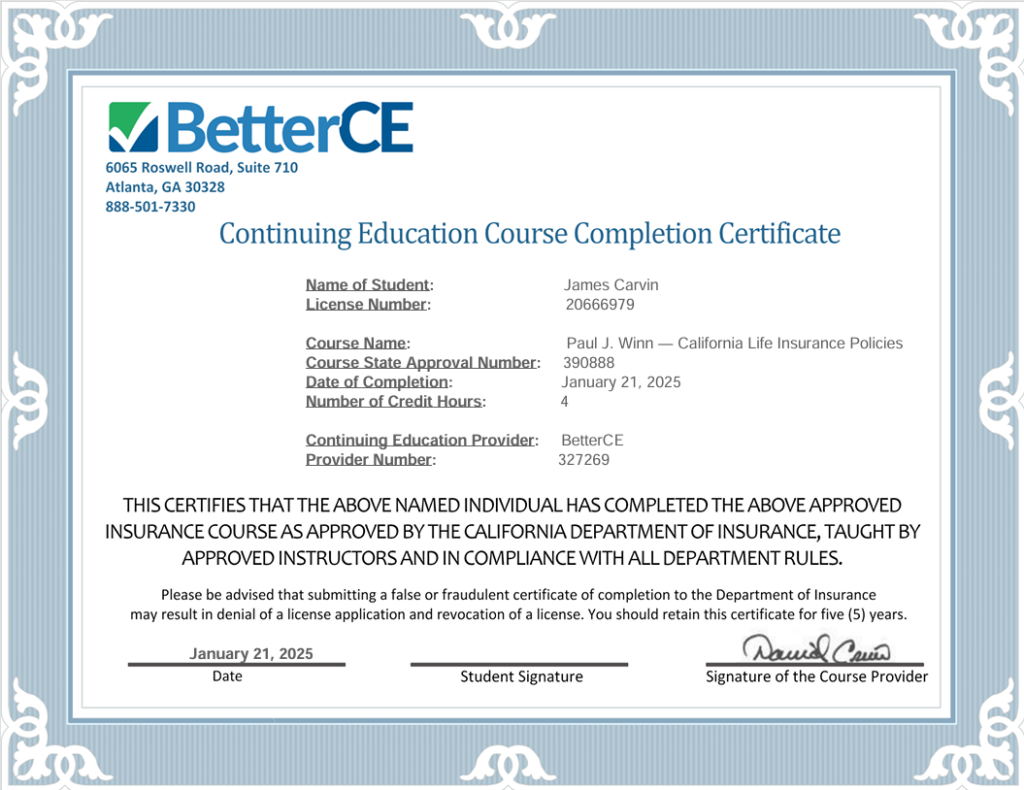

My license information and up-to-date certifications for continuing education requirements are included below for those who may need to check my credentials and eligibility.

NON-RESIDENT LICENCES

As my business expands, I will continue to add state life and health insurance licenses to this page. All licenses and certifications listed here are current.

Michigan 20666979

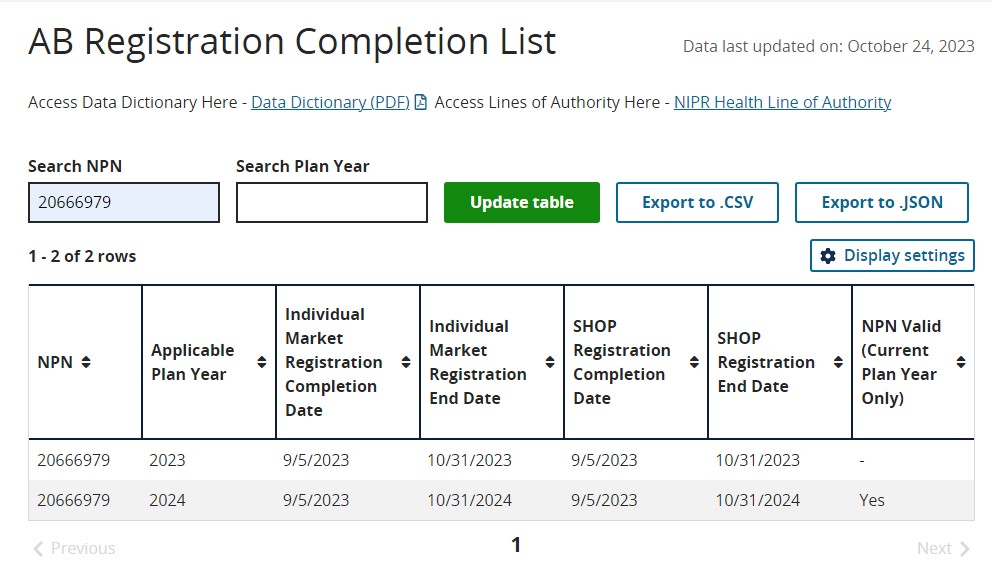

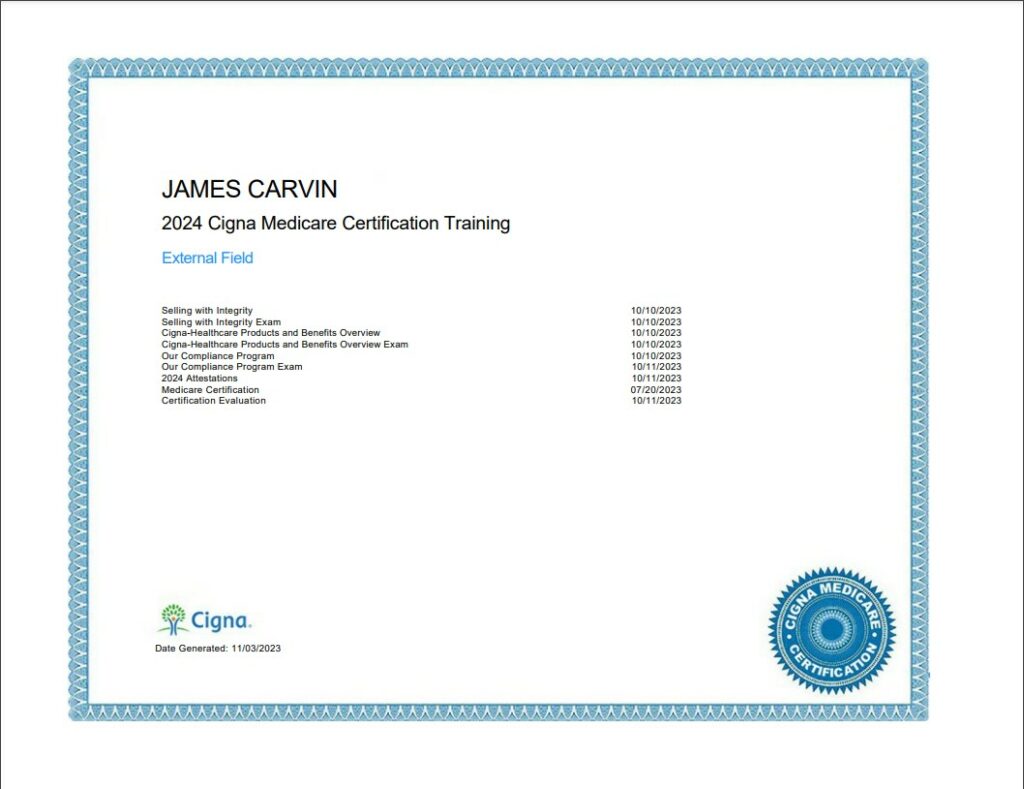

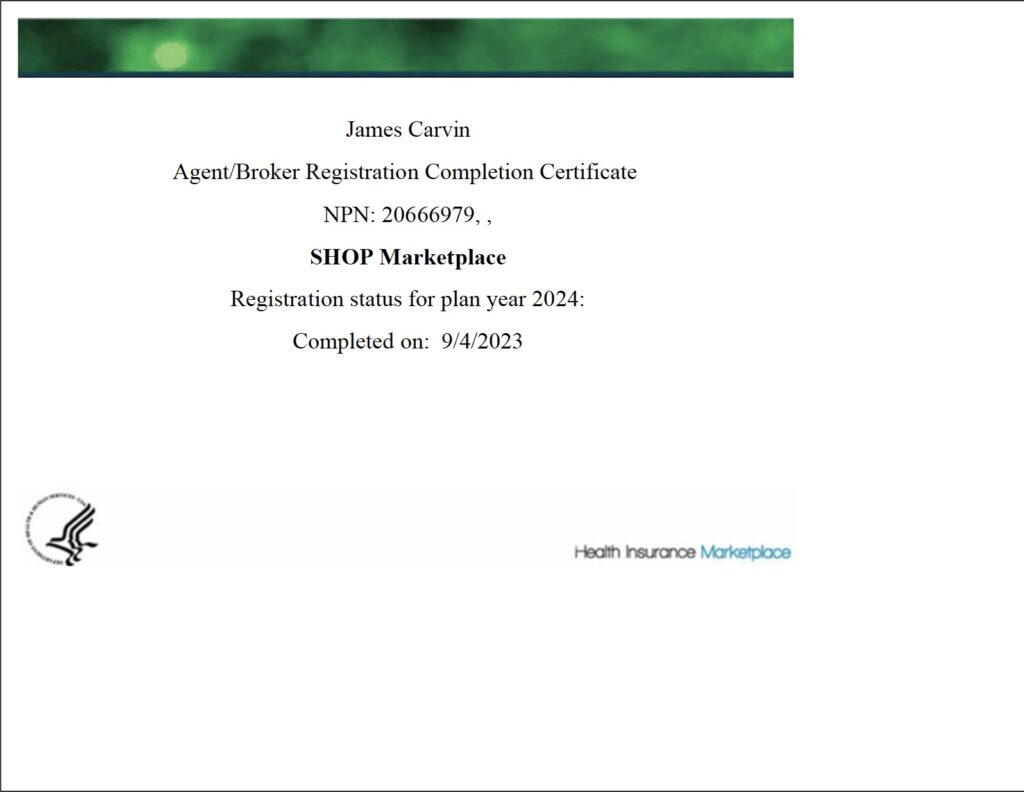

Medicare Certifications

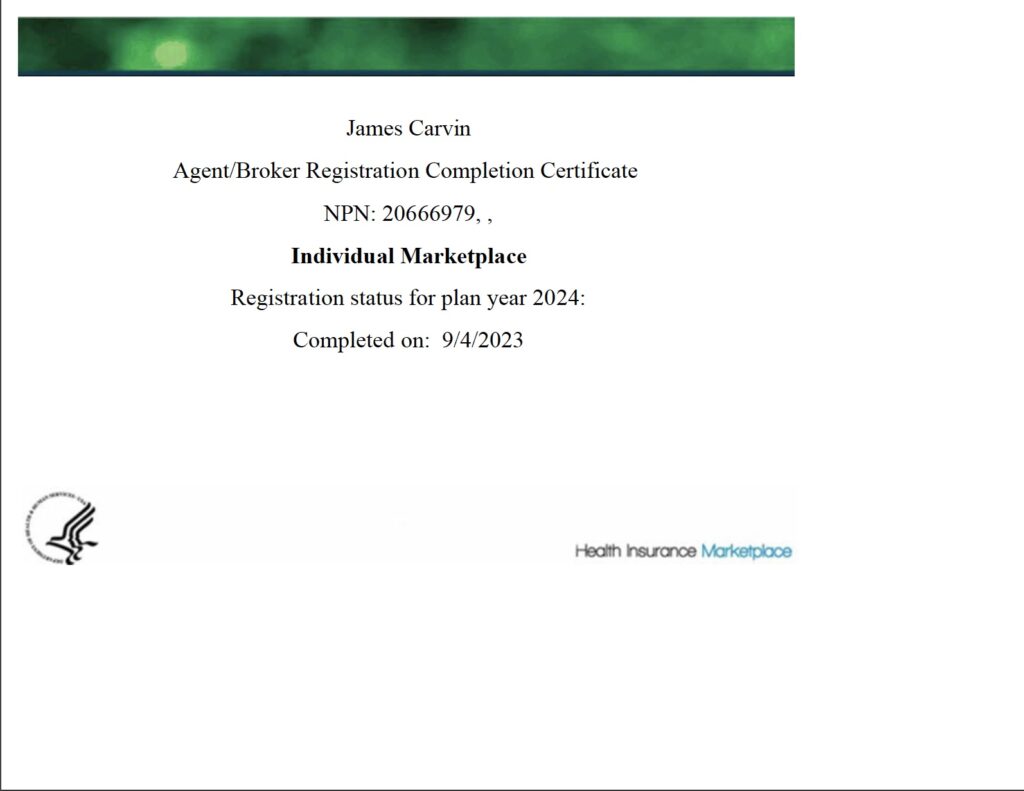

Marketplace Certifications (ACA/FFM)

About Me

I got into the life insurance business in my sixties after graduating from Arizona State University with a 4.0 average. My degree was in Interdisciplinary Studies with concentrations in Organizational Leadership and Philosophy. I already had a degree in Music Composition from the University of South Carolina that I’d earned in 1980 while on a springboard diving scholarship. And then after that I earned a theology degree, as well, after six years of study in two small colleges in South Florida – St. Vincent de Paul Seminary and St. Michael Academy, where I also served as an adjunct professor. I am a highly dedicated, very detail oriented person, who loves to teach and lead. JamesCarvin.com is a comprehensive web site that tells you not just about my life and health insurance brokerage but about my philosophical and entrepreneurial endeavors. Last year I completed Season One of my Awesomeology solo podcast. I’m currently looking for a co-host for Season Two. My motto is “Maximized Awesomeness.”

James Carvin, 1981

I am an Independent Broker working with Multiple Carriers and Plans.

I am not captive to one company or plan. I work with you as an independent broker to assess your family’s needs and goals. Many people ask for quotes when what they really need is guidance. Being independent enables me to do this.

There are three major marketing organizations I work with. Each contracts with multiple carriers to serve as many needs as possible. I do not have contracts with every carrier that these IMOs serve:

Family First Life – FFL contracts with a majority of A-rated life insurance companies, as assessed by AM Best, Fitch, Moody’s and Standard & Poor’s. I personally scan through ninety five A-rated carriers to find you the cheapest plan within your budget using FFL’s unique tools. FFL specializes in whole life, term, mortgage protection, children’s policies, annuities, IUL’s and accidental insurance.

Benzy – Benzy has contracts with well known carriers to provide health matching accounts and private indemnity plans that cover hospital costs, accidents, illness and out of pocket expenses from dental, health, vision, cancer, heart attack and stroke. Their ideal clients are in generally good health and they don’t benefit much from ACA tax benefits or cost sharing from the health marketplace. If you’ve been paying high premiums, high deductibles, high copays and astronomical cost sharing on top of that, then I can help you eliminate it through an indemnity plan and a health matching account. Benzy specializes in private health plans that don’t pass the high costs of pre-existing conditions and predictable expenses like pregnancy onto other members of the network, as is the case with ACA plans and other comprehensive medical plans.

Kellogg – Kellogg Insurance is my marketing portal for traditional comprehensive health plans and plans for seniors. Whether you qualify for accelerated tax credits and cost sharing due to your lower income, or you have pre-existing conditions or you are in your silver years, Kellogg has provided me the organizational power and training to help me help you.

In any of these areas, it is my goal to help you locate the ideal product for your personal, needs, qualifications and budget. Please note that I have contracts with many but not every carrier and my portfolio of products continues to improve over time as do the number of markets I serve.

Arrange a Consultation

If you are married, it is advisable that your spouse be present and attentive.

Carriers require payment and other sensitive information to set up monthly payments and check medical history for simplified underwriting.

Bloodwork and labs are not required for the majority of policies.

If you live in the Tallahassee vacinity, I am happy to accomodate those who prefer in-home consultations up to about fifty miles in any direction. Most of my work is over the phone or on Zoom. When signing electronically, many carriers will require an active email address and/or text. If you don’t have Zoom, I can share screens using your desktop or laptop’s browser. Typically over the phone there will be a discovery call followed by a plan call. Some carriers may require recording all contact and a 48 hour advance appointment using a scope of appointment form. To arrange a consultation of any type, click here.

Note: (1) In-Home consultations are only available within a fifty mile radius of Tallahassee. (2) Telephone consultations will be recorded and records kept ten years where required by law. (3) On-line consultations utilize Zoom or other video presentation technology and will require that you open a link sent to your email. On-line consultations are also recorded.

How to Proceed:

Step One: Read the instructions on how to prepare for our consultation. Step Two: Read and agree to the disclaimer. Step Three: Click on the link below that corresponds to the consultation method that you prefer – In-Home, By-Phone or On-Line.

Understand who I am and what I can do that others can’t. First, as an independent broker, I am not captive to one company or plan. I offer many. I will help you compare your options and meet your goals. Second, I don’t just offer health plans. I also offer life insurance and annuities, mortgage protection and long term care with the best rated carriers. I offer group health and life plans as well as wellness and workers comp. I offer individual and family health plans. I help those in financial need and those with pre-existing conditions. I help business owners and high income earners as well as those with special needs who may qualify for subsidies. I offer both ACA and private plans. Whether or not you have pre-existing conditions or you are a low income earner, I can help. I also offer both traditional Medicare and Medicare Advantage Plans. I offer Medicare Supplemental plans and Prescription Drug Plans. We will discuss your needs and I will help find the solution. That’s who I am and what I do. That’s why it is called consulting rather than sales. Prepare mentally for a very helpful consultation. I am going to help you and direct you to the best plan for your expressed needs. Make time for me.

Different types of meetings require different types of preparation. If we are discussing health plans, I won’t need all your prescription information, but if we are discussing life insurance, I will, so I can compare pricing and value and see which programs you qualify for. For health, since there are laws against discrimination, I can’t ask those questions. However, you will be interested in pricing and I am permitted to answer any questions you have about the cost of certain drugs or the availability of specialists and primary care physicians in a plan’s network. Prepare a list of questions. If you are on Medicare, have your Medicare card ready. If you are enrolling in Medicare for the first time, prepare by applying online at least two weeks before our meeting at SSA.gov so you can have your card before we meet. You must be enrolled in both Part A and Part B to qualify for a Medicare Advantage program. Check your card to make sure you are in both. If not, head to SSA.gov to get enrolled into Plan B.

Whether our consultation is about life or health insurance, have any existing policies you have available for review and comparison and have your banking info ready so I can enroll you into a plan, if needed. Normally payments are made monthly and you can select a date for your payments. You may also choose a different mode of payment, such as quarterly, semi-annually or annually, and select a start date for your plan. Some carriers may require your drivers license. Most require your social security number. For life insurance policies, have available the addresses and dates of birth of any beneficiaries. Most carriers won’t require the social security numbers or emails of your beneficiaries but those are helpful to provide just in case. The social security number prevents confusion about people with the same name. The email address and phone number of the beneficiary helps with notification in the event of your death. Having all this available before our meeting will speed things up tremendously.

If the meeting is about Medicare plans, (as opposed to a general discussion of Medicare not involving plan specifics), then you will have to submit a Scope of Appointment form (SOA) at least 48 hours prior to our meeting. Be aware that at any meeting discussing Medicare plans, I will not be permitted to discuss life insurance or ACA plans by law. Our conversation will have to be limited to what you check off on the Scope of Appointment form and the meeting will be recorded. The only meetings that won’t be recorded are face-to-face meetings. On-line consultations will be recorded on Zoom or other media as required by law. Virtual appointments do not legally qualify as face-to-face meetings according to the Center for Medicare and Medicaid Services. If you do not wish to be recorded, it is only required for Medicare. Let me know in advance of the call if you do not wish to be recorded and so long as it is not out of compliance, I will arrange to talk on an unrecorded line.

Timing matters. Prepare for enrollment periods by knowing when they are and whether they apply. Life insurance is best bought while young and healthy because its cheaper and has more value that way but it doesn’t have any enrollment period restrictions so much as plans that you’ll only qualify for at certain ages. Health Insurance involves enrollment periods you do need to be aware of and Medicare enrollment periods are different than Non-Medicare enrollments. The three main dates on Medicare to know are (1) the Annual Enrollment (AEP) Oct. 15th – Dec. 7th, which allows you to start new plans or change plans and make as many changes as you want (2) the Open Enrollment Period (OEP) Jan. 1st – Mar. 31st, when you can make one change to a Medicare Advantage plan and (3) Special Enrollment Periods (SEPs) throughout the year that can be triggered by events such as coming in and out of an institution or coming on or off Medicaid, discontinued plans or change of address that makes you lose your network. For ACA health plans, open enrollment is from Nov. 1st – Jan 15th and similarly there are Special Enrollment Periods throughout the year. Some indemnity plans and ancillary services aren’t subject to enrollment period restrictions. Be sure to ask me about indemnity plans as they are often the key to eliminating your out of pocket costs. Understand that it is my goal to reduce or eliminate your medical expenses entirely, if possible. And sometimes it is. You just need to know what to look for. Book me.

By completing this consultation scheduler tool, you agree that you have read and understood the following disclaimer:

DISCLAIMER:

1 ~ If you are NOT seeking Medicare or Medicare options such as supplementary insurance or Medicare Advantage or a Medicare Prescription Drug Plan or equivalent, DO NOT check the Medicare Disclaimer on the Scheduling tool.

2 ~ If you ARE seeking Medicare or Medicare options such as supplementary insurance or Medicare Advantage or a Medicare Prescription Drug Plan or equivalent, then YOU MUST check the Medicare Disclaimer on the Scheduling tool and the following disclaimers below shall apply:

2.1 ~ NOT AFFILIATED WITH OR ENDORSED BY THE GOVERNMENT OR FEDERAL MEDICARE PROGRAM.

2.2 ~ Participating sales agencies represent Medicare Advantage [HMO, PPO, PFFS, and PDP] organizations that are contracted with Medicare. Enrollment depends on the plan’s contract renewal.

2.3 ~ I do not offer every plan available in your area. Currently I represent 4 organizations in Tallahassee which offer 18 plans.Please contact Medicare.gov, 1‑800‑MEDICARE, or your local

State Health Insurance Program to get information on all of your options.

I should add some thoughts that help summarize my thinking. One of my goals in offering better health plans is to help families build legacies. If you have read my blog you know how important legacies are to me. A legacy is what you leave to the world after you die. Typically your family is most affected by your presence or absence. Some manage to build foundations and have more long term benefit to the world that survives them. Unfortunately, many legacies are destroyed by a simple failure to check their policies. Often the people that I meet are too embarassed to admit that they may never have checked their policy at work, or the fine print on a policy they picked up at the funeral home or got in the mail. We trust our employers and we are too busy to sort through anything with a lot of fine print on it. This is probably a bigger problem with life insurance policies than health insurance but it applies to both. The simple fact of the matter is that many policies don’t deliver what peo0ple think they do. Let’s check.

If you have access to your existing policies, please have these ready to review when I arrive so we can determine whether you should keep, cancel or modify them. If you do not know which carrier your policies are with or what your current premiums are, check your bank statements. If you are not making payments monthly, you probably don’t have a policy. If you don’t have a copy of your policy, show me the phone number on the bank statement where you are making your payment when I arrive. For life insurance policies, I will make sure that both you and your beneficiaries have a copy of all of your policies before I leave. For health insurance, you ought to have a card. If not, then what will you do if you get sick or have an accident? If a life insurance policy is with an employer, you probably do not have a policy since you don’t own it. Instead, you may have a certificate. Employer life insurance policies often offer far less than what employees assume they do. Did you read my story about Bob and Sally? The same is also the case with PreNeeds policies, renewable term policies, graded and guaranteed issue policies. I will discuss this with you when I arrive. Let me see them.

Location Matters

Once again, all in-home consultations must be in the greater Tallahassee, Florida region, where I live, or possibly Southern Georgia, where I’m also licensed. If you live outside of the Big Bend region or far from town, I prefer to help you by Zoom rather than by phone, so I can see you and you can show me your policies, if you have any. I also prefer to see the faces of the people I help. Visit my Licenses & Certifications page to see which states I am authorized to serve families in.

Be aware that I am not licensed in every state and not every carrier offers the same products in every state. Health insurance is also limited to networks. However, if you are not a Florida resident, in most cases, depending on the type of product, I can still help you. Be sure to let me know what state you are an official resident of before booking your session with me, so I can prepare for our meeting in advance. Otherwise, I will assume that the address you list is the address of your official residence. Florida residency requires that you generally live at your address for 180 days out of the year or more. A Florida drivers license is normally sufficient to establish that you are a resident. If I am not licensed in your state, please let me know where you are. I am always interested in expanding and need to monitor demand.